Question: Exercise 38 Assume a two-asset world. The two assets' expected returns and covariance matrix are given as follows: 0.04 E(ri) = 0.10, E(r2) = 0.16,

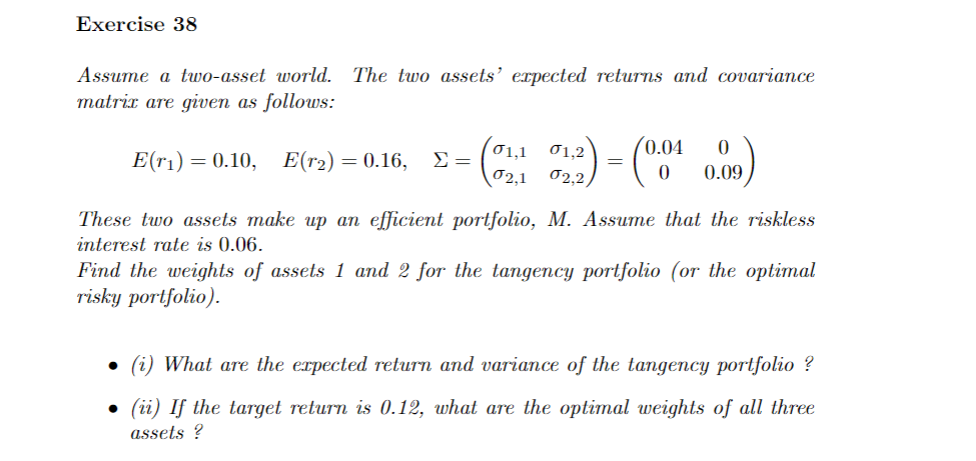

Exercise 38 Assume a two-asset world. The two assets' expected returns and covariance matrix are given as follows: 0.04 E(ri) = 0.10, E(r2) = 0.16, = 01.1 02,1 01,2 02,2 = = ( 0 0.09 These two assets make up an efficient portfolio, M. Assume that the riskless interest rate is 0.06. Find the weights of assets 1 and 2 for the tangency portfolio (or the optimal risky portfolio). (i) What are the expected return and variance of the tangency portfolio ? (ii) If the target return is 0.12, what are the optimal weights of all three assets ? Exercise 38 Assume a two-asset world. The two assets' expected returns and covariance matrix are given as follows: 0.04 E(ri) = 0.10, E(r2) = 0.16, = 01.1 02,1 01,2 02,2 = = ( 0 0.09 These two assets make up an efficient portfolio, M. Assume that the riskless interest rate is 0.06. Find the weights of assets 1 and 2 for the tangency portfolio (or the optimal risky portfolio). (i) What are the expected return and variance of the tangency portfolio ? (ii) If the target return is 0.12, what are the optimal weights of all three assets

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts