Question: Expected Return Standard Deviation Portfolio P. 12% 19% Market (M) 9% 15% The table above contains the return and standard deviation for Portfolio P and

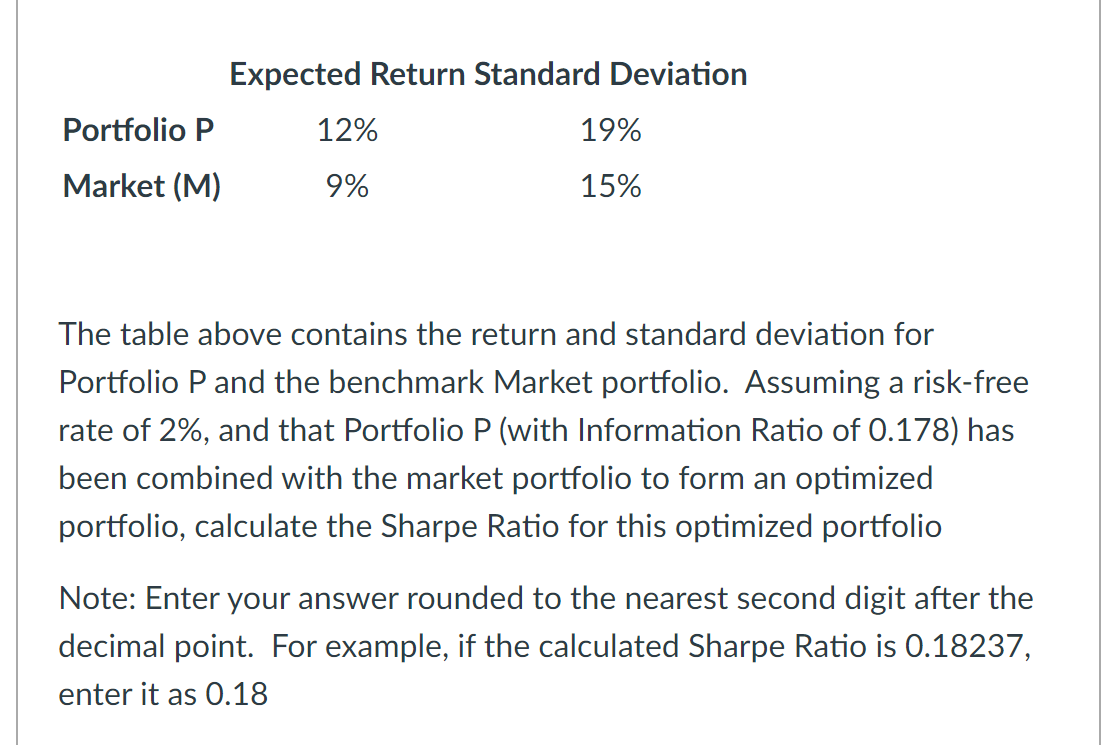

Expected Return Standard Deviation Portfolio P. 12% 19% Market (M) 9% 15% The table above contains the return and standard deviation for Portfolio P and the benchmark Market portfolio. Assuming a risk-free rate of 2%, and that Portfolio P (with Information Ratio of 0.178) has been combined with the market portfolio to form an optimized portfolio, calculate the Sharpe Ratio for this optimized portfolio Note: Enter your answer rounded to the nearest second digit after the decimal point. For example, if the calculated Sharpe Ratio is 0.18237, enter it as 0.18

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock