Question: Explain how to get to the answer and difference between european and american. A stock price is currently $ 4 0 . Over each of

Explain how to get to the answer and difference between european and american. A stock price is currently $ Over each of the next two threemonth periods it is expected to go up by or down by The riskfree interest rate is per annum with continuous compounding. Use riskneutral valuation.

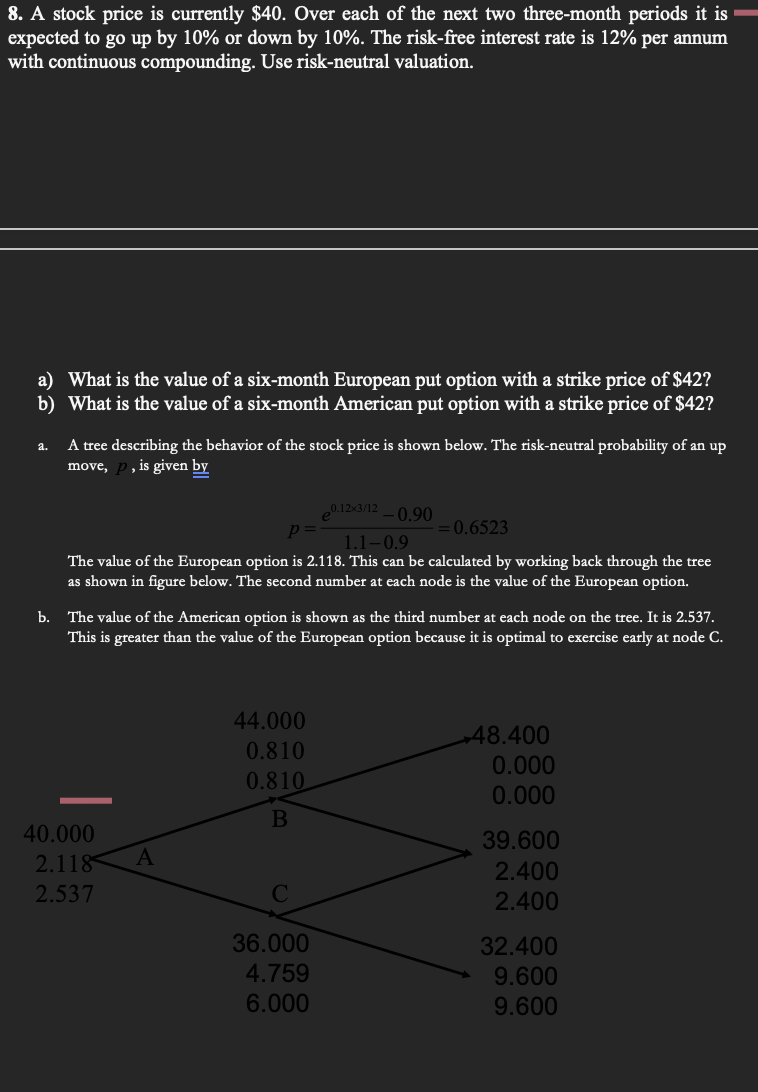

a What is the value of a sixmonth European put option with a strike price of $

b What is the value of a sixmonth American put option with a strike price of $

a A tree describing the behavior of the stock price is shown below. The riskneutral probability of an up move, is given by

The value of the European option is This can be calculated by working back through the tree as shown in figure below. The second number at each node is the value of the European option.

b The value of the American option is shown as the third number at each node on the tree. It is This is greater than the value of the European option because it is optimal to exercise early at node Ca Consider a European call option on a nondividendpaying stock where the stock price is the strike price is the riskfree rate is

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock