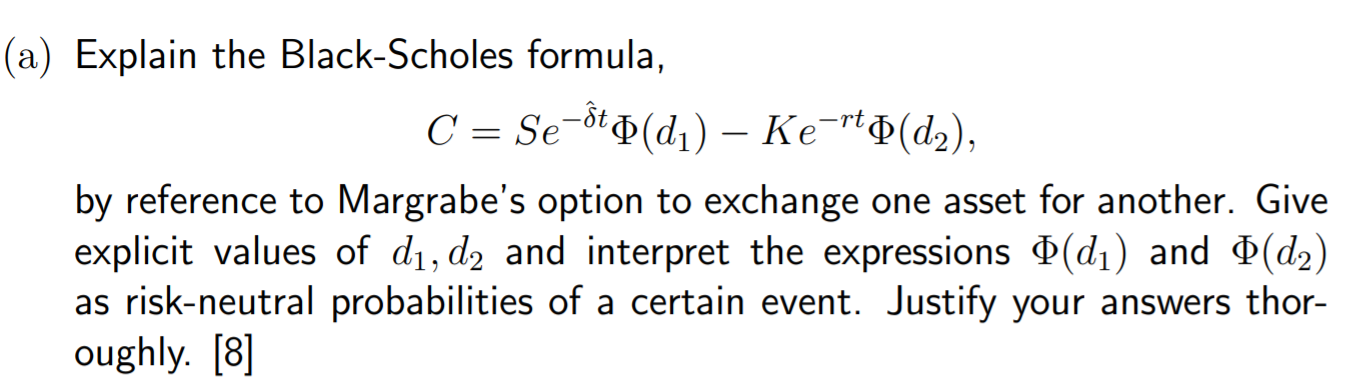

Question: Explain the Black-Scholes formula (a) Explain the Black-Scholes formula, C = Se-tb(d) Ke-rt (d2), by reference to Margrabe's option to exchange one asset for another.

Explain the Black-Scholes formula

(a) Explain the Black-Scholes formula, C = Se-tb(d) Ke-rt (d2), by reference to Margrabe's option to exchange one asset for another. Give explicit values of di, d2 and interpret the expressions (di) and (d) as risk-neutral probabilities of a certain event. Justify your answers thor- oughly. [8]

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock