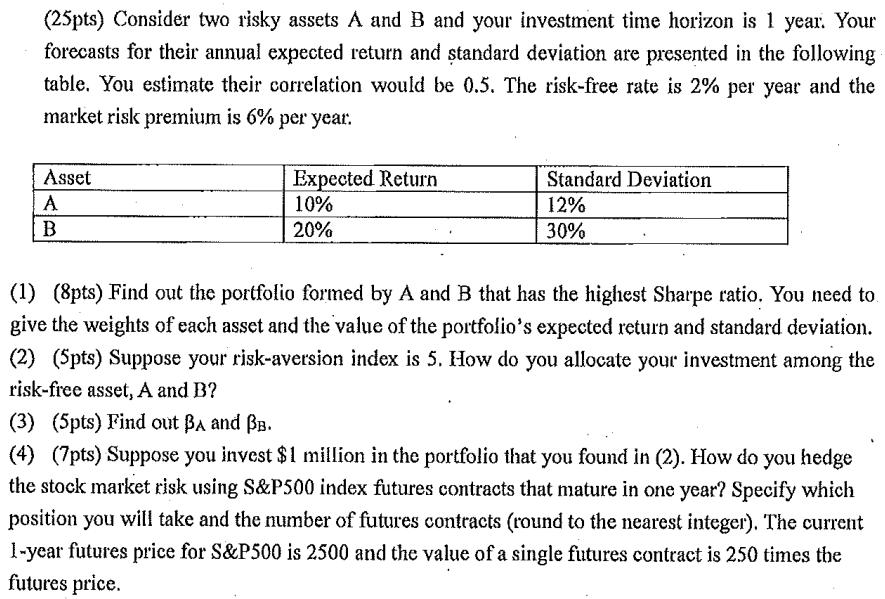

(25pts) Consider two risky assets A and B and your investment time horizon is 1 year....

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Answer 1 8pts Find out the portfolio formed by A and B that has the highest Sharpe ratio You need to give the weights of each asset and the value of the portfolios expected return and standard deviati... View the full answer

Related Book For

Posted Date: