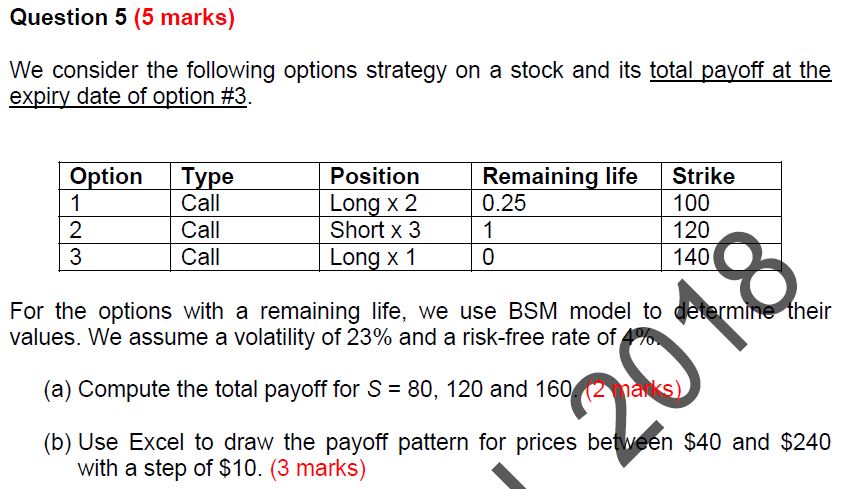

Question: Question 5 (5 marks) We consider the following options strategy on a stock and its total payoff at the expiry date of option #3

Question 5 (5 marks) We consider the following options strategy on a stock and its total payoff at the expiry date of option #3 O tion 2 3 Position Lon x 2 Short x 3 Lon x 1 Remainin 0.25 life Call Call Call Strike 100 120 140 m For the options with a remaining life, we use BSM model to values. We assume a volatility of 23% and a risk-free rate of (a) Compute the total payoff for S = 80, 120 and 16 (b) Use Excel to draw the payoff pattern for prices be with a step of $10. (3 marks) heir n $40 and $240

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock