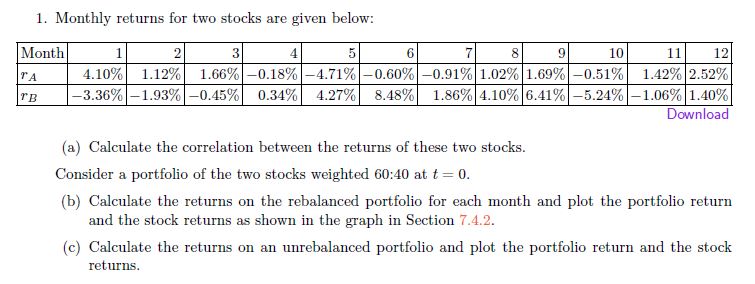

Question: Month 1. Monthly returns for two stocks are given below: 1.86% 4.10% 6.41% 5.24% 1.06% 1.40% 2 3 4 5 6 7 8 9

Month 1. Monthly returns for two stocks are given below: 1.86% 4.10% 6.41% 5.24% 1.06% 1.40% 2 3 4 5 6 7 8 9 10 4.10% 1.12% 1.66% 0.18% 4.71% 0.60% 0.91% 1.02% 1.69% 0.51% 3.36% 1.93% 0.45% 0.34% 4.27% 8.48% (a) Calculate the correlation between the returns of these two stocks. Consider a portfolio of the two stocks weighted 60:40 at t = 0. 11 12 1.42% 2.52% Download (b) Calculate the returns on the rebalanced portfolio for each month and plot the portfolio return and the stock returns as shown in the graph in Section 7.4.2. (c) Calculate the returns on an unrebalanced portfolio and plot the portfolio return and the stock returns.

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts