Facts: On January 1, 2022, Parent Co purchased 100% of the voting common shares of Sub Co.

Question:

Facts: On January 1, 2022, Parent Co purchased 100% of the voting common shares of Sub Co. Parent Co uses the equity method to account for its investment in Sub Co. At the acquisition date, $810 of the purchase price was attributed to land that had a fair value in

excess of the carrying value on Sub Co's books. In addition, $270 of the purchase price was attributed to equipment that had a fair value in excess of the carrying value on Sub Co's books. At acquisition date, the equipment had a remaining useful life of 10 years.

It is assumed that the consideration paid by Parent to acquire Sub Co was equal to the fair value i.e., market value) of the business and that the fair value of the business exceeded the fair value of net assets acquired at the acquisition date by $540.

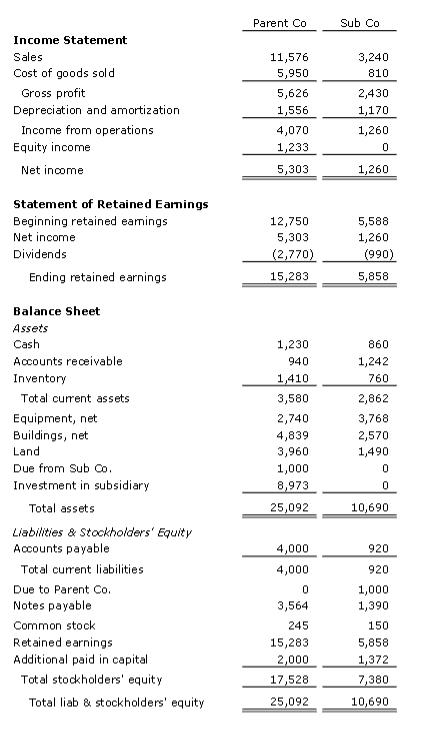

It is now December 31, 2022, and consolidated financial statements need to be prepared. As of year-end, Sub Co had borrowed $1,000 from Parent Co, without interest. Parent Co and Sub Co's financial statements at the end of the first year following the acquisition are detailed in the Excel file "Case 1 - Advanced accounting topics."

Required: Using the Excel file "Case 1 - Advanced accounting topics" and the worksheet

"Part I," prepare the eliminating/consolidating journal entries and the consolidated financial statements at

the end of the first year following the acquisition. Ignore tax effects for any adjustments to the income statement.

Expert Answer:

Modern Advanced Accounting in Canada

ISBN: 978-1259087554

7th edition

Authors: Hilton Murray, Herauf Darrell