Question: fd= incorrect, f0= incorrect, fu= incorrect one-step binomial tree put option risk neutral probability CJ's stock is currently trading at $36 a share. CJ's stock

fd= incorrect, f0= incorrect, fu= incorrect

fd= incorrect, f0= incorrect, fu= incorrect

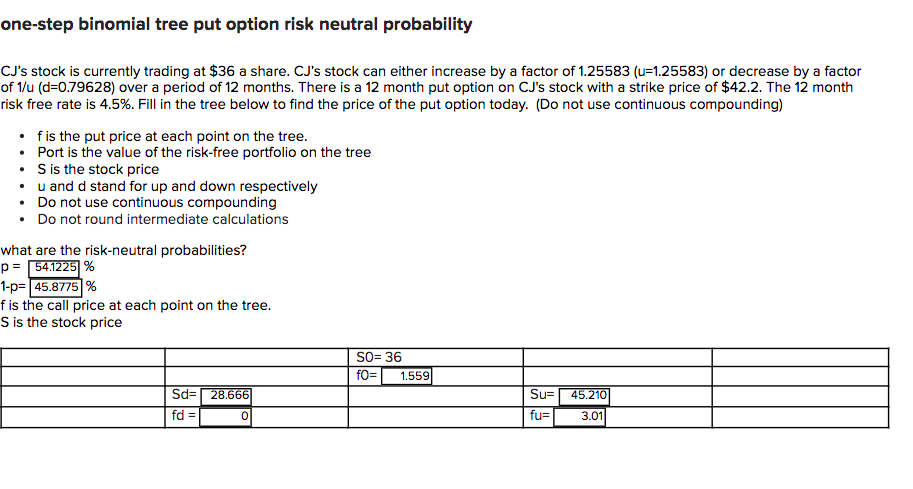

one-step binomial tree put option risk neutral probability CJ's stock is currently trading at $36 a share. CJ's stock can either increase by a factor of 1.25583 (u=1.25583) or decrease by a factor of 1/u (d=0.79628) over a period of 12 months. There is a 12 month put option on CJ's stock with a strike price of $42.2. The 12 month risk free rate is 4.5%. Fill in the tree below to find the price of the put option today. (Do not use continuous compounding) fis the put price at each point on the tree. Port is the value of the risk-free portfolio on the tree . S is the stock price u and d stand for up and down respectively Do not use continuous compounding Do not round intermediate calculations what are the risk-neutral probabilities? p= 54.1225 % 1-p= 45.8775% fis the call price at each point on the tree. S is the stock price SO= 36 fo= 1.559 Sd=28.666 fd = 0 Su= fu= 45.210 3.01

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts