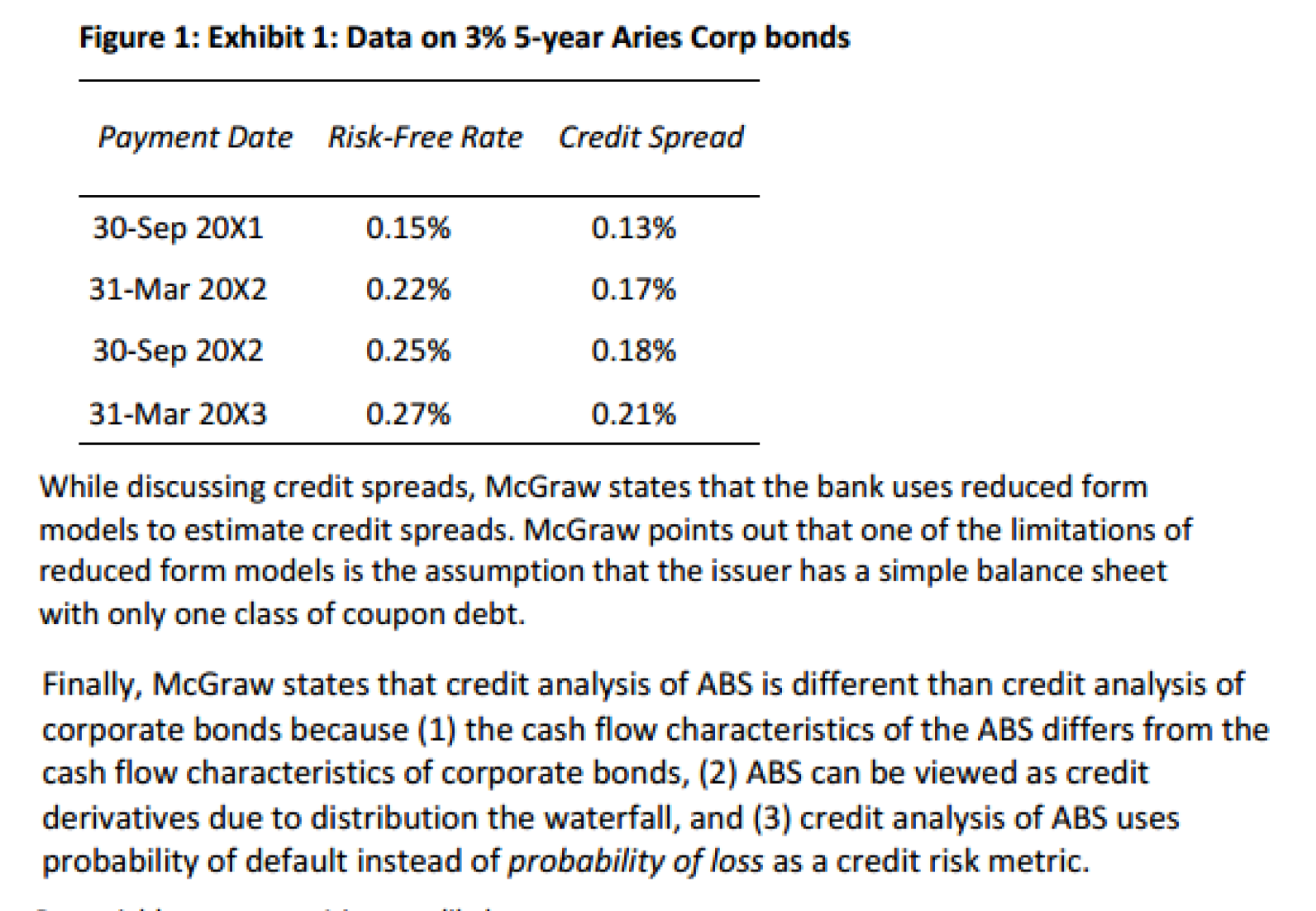

Question: Figure 1: Exhibit 1: Data on 3% 5-year Ari. Corp bonds Payment Date Risk-Free Rate Credit Spread 30-Sep 2011 0.15% 0.1396 31-Mar 20KB 0.22% 0.1796

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock