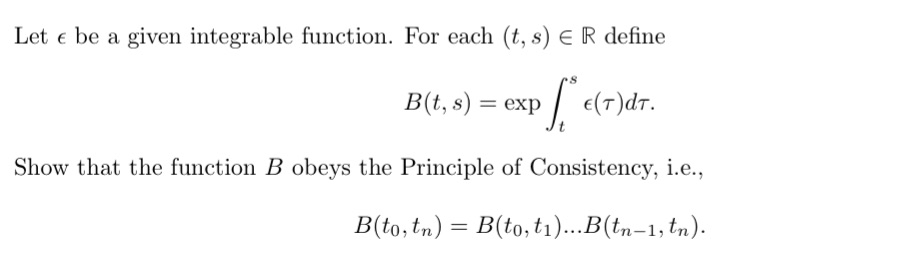

Question: Financial Mathematics Let e be a given integrable function. For each (t, s) E R define B(t, s) = exp E(T) dT. Show that the

Financial Mathematics

Let e be a given integrable function. For each (t, s) E R define B(t, s) = exp E(T) dT. Show that the function B obeys the Principle of Consistency, i.e., B(to, tn) = B(to, t1)...B(tn-1, tn)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock