Question: please provide steps 5. a. Let K, T, o and r be positive constants, and define the function g : R - R as b(z

please provide steps

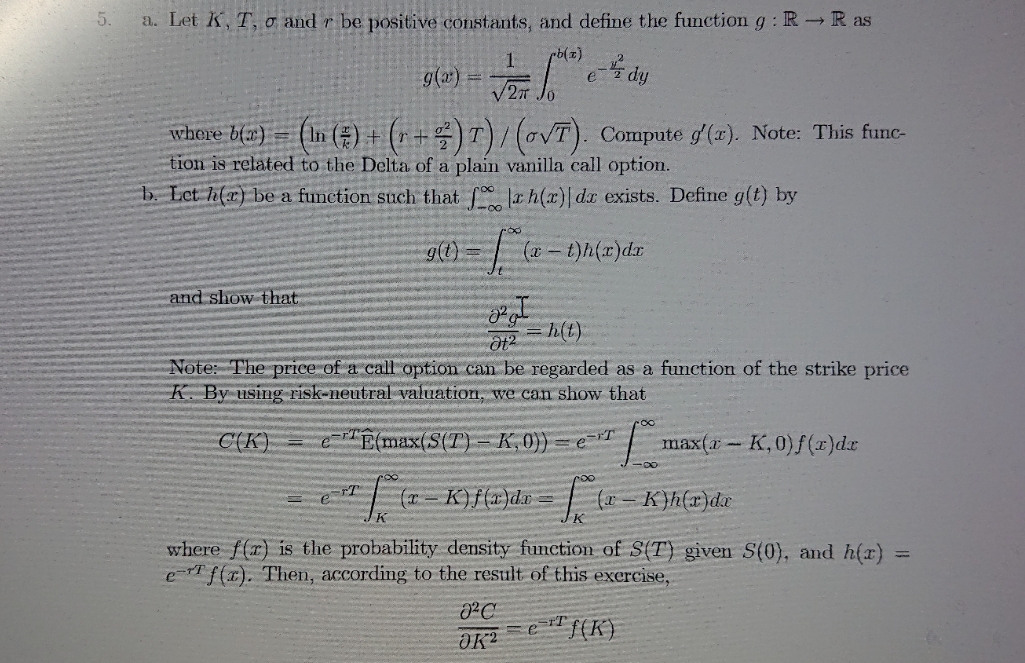

5. a. Let K, T, o and r be positive constants, and define the function g : R - R as "b(z ) g(2) - VZx Jo e - z dy where box) = ( In (#) + (r+ 2 ) T) / (GVT ). Compute g'(x). Note: This func- tion is related to the Delta of a plain vanilla call option. b. Let h(r) be a function such that f" (ah(x) | dax exists. Define g(t) by " (1) = (x - t)h(2)dx and show that atz = h (t) Note: The price of a call option can be regarded as a function of the strike price K. By using risk-neutral valuation, we can show that "(K) - eE(max(S(T) - K.O)) - e- T ( max(x - K,O)f(r)dx -DO K ( r - K)f()da = (x kyh(x)dx K where f(x) is the probability density function of S(T) given S(0), and h(x) = e If(x). Then, according to the result of this exercise, One e " f( K)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts