FluTech has a year-end of 31 March and acquired Equipment A and Equipment B on 1 Apr

Question:

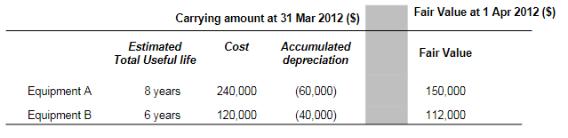

FluTech has a year-end of 31 March and acquired Equipment A and Equipment B on 1 Apr 2010. The estimated useful life at acquisition is 8 years for Equipment A and 6 years for Equipment B. Both items are depreciated on a straight-line basis with no estimated residual value. For Equipment, the entity applies the revaluation model under IAS 16. For both items, there was no revaluation adjustment prior to 1 Apr 2012. However, there is a sudden change in fair value on 1 Apr 2012 as below.

On 31 Mar 2013, no revaluation adjustment is required.

On 31 Mar 2014, Equipment A has a fair value of 135,000, and Equipment B was sold on that date for

cash $80,000.

The entity uses the elimination method for revaluation adjustment. It makes an annual transfer from its

revaluation surplus reserve to retained earnings in respect of excess depreciation.

Required:

(Ignore tax. Narratives explaining the journal entries are not required. You may calculate all amountsto the nearest dollar.)

(a) Prepare all journal entries associated with Equipment A and Equipment B, separately, as required under all relevant IFRS from 1 Apr 2012 to 31 March 2014. Year-end journal entries to close income and expense items to balance sheet equity are not required.

Expert Answer: