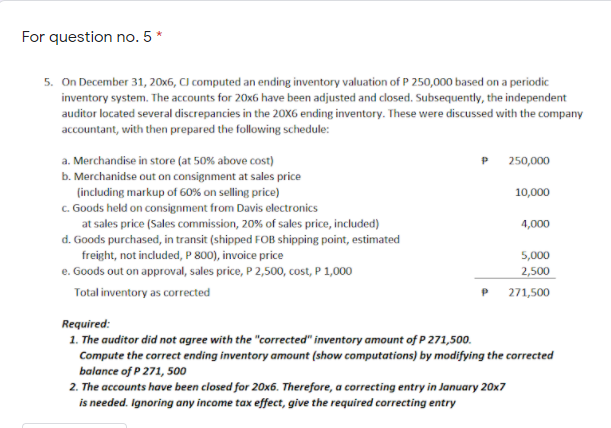

Question: For question no.5* 5. On December 31, 20x6, Cl computed an ending inventory valuation of P 250,000 based on a periodic inventory system. The accounts

For question no.5* 5. On December 31, 20x6, Cl computed an ending inventory valuation of P 250,000 based on a periodic inventory system. The accounts for 20x6 have been adjusted and closed. Subsequently, the independent auditor located several discrepancies in the 20x6 ending inventory. These were discussed with the company accountant, with the prepared the following schedule: a. Merchandise in store (at 50% above cost) P 250,000 b. Merchanidse out on consignment at sales price (including markup of 60% on selling price) 10,000 C. Goods held on consignment from Davis electronics at sales price (Sales commission, 20% of sales price, included) 4,000 d. Goods purchased, in transit (shipped FOB shipping point, estimated freight, not included, P 800), invoice price 5,000 e. Goods out on approval, sales price, P2,500, cost, P 1,000 2,500 Total inventory as corrected P271,500 Required: 1. The auditor did not agree with the "corrected" inventory amount of P 271,500. Compute the correct ending inventory amount (show computations) by modifying the corrected balance of P 271, 500 2. The accounts have been closed for 20x6. Therefore, a correcting entry in January 20x7 is needed. Ignoring any income tax effect, give the required correcting entry

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts