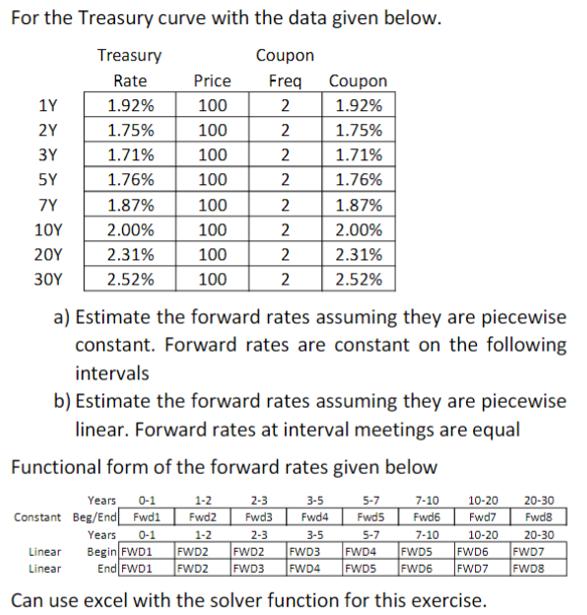

Question: For the Treasury curve with the data given below. Treasury Coupon Rate Freq 1.92% 2 1.75% 2 1.71% 2 1.76% 2 1.87% 2 2.00%

For the Treasury curve with the data given below. Treasury Coupon Rate Freq 1.92% 2 1.75% 2 1.71% 2 1.76% 2 1.87% 2 2.00% 2 2.31% 2 2.52% 2 1Y 2Y 3Y 5Y 7Y 10Y 20Y 3 Price 100 100 100 100 100 100 100 100 Coupon 1.92% 1.75% 1.71% 1.76% 1.87% 2.00% 2.31% 2.52% a) Estimate the forward rates assuming they are piecewise constant. Forward rates are constant on the following intervals Linear Linear b) Estimate the forward rates assuming they are piecewise linear. Forward rates at interval meetings are equal Functional form of the forward rates given below 1-2 3-5 Years 0-1 Constant Beg/End Fwd1 Fwd2 Fwd4 3-5 5-7 Fwd5 5-7 2-3 Fwd3 2-3 Years 0-1 Begin FWD1 End FWD1 FWD2 FWD3 FWD4 FWDS FWD6 FWD7 1-2 FWD2 FWDZ FWD3 FWD4 FWDS FWD6 Can use excel with the solver function for this exercise. 7-10 Fwd6 7-10 10-20 20-30 Fwd7 Fwd8 10-20 20-30 FWD7 FWD8

Step by Step Solution

3.38 Rating (160 Votes )

There are 3 Steps involved in it

To estimate the forward rates based on the given Treasury curve we can assume piecewise constant and ... View full answer

Get step-by-step solutions from verified subject matter experts