Question: For this assignment, it may be faster to setup a table in Excel. If you create a timeline and calculate the pieces in the spreadsheet,

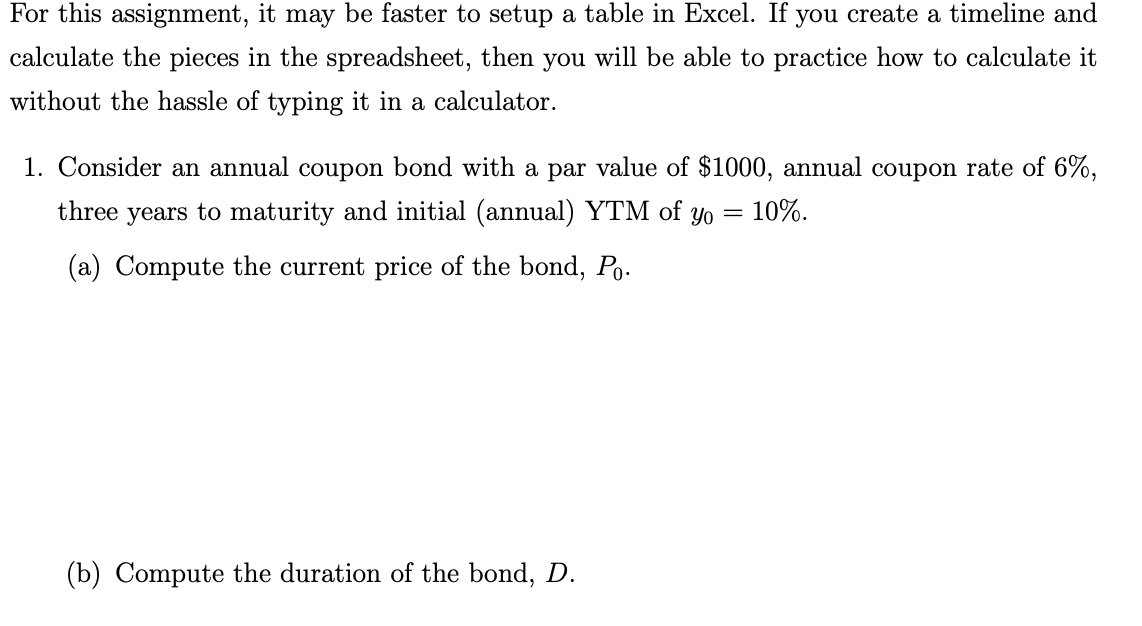

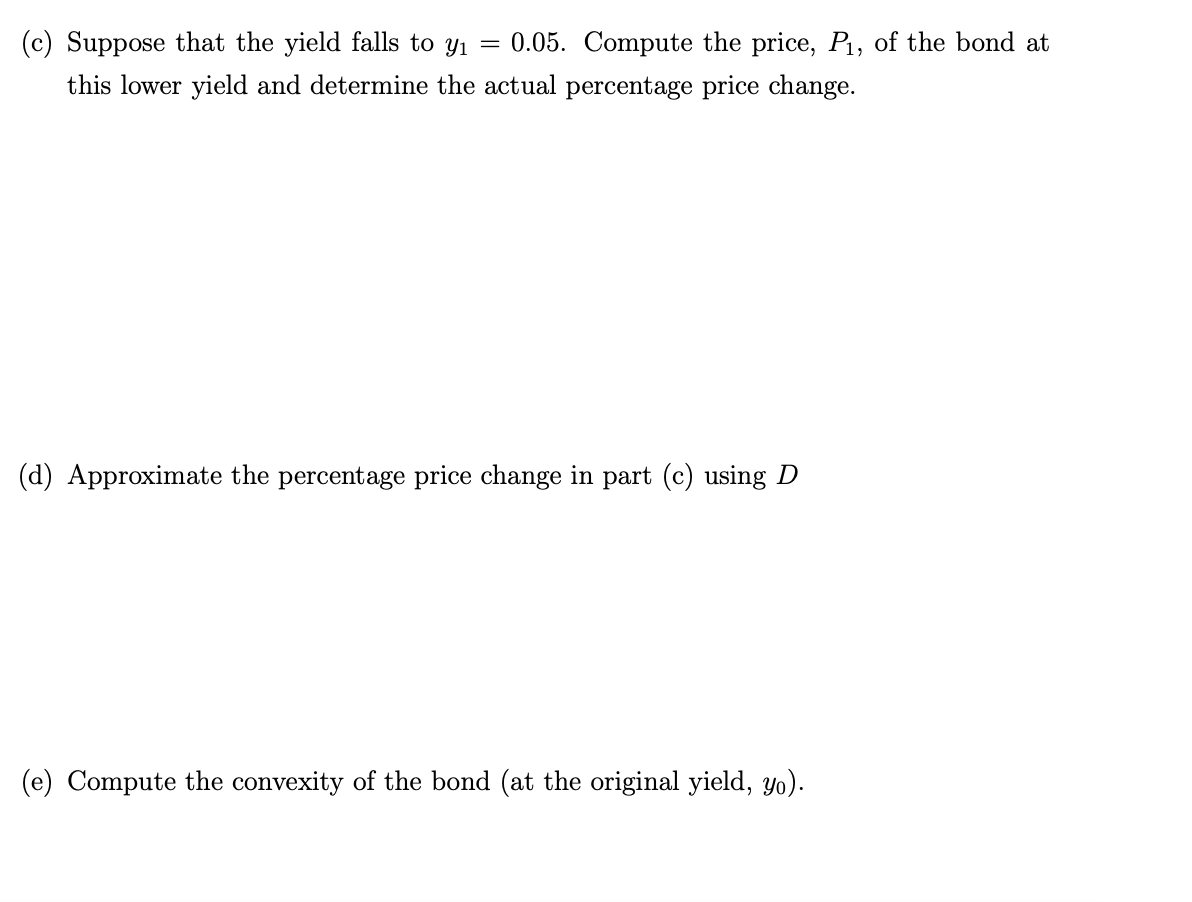

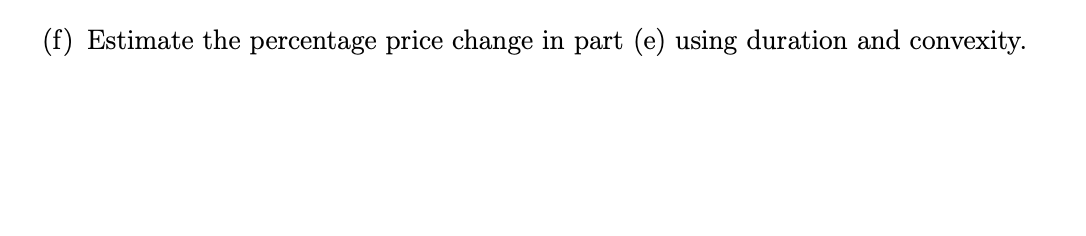

For this assignment, it may be faster to setup a table in Excel. If you create a timeline and calculate the pieces in the spreadsheet, then you will be able to practice how to calculate it without the hassle of typing it in a calculator. 1. Consider an annual coupon bond with a par value of $1000, annual coupon rate of 6%, three years to maturity and initial (annual) YTM of yo 10%. (a) Compute the current price of the bond, Po. (b) Compute the duration of the bond, D. (c) Suppose that the yield falls to y = 0.05. Compute the price, P1, of the bond at this lower yield and determine the actual percentage price change. (d) Approximate the percentage price change in part (c) using D (e) Compute the convexity of the bond (at the original yield, yo). () Estimate the percentage price change in part (e) using duration and convexity

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts