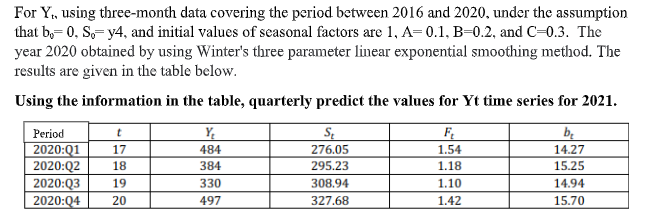

Question: For Y., using three-month data covering the period between 2016 and 2020, under the assumption that bo=0, S=y4, and initial values of seasonal factors are

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock