Question: Formulas for Quiz 4 = required return;=rf + Bi(E[rm] -rf) Bp = wi + w2w + + wnn Pt+1 + Divt+1 Pt Rt +1= Pt

![Formulas for Quiz 4 = required return;=rf + Bi(E[rm] -rf) Bp](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2024/09/66edb8d0c7171_37666edb8d0441e0.jpg)

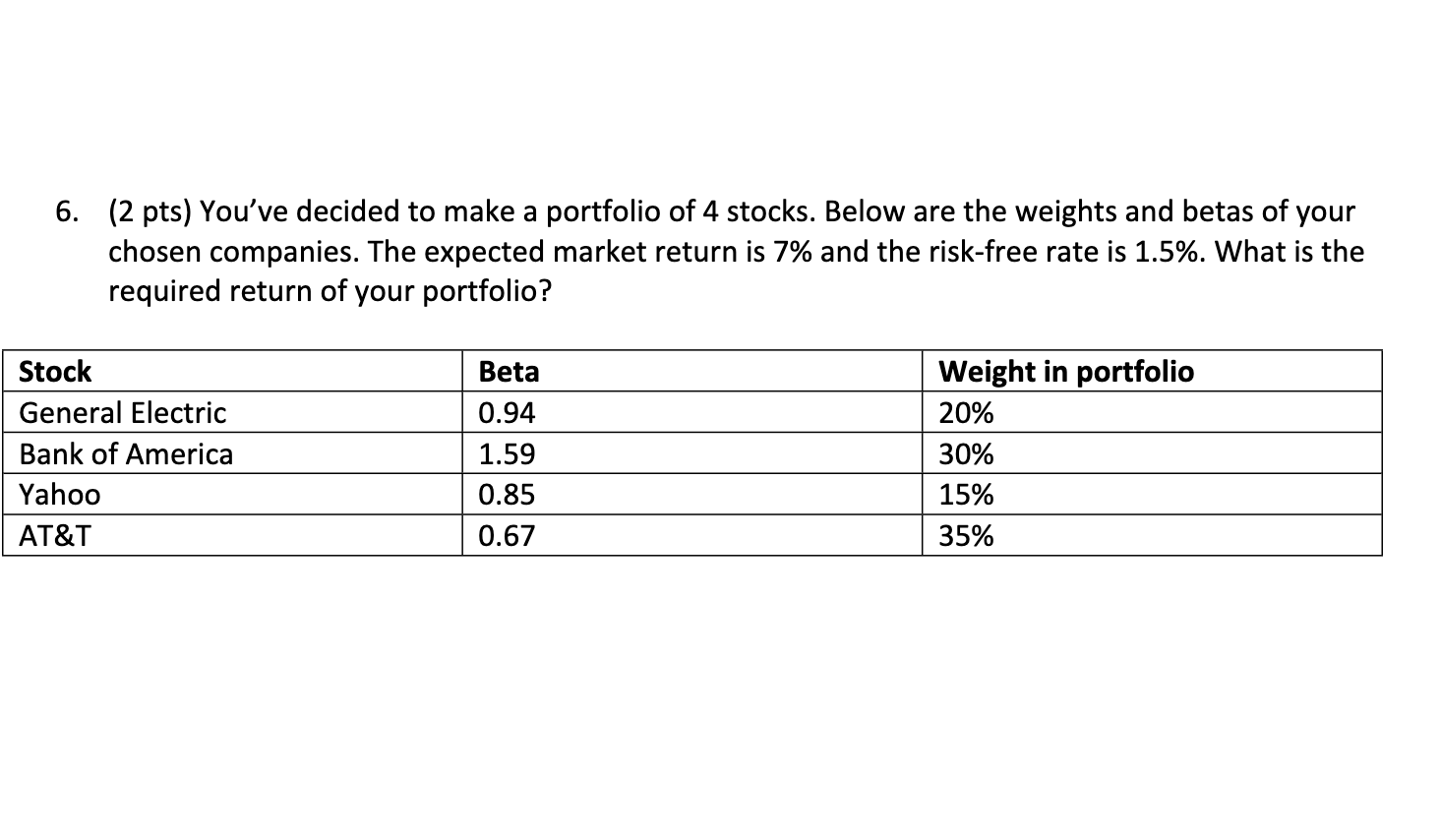

Formulas for Quiz 4 = required return;=rf + Bi(E[rm] -rf) Bp = wi + w2w + + wnn Pt+1 + Divt+1 Pt Rt +1= Pt 1 Variance(?) = (1 - 1)[(R3 R)2 + (R2 R)? + ... + (R R)?] ET - Rt t=2 R= T - 1 = Standard Deviation(o) = V Variance Oi Bi= Pi,m Om NetDebt Equity WACC = rEquity NetDebt + Equity + rDebt: (1 t) NetDebt + Equity 6. (2 pts) You've decided to make a portfolio of 4 stocks. Below are the weights and betas of your chosen companies. The expected market return is 7% and the risk-free rate is 1.5%. What is the required return of your portfolio? Stock General Electric Bank of America Yahoo AT&T Beta 0.94 1.59 0.85 0.67 Weight in portfolio 20% 30% 15% 35%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts