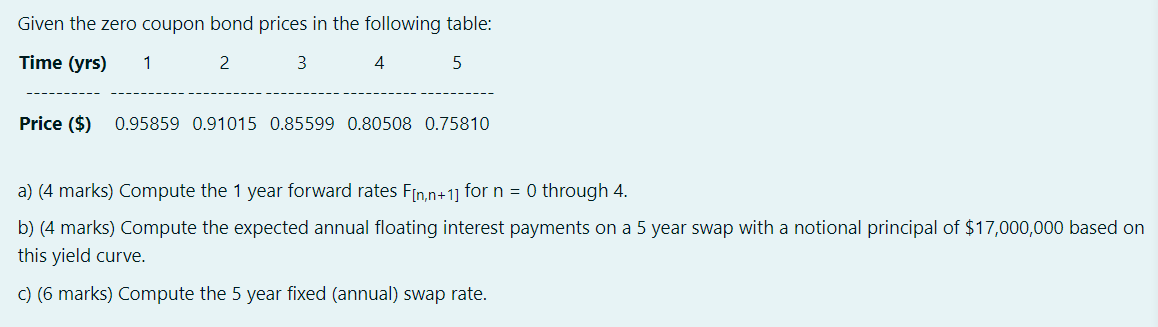

Question: full answer plz 1 Given the zero coupon bond prices in the following table: Time (yrs) 1 2 3 4 5 Price ($) 0.95859 0.91015

full answer plz

full answer plz

1

Given the zero coupon bond prices in the following table: Time (yrs) 1 2 3 4 5 Price ($) 0.95859 0.91015 0.85599 0.80508 0.75810 a) (4 marks) Compute the 1 year forward rates F[n,n+1] for n = 0 through 4. b) (4 marks) Compute the expected annual floating interest payments on a 5 year swap with a notional principal of $17,000,000 based on this yield curve. c) (6 marks) Compute the 5 year fixed (annual) swap rate

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock