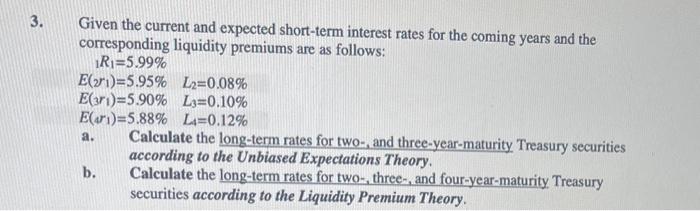

Question: Given the current and expected short-term interest rates for the coming years and the corresponding liquidity premiums are as follows: 1R1=5.99% E(1)=5.95%L2=0.08% E(r1)=5.90%L3=0.10% E(4r1)=5.88%L4=0.12% a.

Given the current and expected short-term interest rates for the coming years and the corresponding liquidity premiums are as follows: 1R1=5.99% E(1)=5.95%L2=0.08% E(r1)=5.90%L3=0.10% E(4r1)=5.88%L4=0.12% a. Calculate the long-term rates for two-, and three-year-maturity Treasury securities according to the Unbiased Expectations Theory. b. Calculate the long-term rates for two-, three-, and four-year-maturity. Treasury securities according to the Liquidity Premium Theory

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock