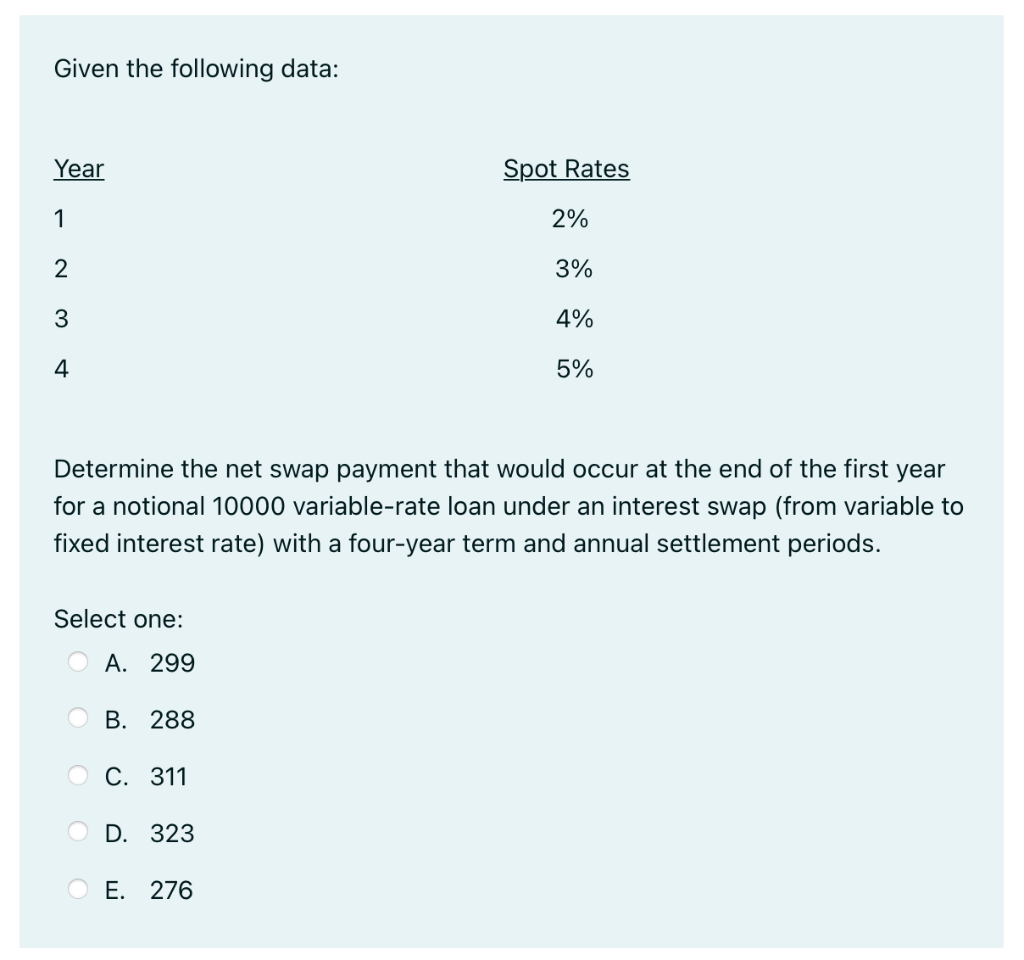

Question: Given the following data: Year Spot Rates 1 2% 2 3% 3 4% 4 5% Determine the net swap payment that would occur at the

Given the following data: Year Spot Rates 1 2% 2 3% 3 4% 4 5% Determine the net swap payment that would occur at the end of the first year for a notional 10000 variable-rate loan under an interest swap (from variable to fixed interest rate) with a four-year term and annual settlement periods. Select one: A. 299 B. 288 O C. 311 D. 323 E. 276

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock