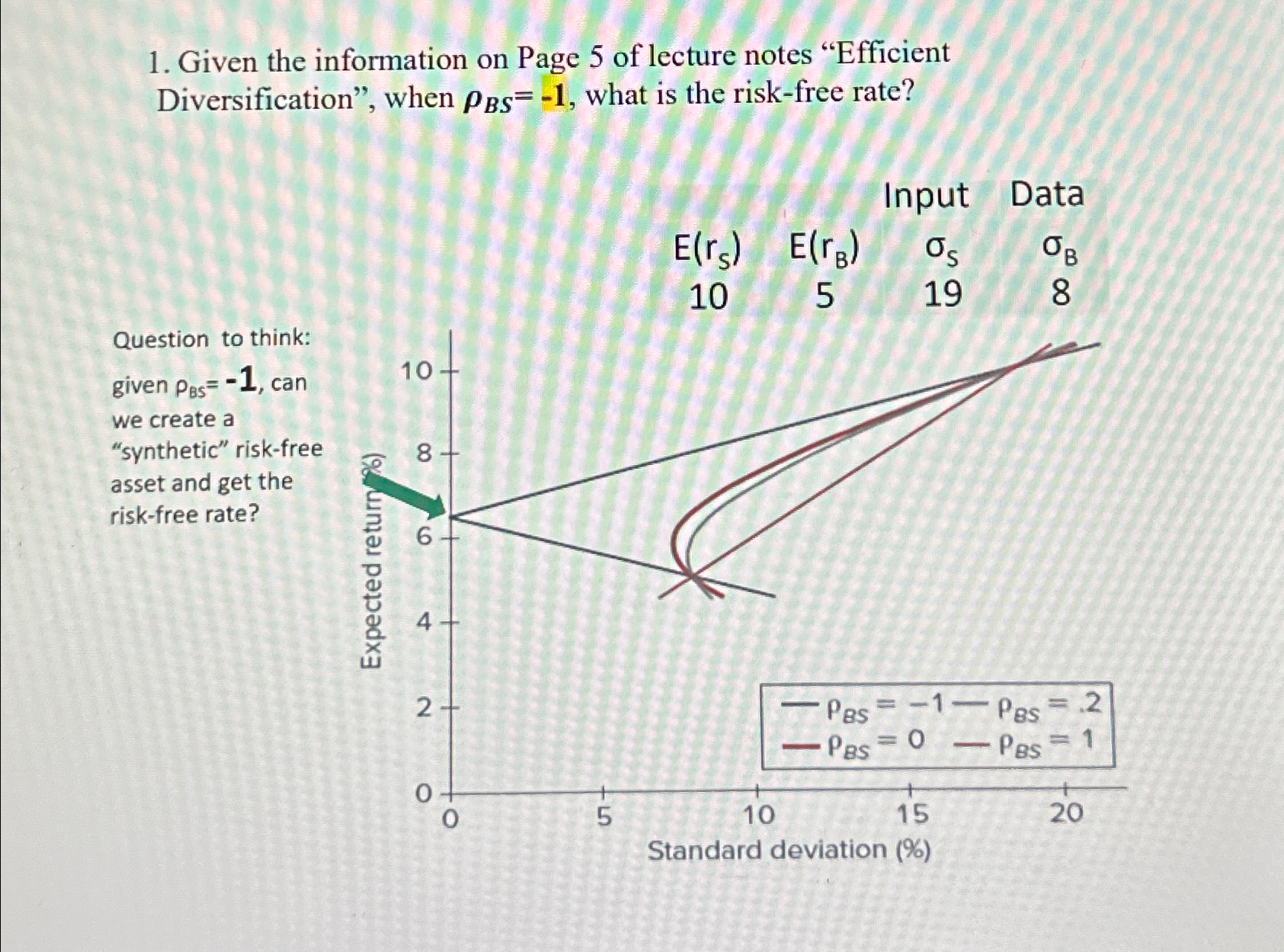

Question: Given the information on Page 5 of lecture notes Efficient Diversification, when B S = - 1 , what is the risk - free rate?

Given the information on Page of lecture notes "Efficient Diversification", when what is the riskfree rate?

Input Data

Question to think: given can we create a "synthetic" riskfree asset and get the riskfree rate?

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock