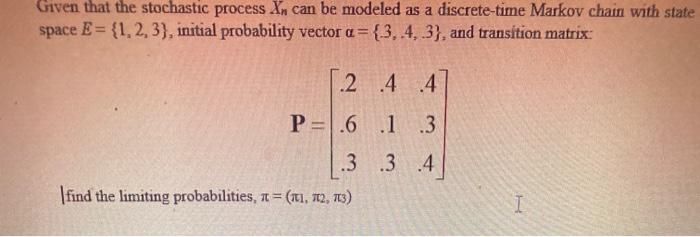

Question: Given that the stochastic process Xn can be modeled as a discrete-time Markov chain with state space E= {1, 2, 3}, initial probability vector

Given that the stochastic process Xn can be modeled as a discrete-time Markov chain with state space E= {1, 2, 3}, initial probability vector a= {3,4, 3}, and transition matrix: %3D 2 4 4 P =.6 .1 .3 .3 3 4 |find the limiting probabilities, a= (x1, 12, 13)

Step by Step Solution

★★★★★

3.44 Rating (157 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

we have to find lmiting probabiities T TT TT2 TI3 012 04 04 we have P 03 03 O 4 O3 we have to ... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock