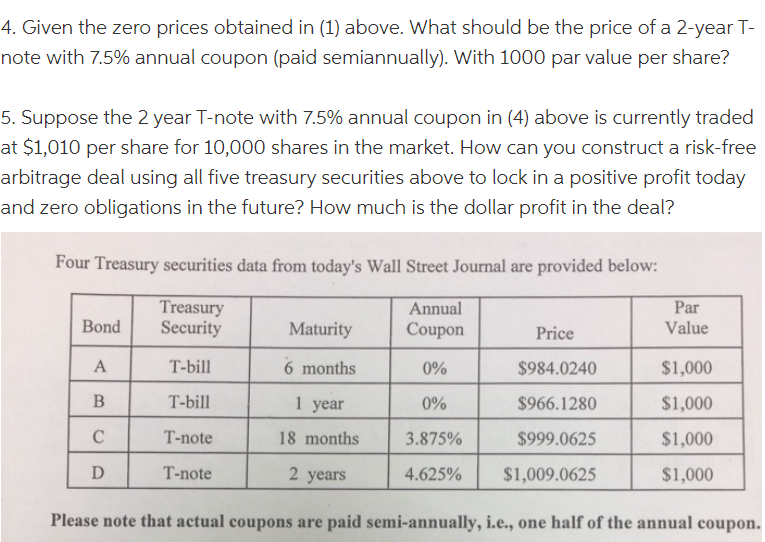

Question: Given the zero prices obtained in (1) above. What should be the price of a 2-year Thote with 7.5% annual coupon (paid semiannually). With 1000

Given the zero prices obtained in (1) above. What should be the price of a 2-year Thote with 7.5% annual coupon (paid semiannually). With 1000 par value per share? 5. Suppose the 2 year T-note with 7.5% annual coupon in (4) above is currently traded at $1,010 per share for 10,000 shares in the market. How can you construct a risk-free arbitrage deal using all five treasury securities above to lock in a positive profit today and zero obligations in the future? How much is the dollar profit in the deal? Four Treasury securities data from today's Wall Street Journal are provided below: Please note that actual coupons are paid semi-annually, i.e., one half of the annual coupon

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts