Health 24-7 is a gym and wellness centre in Camps Bay. The business sells annual gym...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

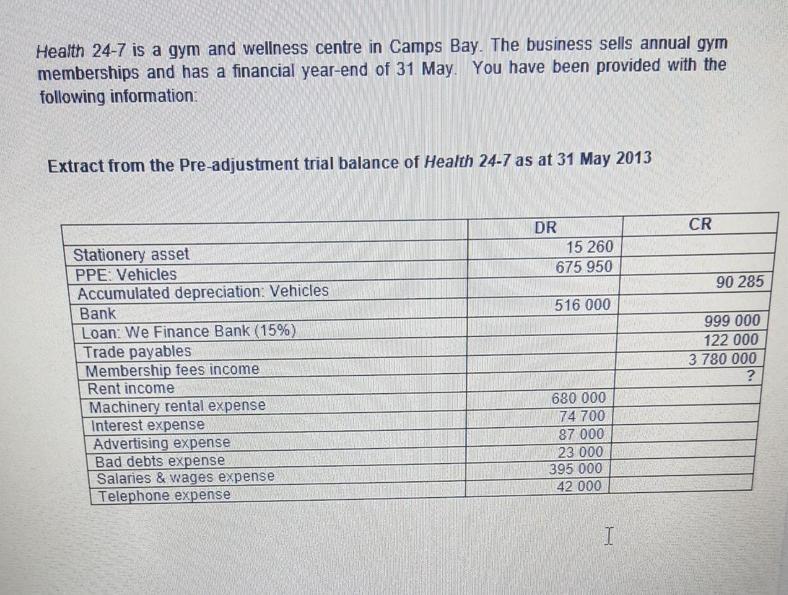

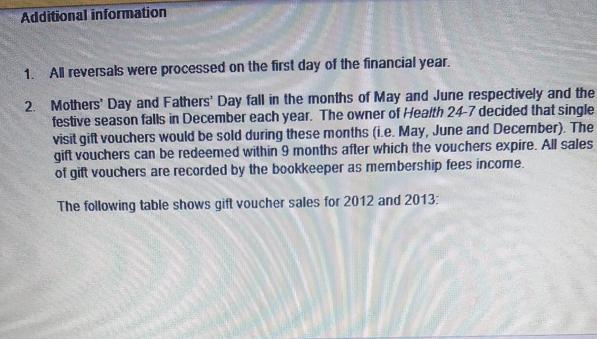

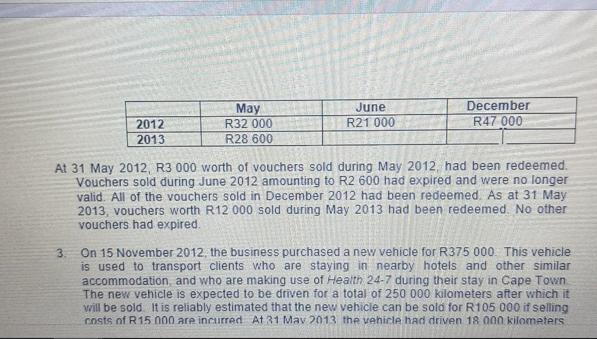

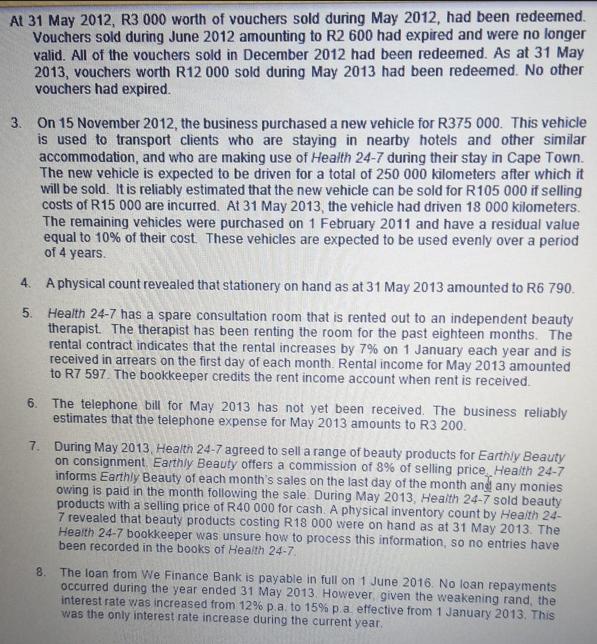

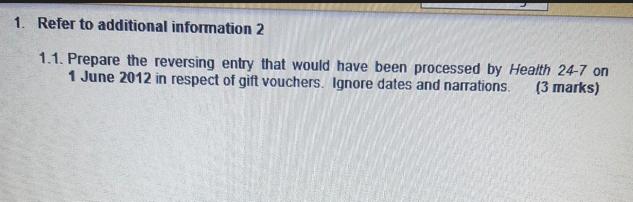

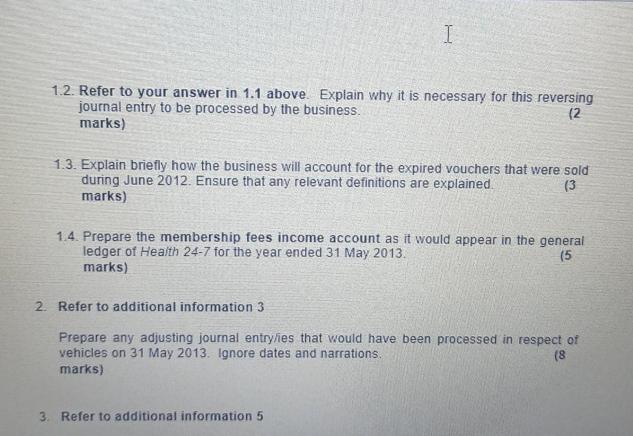

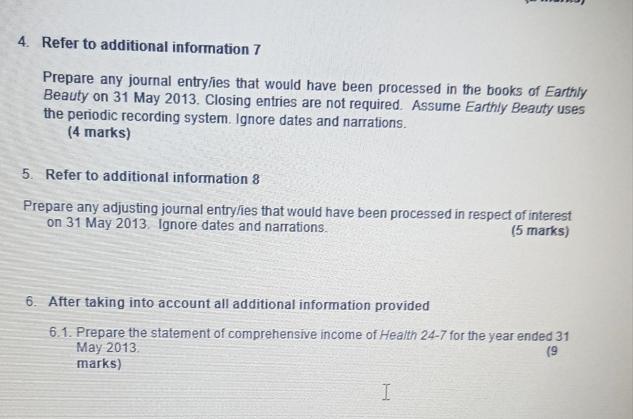

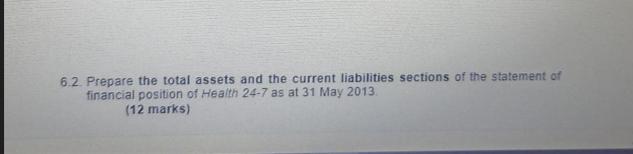

Health 24-7 is a gym and wellness centre in Camps Bay. The business sells annual gym memberships and has a financial year-end of 31 May. You have been provided with the following information: Extract from the Pre-adjustment trial balance of Health 24-7 as at 31 May 2013 Stationery asset PPE: Vehicles Accumulated depreciation: Vehicles Bank Loan: We Finance Bank (15%) Trade payables Membership fees income Rent income Machinery rental expense Interest expense Advertising expense Bad debts expense Salaries & wages expense Telephone expense DR 15 260 675 950 516 000 680 000 74 700 87 000 23 000 395 000 42 000 I CR 90 285 999 000 122 000 3 780 000 ? Additional information 1. All reversals were processed on the first day of the financial year. 2. Mothers' Day and Fathers' Day fall in the months of May and June respectively and the festive season falls in December each year. The owner of Health 24-7 decided that single visit gift vouchers would be sold during these months (i.e. May, June and December). The gift vouchers can be redeemed within 9 months after which the vouchers expire. All sales of gift vouchers are recorded by the bookkeeper as membership fees income. The following table shows gift voucher sales for 2012 and 2013: 2012 2013 May R32 000 R28 600 June R21 000 December R47 000 At 31 May 2012, R3 000 worth of vouchers sold during May 2012, had been redeemed. Vouchers sold during June 2012 amounting to R2 600 had expired and were no longer valid. All of the vouchers sold in December 2012 had been redeemed. As at 31 May 2013, vouchers worth R12 000 sold during May 2013 had been redeemed. No other vouchers had expired. 3. On 15 November 2012, the business purchased a new vehicle for R375 000. This vehicle is used to transport clients who are staying in nearby hotels and other similar accommodation, and who are making use of Health 24-7 during their stay in Cape Town The new vehicle is expected to be driven for a total of 250 000 kilometers after which it will be sold. It is reliably estimated that the new vehicle can be sold for R105 000 if selling costs of R15 000 are incurred At 31 May 2013 the vehicle had driven 18 000 kilometers At 31 May 2012, R3 000 worth of vouchers sold during May 2012, had been redeemed. Vouchers sold during June 2012 amounting to R2 600 had expired and were no longer valid. All of the vouchers sold in December 2012 had been redeemed. As at 31 May 2013, vouchers worth R12 000 sold during May 2013 had been redeemed. No other vouchers had expired. 3. On 15 November 2012, the business purchased a new vehicle for R375 000. This vehicle is used to transport clients who are staying in nearby hotels and other similar accommodation, and who are making use of Health 24-7 during their stay in Cape Town. The new vehicle is expected to be driven for a total of 250 000 kilometers after which it will be sold. It is reliably estimated that the new vehicle can be sold for R105 000 if selling costs of R15 000 are incurred. At 31 May 2013, the vehicle had driven 18 000 kilometers. The remaining vehicles were purchased on 1 February 2011 and have a residual value equal to 10% of their cost. These vehicles are expected to be used evenly over a period of 4 years. 4. A physical count revealed that stationery on hand as at 31 May 2013 amounted to R6 790. Health 24-7 has a spare consultation room that is rented out to an independent beauty therapist. The therapist has been renting the room for the past eighteen months. The rental contract indicates that the rental increases by 7% on 1 January each year and is received in arrears on the first day of each month. Rental income for May 2013 amounted to R7 597. The bookkeeper credits the rent income account when rent is received. 5. 6. The telephone bill for May 2013 has not yet been received. The business reliably estimates that the telephone expense for May 2013 amounts to R3 200. 7. During May 2013, Health 24-7 agreed to sell a range of beauty products for Earthly Beauty on consignment, Earthly Beauty offers a commission of 8% of selling price Health 24-7 informs Earthly Beauty of each month's sales on the last day of the month and any monies owing is paid in the month following the sale. During May 2013, Health 24-7 sold beauty products with a selling price of R40 000 for cash. A physical inventory count by Health 24- 7 revealed that beauty products costing R18 000 were on hand as at 31 May 2013. The Health 24-7 bookkeeper was unsure how to process this information, so no entries have been recorded in the books of Health 24-7. 8. The loan from We Finance Bank is payable in full on 1 June 2016. No loan repayments occurred during the year ended 31 May 2013. However, given the weakening rand, the interest rate was increased from 12% p.a. to 15% p.a. effective from 1 January 2013. This was the only interest rate increase during the current year. 1. Refer to additional information 2 1.1. Prepare the reversing entry that would have been processed by Health 24-7 on 1 June 2012 in respect of gift vouchers. Ignore dates and narrations. (3 marks) I 1.2. Refer to your answer in 1.1 above. Explain why it is necessary for this reversing journal entry to be processed by the business. marks) (2 1.3. Explain briefly how the business will account for the expired vouchers that were sold during June 2012. Ensure that any relevant definitions are explained. marks) (3 1.4. Prepare the membership fees income account as it would appear in the general ledger of Health 24-7 for the year ended 31 May 2013. marks) (5 2. Refer to additional information 3 Prepare any adjusting journal entry/ies that would have been processed in respect of vehicles on 31 May 2013. Ignore dates and narrations. (8 marks) 3. Refer to additional information 5 4. Refer to additional information 7 Prepare any journal entry/ies that would have been processed in the books of Earthly Beauty on 31 May 2013. Closing entries are not required. Assume Earthly Beauty uses the periodic recording system. Ignore dates and narrations. (4 marks) 5. Refer to additional information 8 Prepare any adjusting journal entry/ies that would have been processed in respect of interest on 31 May 2013. Ignore dates and narrations. (5 marks) 6. After taking into account all additional information provided 6.1. Prepare the statement of comprehensive income of Health 24-7 for the year ended 31 May 2013. (9 marks) H 6.2. Prepare the total assets and the current liabilities sections of the statement of financial position of Health 24-7 as at 31 May 2013. (12 marks) Health 24-7 is a gym and wellness centre in Camps Bay. The business sells annual gym memberships and has a financial year-end of 31 May. You have been provided with the following information: Extract from the Pre-adjustment trial balance of Health 24-7 as at 31 May 2013 Stationery asset PPE: Vehicles Accumulated depreciation: Vehicles Bank Loan: We Finance Bank (15%) Trade payables Membership fees income Rent income Machinery rental expense Interest expense Advertising expense Bad debts expense Salaries & wages expense Telephone expense DR 15 260 675 950 516 000 680 000 74 700 87 000 23 000 395 000 42 000 I CR 90 285 999 000 122 000 3 780 000 ? Additional information 1. All reversals were processed on the first day of the financial year. 2. Mothers' Day and Fathers' Day fall in the months of May and June respectively and the festive season falls in December each year. The owner of Health 24-7 decided that single visit gift vouchers would be sold during these months (i.e. May, June and December). The gift vouchers can be redeemed within 9 months after which the vouchers expire. All sales of gift vouchers are recorded by the bookkeeper as membership fees income. The following table shows gift voucher sales for 2012 and 2013: 2012 2013 May R32 000 R28 600 June R21 000 December R47 000 At 31 May 2012, R3 000 worth of vouchers sold during May 2012, had been redeemed. Vouchers sold during June 2012 amounting to R2 600 had expired and were no longer valid. All of the vouchers sold in December 2012 had been redeemed. As at 31 May 2013, vouchers worth R12 000 sold during May 2013 had been redeemed. No other vouchers had expired. 3. On 15 November 2012, the business purchased a new vehicle for R375 000. This vehicle is used to transport clients who are staying in nearby hotels and other similar accommodation, and who are making use of Health 24-7 during their stay in Cape Town The new vehicle is expected to be driven for a total of 250 000 kilometers after which it will be sold. It is reliably estimated that the new vehicle can be sold for R105 000 if selling costs of R15 000 are incurred At 31 May 2013 the vehicle had driven 18 000 kilometers At 31 May 2012, R3 000 worth of vouchers sold during May 2012, had been redeemed. Vouchers sold during June 2012 amounting to R2 600 had expired and were no longer valid. All of the vouchers sold in December 2012 had been redeemed. As at 31 May 2013, vouchers worth R12 000 sold during May 2013 had been redeemed. No other vouchers had expired. 3. On 15 November 2012, the business purchased a new vehicle for R375 000. This vehicle is used to transport clients who are staying in nearby hotels and other similar accommodation, and who are making use of Health 24-7 during their stay in Cape Town. The new vehicle is expected to be driven for a total of 250 000 kilometers after which it will be sold. It is reliably estimated that the new vehicle can be sold for R105 000 if selling costs of R15 000 are incurred. At 31 May 2013, the vehicle had driven 18 000 kilometers. The remaining vehicles were purchased on 1 February 2011 and have a residual value equal to 10% of their cost. These vehicles are expected to be used evenly over a period of 4 years. 4. A physical count revealed that stationery on hand as at 31 May 2013 amounted to R6 790. Health 24-7 has a spare consultation room that is rented out to an independent beauty therapist. The therapist has been renting the room for the past eighteen months. The rental contract indicates that the rental increases by 7% on 1 January each year and is received in arrears on the first day of each month. Rental income for May 2013 amounted to R7 597. The bookkeeper credits the rent income account when rent is received. 5. 6. The telephone bill for May 2013 has not yet been received. The business reliably estimates that the telephone expense for May 2013 amounts to R3 200. 7. During May 2013, Health 24-7 agreed to sell a range of beauty products for Earthly Beauty on consignment, Earthly Beauty offers a commission of 8% of selling price Health 24-7 informs Earthly Beauty of each month's sales on the last day of the month and any monies owing is paid in the month following the sale. During May 2013, Health 24-7 sold beauty products with a selling price of R40 000 for cash. A physical inventory count by Health 24- 7 revealed that beauty products costing R18 000 were on hand as at 31 May 2013. The Health 24-7 bookkeeper was unsure how to process this information, so no entries have been recorded in the books of Health 24-7. 8. The loan from We Finance Bank is payable in full on 1 June 2016. No loan repayments occurred during the year ended 31 May 2013. However, given the weakening rand, the interest rate was increased from 12% p.a. to 15% p.a. effective from 1 January 2013. This was the only interest rate increase during the current year. 1. Refer to additional information 2 1.1. Prepare the reversing entry that would have been processed by Health 24-7 on 1 June 2012 in respect of gift vouchers. Ignore dates and narrations. (3 marks) I 1.2. Refer to your answer in 1.1 above. Explain why it is necessary for this reversing journal entry to be processed by the business. marks) (2 1.3. Explain briefly how the business will account for the expired vouchers that were sold during June 2012. Ensure that any relevant definitions are explained. marks) (3 1.4. Prepare the membership fees income account as it would appear in the general ledger of Health 24-7 for the year ended 31 May 2013. marks) (5 2. Refer to additional information 3 Prepare any adjusting journal entry/ies that would have been processed in respect of vehicles on 31 May 2013. Ignore dates and narrations. (8 marks) 3. Refer to additional information 5 4. Refer to additional information 7 Prepare any journal entry/ies that would have been processed in the books of Earthly Beauty on 31 May 2013. Closing entries are not required. Assume Earthly Beauty uses the periodic recording system. Ignore dates and narrations. (4 marks) 5. Refer to additional information 8 Prepare any adjusting journal entry/ies that would have been processed in respect of interest on 31 May 2013. Ignore dates and narrations. (5 marks) 6. After taking into account all additional information provided 6.1. Prepare the statement of comprehensive income of Health 24-7 for the year ended 31 May 2013. (9 marks) H 6.2. Prepare the total assets and the current liabilities sections of the statement of financial position of Health 24-7 as at 31 May 2013. (12 marks)

Expert Answer:

Answer rating: 100% (QA)

11 Prepare the reversing entry that would have been processed by Health 247 on 1 June 2012 in respect of gift vouchers Ignore dates and narrations 3 marks Membership fees income 3 000 Deferred income ... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

Use the information given below to draw up the Statement of Comprehensive Income for TREK TRADING for the year ended 28 February 2017. Treck Trading Pre Adjustment trial Balance as at 28 February...

-

1. Microcontroller technology (5 marks) Perform a research study on the current state-of-the-art of microcontroller technology. The study shall cover but not limited to, a. Advancement of...

-

Which or the following results has the higher t value for a test of the null hypothesis that the average US passenger car gels 30 miles per gallon? Do not do any calculations; just explain your...

-

Codominance observable effect on the phenotype of a heter neither allele is recessive-both alleles are dominant. 6. Which of the genotypes results in a blood type that provides clear evidence of...

-

An astronomical unit (AU) is equal to the average distance from Earth to the Sun, about 92.9 x 106 mi. A parsec (pc) is the distance at which a length of 1 AU would subtend an angle of exactly 1...

-

Discuss the different methods of improving decision making in organizations. Which of these methods do you expect to find widely used in organizations? Discuss differences in how easy it is to use...

-

The constant in Eq. (15-22b) is \(1.173 \times 10^{-16}\), which agrees with Geankoplis et al. (2018). However, Cussler (2009) and Wankat and Knaebel (2019) use a constant of 7.4 \(\times 10^{-8}\)....

-

Everything about the deal was acceptable to PEMEX and Hyundai in September, 2010. The final negotiated price for 7500 new Hyundai Aguila automobiles was 58 Billion KRW (Korean Won). Payment was...

-

Find the EAR in each of the following cases. Note: Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e . g . , 3 2 . 1 6 . Use 3 6 5 days in a...

-

Capstone Case: Sunrise Bakery Expansion The Sunrise Bakery Corporation was originally founded in Houston, TX in 1991 by Griffin Harris, who currently serves as the company's Chief Executive Officer....

-

Summary Income Statement in $ Sales 5,000,000 EBIT 1,000,000 Int. Expense 40,000 EBT 960,000 Net Income 624,000 Other Financial Information in $ Market Value of LT Debt 500,000 Market Value of Equity...

-

Read the following article from The Marshall Project https://www.themarshallproject.org/2023/08/31/dungeons-and-dragons-texas-death-row-tdcj Ask yourself a few things: 1. What is the Marshall...

-

To avoid being a price taker, you understand that you have to differentiate your product so you face a specific demand curve for your product that is downward sloping. Now you can raise price for...

-

where: Calculate the cost of equity for a hypothetical private firm (rate of return for private investors) under the following circumstances. (8pts): cost of common equity 10% advisory premium 11%...

-

Carla is a 14-year-old female who lives with hermom and 17-year-old brother. She has had annual preventive healthcare from birth and has grown along average height and weight trends. Her medical...

-

Your little sister starts talking about a family vacation thatyou had gone on quite some time ago when she was only 3 years old.She swears she remembers the trip but you are skeptical. How wouldyou...

-

Nevada businessman CalRebuild is Nigel. a. eCar.com has no Nevada dealerships or online salespeople. b. It sells cars on eBay in California and nationwide. c. purchasing automobile, visual issues...

-

What are some of the possible sources of information about a company that could be used for determining the companys competitive stance?

-

Which should be more important to the management of an entity, cash flow or in come? Explain your answer.

-

In 2015, Chin Corp. purchased a piece of land for $2,500,000. In 2018, the land was sold for $3,500,000. Required: Prepare the journal entry to record the sale of Chin Corp's land.

-

Read the part of Note 1 on the use of judgements, estimates, and assumptions. Why is this note included in the financial statements and why is it important? (In your answer discuss why estimates are...

-

Wilmot Real Estate Co. had the following balance sheet at year-end 2015: In early 2016, the company took out a \($200,000\) two-year bank loan to finance new real estate investments. The loan...

-

Presented below is selected financial data for Apple !nc., for the five-year period 2010 to 2014. Required 1. Comment on the relationship between the growth in net sales and the growth in net income...

-

Presented below are the consolidated balance sheets and income statements for Tesco, PLC, the worlds third largest retailer, for the years 2016 and 2015. Tesco is based in the United Kingdom....

Study smarter with the SolutionInn App