Question: Hedging 1 0 2 : The perfect hedge for a processor Setup You are a bread manufacturer. Your production process uses a lot of wheat.

Hedging : The perfect hedge for a processor

Setup

You are a bread manufacturer. Your production process uses a lot of wheat. When your wheat input costs are low, you are happy. But wheat prices can rise, making you unhappy.

You need to ensure a steady supply of wheat for your bread factories. It is now March, and you are worried about having wheat in June. You are short June wheat. To obtain wheat in June, you have three options:

Buy wheat now and store it

Obtain it using forward contracts for June delivery.

Just buy it in June.

The first two options may not be available, or you may usually be able to get a better price by waiting until June. However, the price may change from what you are expecting and you want to ensure that the price you pay in June is what you expect. So you choose option and plan to use the futures market to hedge.

The Hedge

Recall the two steps in hedging:

In March, you place a hedge by taking the opposite position in the futures market from your cash market position.

In June, you unwind the hedge by a offsetting your futures position and b buying wheat.

Let's look at how you do this as a processor. Assume for the moment that the cash and futures prices are both $ By June, the cash and futures prices both increased by $ One wheat futures contract is for bushels exactly what you need in June.

You are short in the cash market in March, so you place a hedge by buying one June futures contract take a long position in the futures market Fill out the first row of the futures column with your position and the price at which you took this position.

In June, you unwind your hedge by first selling one June futures contract at the new price. Fill in the second row under Futures with your position and the price at which you took this position.

To finish unwinding your hedge, you then buy your wheat from the local farmer who has wheat stored from the previous harvest at the June price. This results in a long cash market position. Record this under the second row of the Cash column.

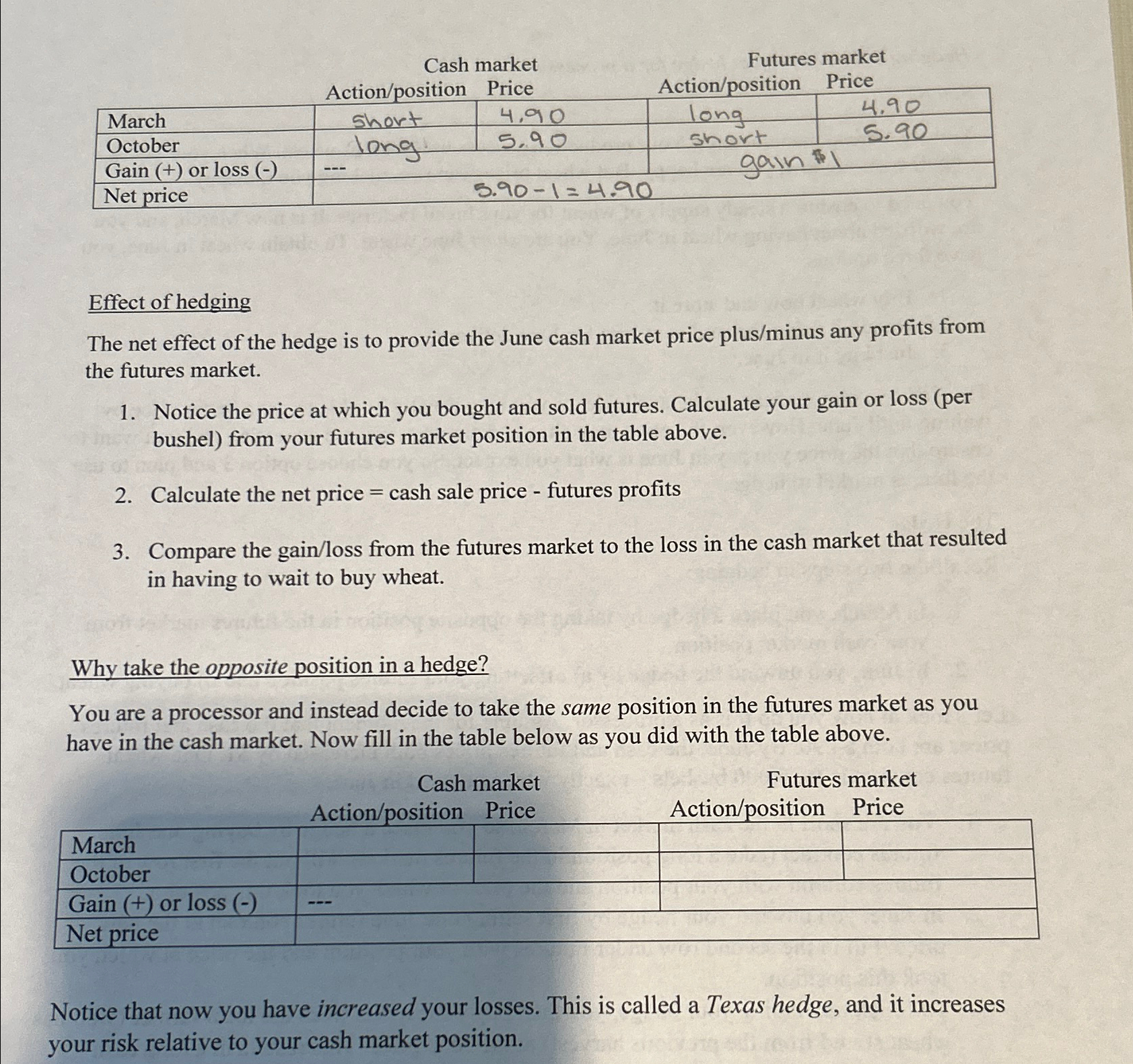

tableFutures marketActionposition market,ActionpositionPrice,,MarchShort,long,Octoberlong,Short,Gain or loss gain Net price,,,,,,

Effect of hedging

The net effect of the hedge is to provide the June cash market price plusminus any profits from the futures market.

Notice the price at which you bought and sold futures. Calculate your gain or loss per bushel from your futures market position in the table above.

Calculate the net price cash sale price futures profits

Compare the gainloss from the futures market to the loss in the cash market that resulted in having to wait to buy wheat.

Why take the opposite position in a hedge?

You are a processor and instead decide to take the same position in the futures market as you have in the cash market. Now fill in the table below as you did with the table above.

Notice that now you have increased your losses. This is called a Texas hedge, and it increases your risk relative to your cash market position.

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock