Question: Hello all! Can anyone could help me on this question please? You observe the following default-free noncallable term structure of interest rates You are a

Hello all! Can anyone could help me on this question please?

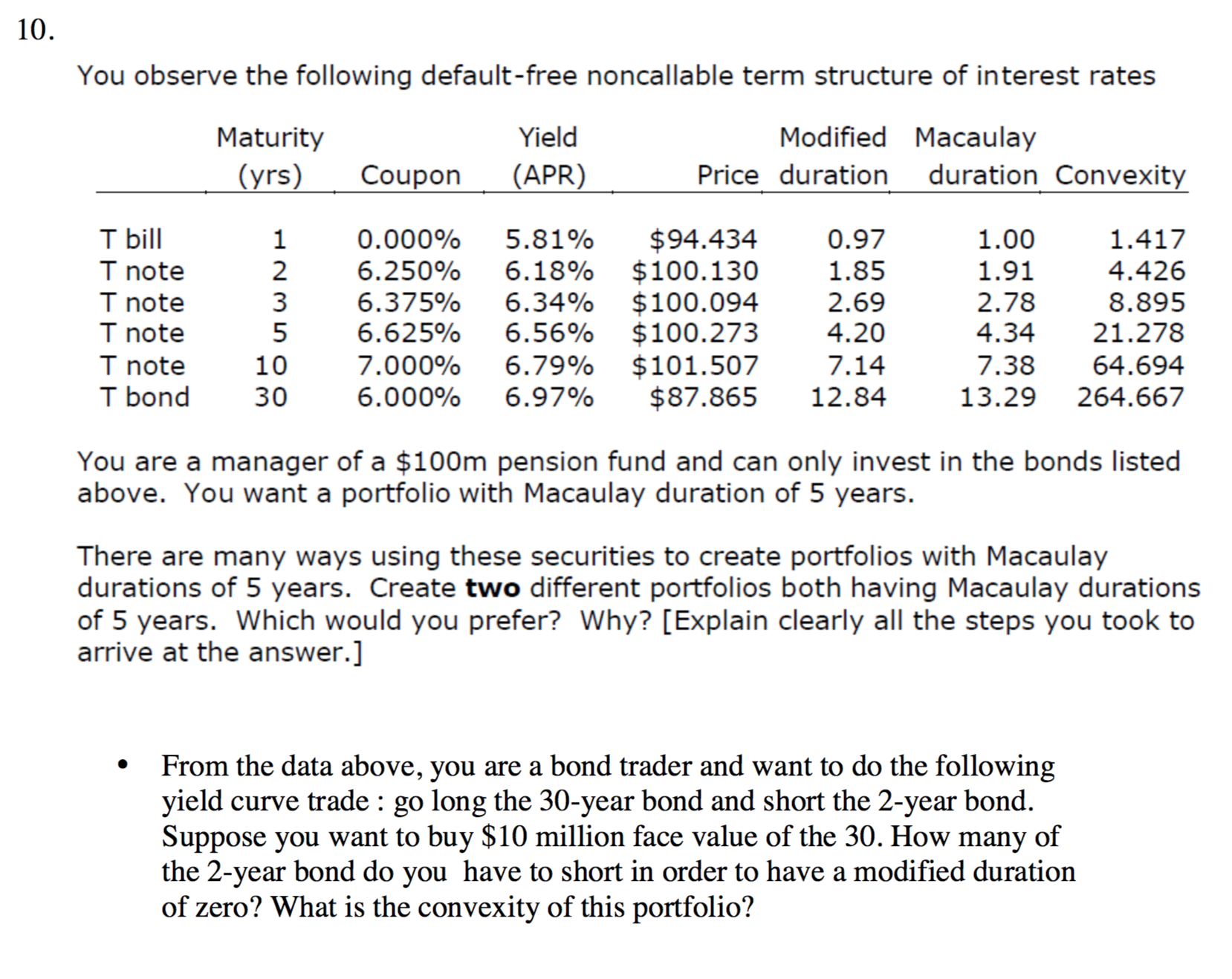

You observe the following default-free noncallable term structure of interest rates You are a manager of a $100m pension fund and can only invest in the bonds listed above. You want a portfolio with Macaulay duration of 5 years. There are many ways using these securities to create portfolios with Macaulay durations of 5 years. Create two different portfolios both having Macaulay durations of 5 years. Which would you prefer? Why? [Explain clearly all the steps you took to arrive at the answer.] From the data above, you are a bond trader and want to do the following yield curve trade : go long the 30-year bond and short the 2-year bond. Suppose you want to buy $10 million face value of the 30. How many of the 2-year bond do you have to short in order to have a modified duration of zero? What is the convexity of this portfolio? You observe the following default-free noncallable term structure of interest rates You are a manager of a $100m pension fund and can only invest in the bonds listed above. You want a portfolio with Macaulay duration of 5 years. There are many ways using these securities to create portfolios with Macaulay durations of 5 years. Create two different portfolios both having Macaulay durations of 5 years. Which would you prefer? Why? [Explain clearly all the steps you took to arrive at the answer.] From the data above, you are a bond trader and want to do the following yield curve trade : go long the 30-year bond and short the 2-year bond. Suppose you want to buy $10 million face value of the 30. How many of the 2-year bond do you have to short in order to have a modified duration of zero? What is the convexity of this portfolio

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts