Question: Hello, Can you help please? My paper is about imaginary, nonprofit primary health health clinic serving unprivileged who cannot pay for doctor's visits or prescriptions.

Hello,

Can you help please?

My paper is about imaginary, nonprofit primary health health clinic serving unprivileged who cannot pay for doctor's visits or prescriptions. Clinic performs office visits, prescriptions (excluding opioids), basics labs and simple X-rays in the clinic. The clinic also provide diabetic education to those in needs as well as provide free diabetic meters and testing supplies. The clinic is located in Chicago neighborhood, employ about 20 employees, excluding physicians who volunteer one day per week for the clinic.

There is no fee for the services.

Balance Sheet (Norwicki, 2018, pp. 51-54)

Can you help me make a balance sheet? something that I could build my own answer on ? something to show a hypothetical but realistic balance sheet for my clinic.

This balance sheet should cover two years, the current year and the subsequent year. The balance sheet should show a vivid increase in total net assets.

Then I have to explain the entries in this balance sheet, and calculate the assets for both years.

I include the pages from the book (51-54)

Can you help?

Thank you.

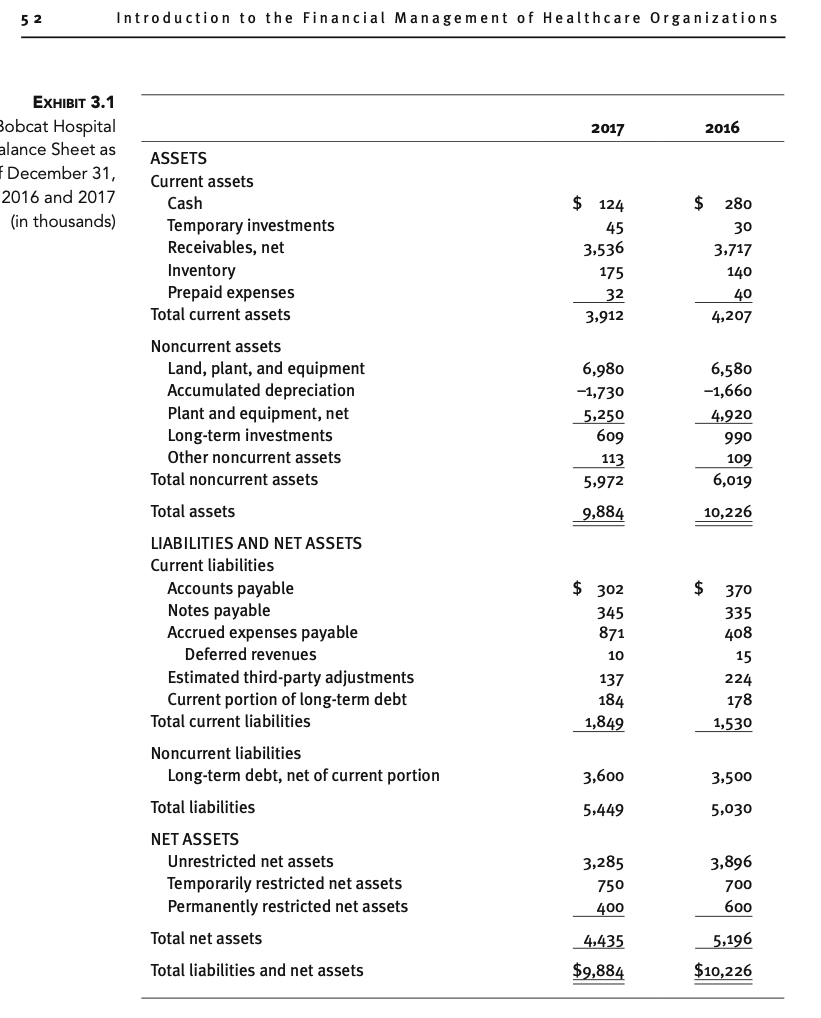

BALANCE SHEET The balance sheet shows the organization's financial position at a specific point in time, typically at the end of an accounting period (see exhibit 3.1). The balance sheet presents the organization's assets, liabilities, and net assets (or shareholders' equity in for-profit orga- nizations) and its relationships, which are reflected in the following accounting equation: Assets = Liabilities + Net Assets Assets are economic resources that provide or are expected to provide benefit to the organization. Current assets are economic resources that have a life of less than one year (i.e., the organization expects to consume them within one year). Current assets are listed on the balance sheet in order of liquidity. Cash is money on hand and in the bank that the organization can access immediately. Temporary investments consist of money placed in securities with maturities up to one year, such as commodities and options. The category receivables, net-made up of patient accounts receivable, net of allowances for contractual allowances, charity care, and bad debt-represents money due to the organization from patients and third parties for services already provided. Inventory is the cost of food, fuel, drugs, and other supplies purchased by the hospital but not yet used or consumed. Prepaid expenses are expenditures made by the hospital for goods and services not yet consumed or used in hospital operations (sometimes referred to as deferred expenses), such as rent and insurance premiums. Noncurrent assets are economic resources that have a life of one year or more (i.e., the organization expects to consume them over a span longer than one year). Plant and equipment, net consists of economic resources, such as land, buildings, and equipment, minus the amount that has been depreciated over the life of the buildings and equipment (which is called accumulated depreciation). Long-term investments are economic resources that the hospital owns, such as corporate bonds and government securities, and intends5 2 Introduction to the Financial Management of Healthcare Organizations EXHIBIT 3.1 obcat Hospital 2017 2016 lance Sheet as ASSETS December 31, Current assets 2016 and 2017 Cash $ 124 $ 280 (in thousands) Temporary investments 45 30 Receivables, net 3,536 3,717 Inventory 175 140 Prepaid expenses 32 40 Total current assets 3,912 4,207 Noncurrent assets Land, plant, and equipment 6,980 6,580 Accumulated depreciation -1,730 -1,660 Plant and equipment, net 5,250 4,920 Long-term investments 609 990 Other noncurrent assets 113 109 Total noncurrent assets 5,972 6,019 Total assets 9,884 10,226 LIABILITIES AND NET ASSETS Current liabilities Accounts payable $ 302 $ 370 Notes payable 345 335 Accrued expenses payable 871 408 Deferred revenues 10 15 Estimated third-party adjustments 137 224 Current portion of long-term debt 184 178 Total current liabilities 1,849 1,530 Noncurrent liabilities Long-term debt, net of current portion 3,600 3,500 Total liabilities 5,449 5,030 NET ASSETS Unrestricted net assets 3,285 3,896 Temporarily restricted net assets 750 700 Permanently restricted net assets 400 600 Total net assets 4,435 5,196 Total liabilities and net assets $9,884 $10,226Chapter 3: Financial Analysis and Management Reporting 53 to hold for more than one year. Other noncurrent assets include assets limited as to use (by contracts with outside parties) and goodwill, which represents the amount above fair market value based on an entity's future earning potential. Liabilities are economic obligations, or debts, of the organization. Current liabili liabilities ties are economic obligations, or debts, that are due within one year. Accounts payable Economic obligations, are amounts the organization owes to suppliers and other trade creditors for merchandise or debts, of the and services purchased from them, but for which the organization has not yet paid. Notes organization. payable are short-term obligations for which a formal contract has been signed, such as a short-term loan. Accrued expenses payable are liabilities for expenses that have been incurred by the hospital but for which the hospital has not yet paid, such as compensation to employees. Deferred revenue is money received by the hospital but not yet earned by the hospital, such as registration fees for an educational program not yet provided. Estimated third-party adjustments are approximations of how much money the organization will be required to return to third-party payers due to overpayments to the organization. Cur- rent portion of long-term debt is the amount of the organization's long-term debt (not including interest) that is expected to be paid within one year. Long-term liabilities are economic obligations, or debts, that are due in more than one year. Long-term debt, net of current portion is an economic obligation, or debt, that is due in more than one year, minus the amount that is due within one year. Net assets is the current AICPA-approved term for the difference between assets net assets and liabilities in not-for-profit healthcare organizations and represents the owner's (com- The difference between munity's or religion's) and others' (donors external to the organization) financial interest in assets and liabilities the organization. Unrestricted net assets include net assets that have not been externally in a not-for-profit organization, which restricted by donors or grantors, such as the excess of revenues to expenses from operations. represents the owner's Unrestricted net assets include net assets that are contractually limited by the governing and others' financial body, such as proceeds of debt issues, funds deposited with a trustee and limited to use by interests in the an indenture agreement, and funds set aside under self-insurance arrangements and statu- organization. tory reserve requirements. Temporarily restricted net assets include donor-restricted net assets that the organization can use for the donor's specific purpose after the organization has met the donor's restriction, such as the passage of time or an action by the organiza- tion. Permanently restricted net assets include donor-restricted net assets with restrictions that never expire, such as endowment funds. In fiscal years beginning after December 15, 2017, organizations will be expected to present net assets in two categories instead of three: "net assets without donor restrictions" and "net assets with donor restrictions." Generally accepted accounting principles (GAAP) will require organizations to disclose the amount, purpose, and type of board restrictions for net assets without donor restrictions, and GAAP will require organizations to disclose the nature and amount of donor restrictions for net assets with donor restrictions (Connor and Mosrie 2016).5 4 Introduction to the Financial Management of Healthcare Organizations Shareholders' equity is the current AICPA-approved term for the difference between assets and liabilities in for-profit healthcare organizations; it represents the ownership interest of stockholders in the organization. Shareholders' equity is also called stockholders' equity, owners equity, or net worth and comprises common stock and retained earnings. Common stock is money invested in the organization by its owners. Retained earnings result from income earned by the organization from operations minus dividends (distributions of earn- ings paid to stockholders based on the number of shares of stock owned). Explanatory notes for the balance sheet and the other financial statements should identify extraordinary events, as well as certain required provisions, and should be presented following the financial statements. In fiscal years beginning after December 15, 2018, public organizations and not-for-profit organizations that have issued securities that are traded or listed on an exchange or over-the-counter market will be expected to present the effects of all leases on the balance sheet (the deadline for all other organizations is fiscal years begin- ning after December 15, 2019). ASU 2016-02, Leases (Topic 842) intends to increase transparency and comparability among organizations by requiring all organizations, not just healthcare organizations, to present the effects of both financial leases and operating leases on the balance sheet (historically, organizations have not presented the effects of operating leases on the balance sheet). The organization should recognize a liability (lease payments) and a right-of-use asset on the balance sheet (Connor and Mosrie 2016)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts