Question: Hello, I don't understand the response, a) when we write down the optimal allocation function, gamma is supposed to by = 1 with the information

Hello,

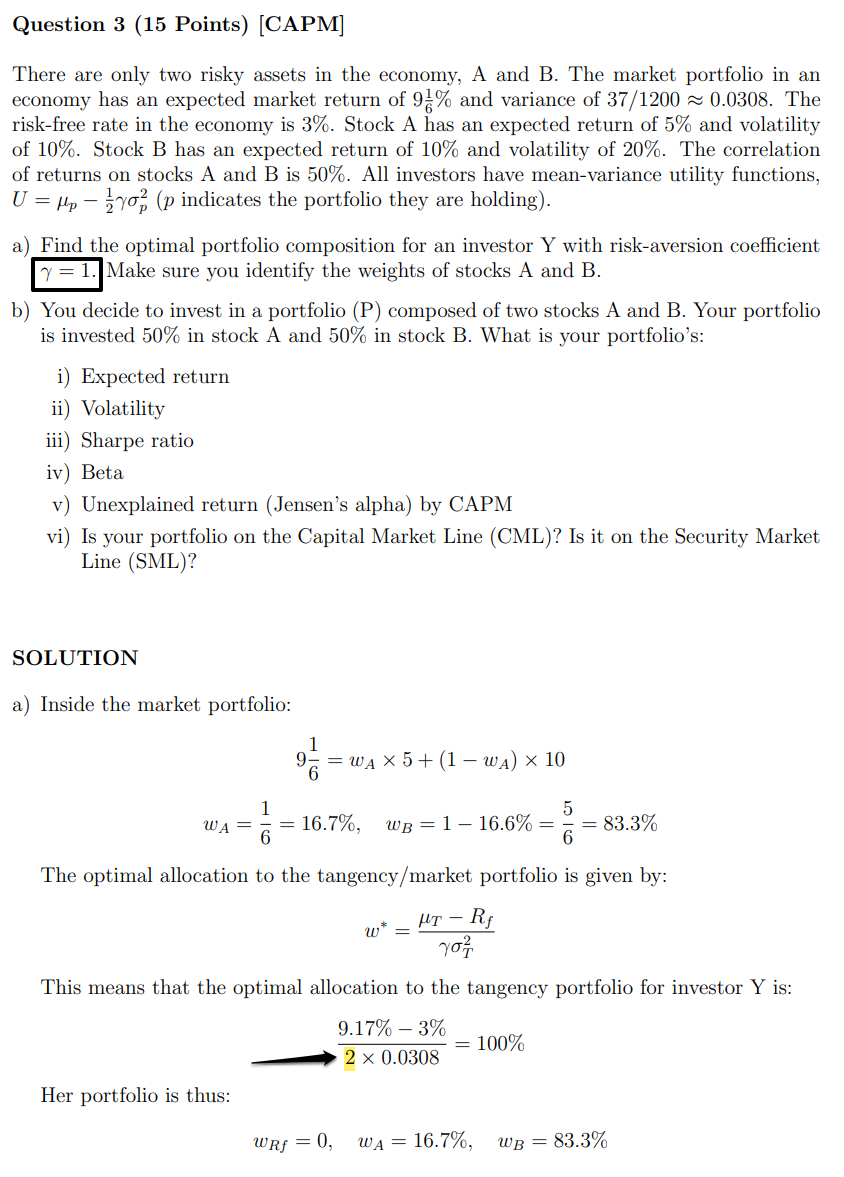

I don't understand the response, a) when we write down the optimal allocation function, gamma is supposed to by = 1 with the information provided in the question. Why do we have a 2 in the equation? Is it gamma or something else ?

Thank you for your time

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock