Question: Hello, Please answer ONLY the first question. I will post the second one in another request. Please make sure to provide how you calculate the

Hello,

Please answer ONLY the first question. I will post the second one in another request. Please make sure to provide how you calculate the problem. Also, please answer the question manually without using Excel.

Thank you

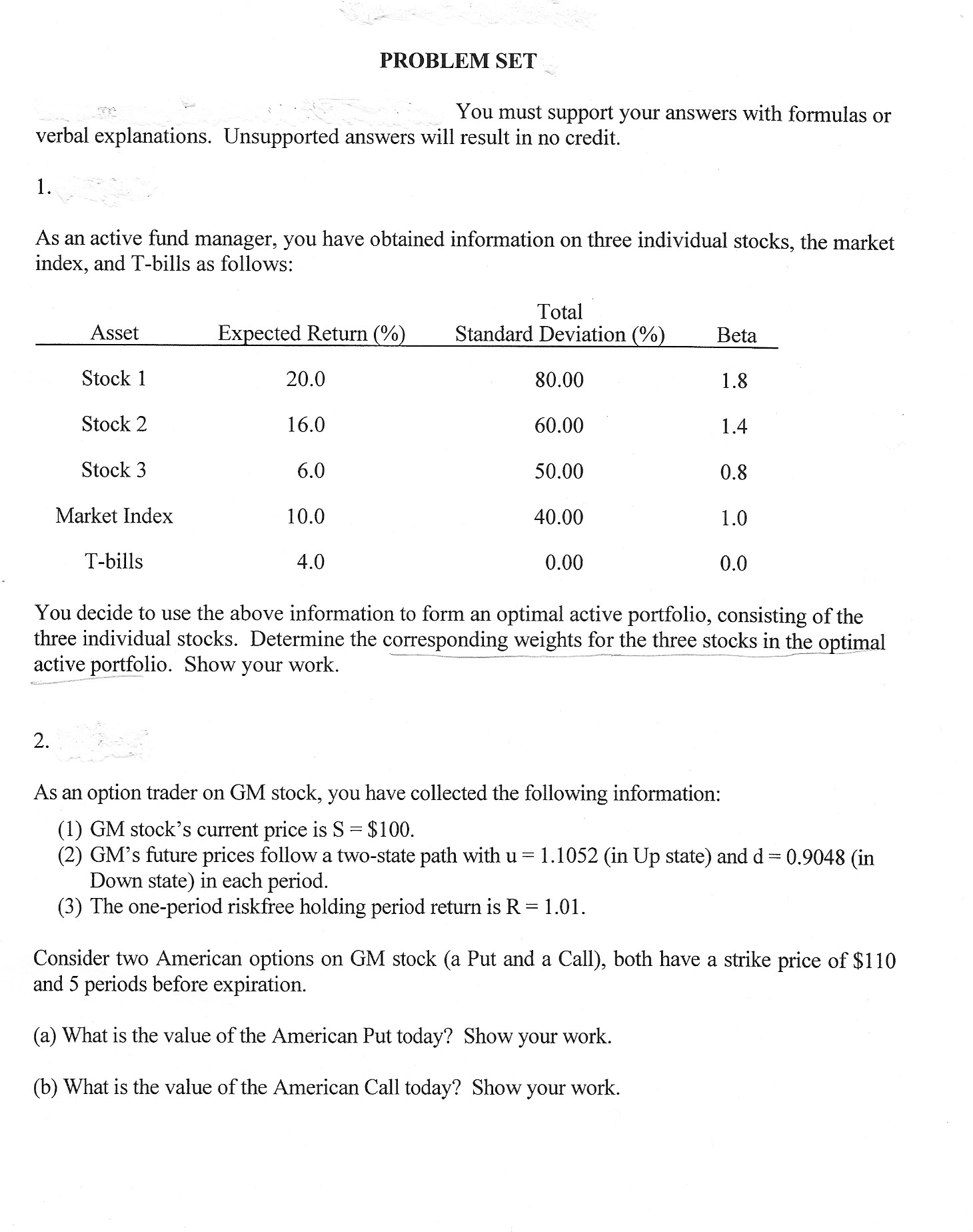

PROBLEM SET ' _ 7 _ _ You must support your answers with formulas or verbal explanations. Unsupported answers will result in no credit. 1. As an active fund manager, you have obtained information on three individual stocks, the market index, and Tbills as follows: Asset Expected Return ! %1 Standard 110(etgiation (%! Beta Stock 1 20.0 80.00 1.8 Stock 2 16.0 60.00 ' 1.4 Stock 3 6.0 50.00 0.8 Market Index 10.0 40.00 1.0 T-bills 4.0 0.00 0.0 You decide to use the above information to form an optimal active portfolio, consisting of the three individual stocks. Determine the corresponding weights for the @3355)?\" in the optimal activeportfolio. Show your work. __..,,..- mi' 2. As an option trader on GM stock, you have collected the following information: (1) GM stock's current price is S = $100. (2) GM's future prices follow a two-state path with u = 1.1052 (in Up state) and d = 0.9048 (in Down state) in each period. (3) The oneperiod riskfi'ee holding period return is R = 1.01. Consider two American options on GM stock (a Put and a Call), both have a strike price of $110 and 5 periods before expiration. (a) What is the value of the American Put today? Show your work. (b) What is the value of the American Call today? Show your work

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts