Question: Help for 7 and 8 Use the formula for approximate modified duration to calculate the duration of the 5%, 10year bond for 10bps change in

Help for 7 and 8

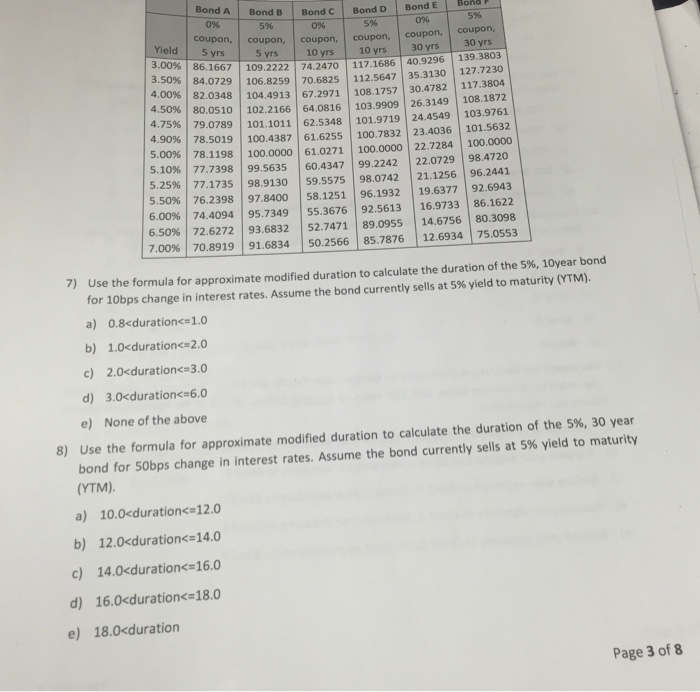

Use the formula for approximate modified duration to calculate the duration of the 5%, 10year bond for 10bps change in interest rates. Assume the bond currently sells at 5% yield to maturity (YTM). Use the formula for approximate modified duration to calculate the duration of the S%, 30 year bond for 50bps change in interest rates. Assume the bond currently sells at 5% yield to maturity (YTM)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock