Question: Help here. Two assets. A and B with independent returns R, and Ry, are available to investors. The retum on Asset A is assumed to

Help here.

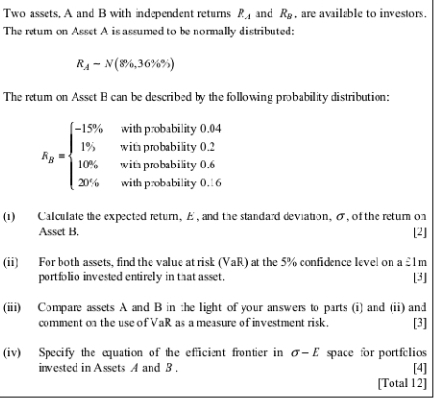

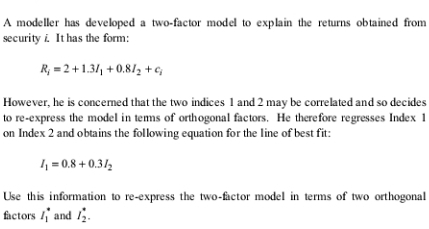

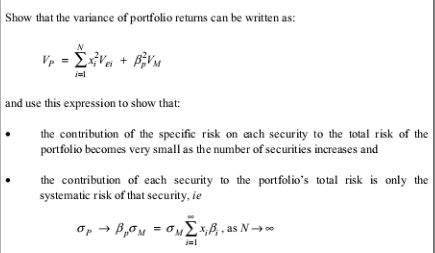

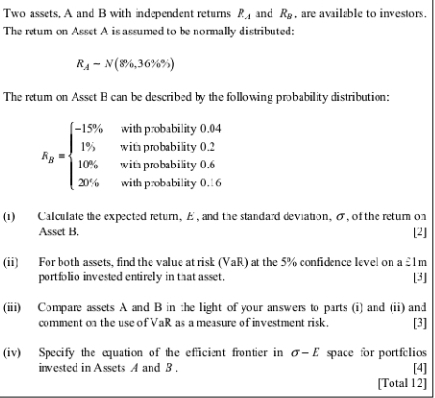

Two assets. A and B with independent returns R, and Ry, are available to investors. The retum on Asset A is assumed to be normally distributed: RA - N(86,36%%) The retum on Asset B can be described by the following probability distribution: -15% with probability 0.04 1% with probability 0.2 10% with probability 0.6 20% with probability 0.16 (1) Calculate the expected return, A, and the standard deviation, of, of the return on Asset B. 121 (ii) For both assets, find the value at risk (Val) at the 5% confidence level on a Elm portfolio invested entirely in that asset. (mi) Compare assets A and B in the light of your answers to parts (i] and (ii) and comment on the use of Vak as a measure of investment risk. [3] (iv) Specify the equation of the efficient frontier in o-E space for portfolios invested in Assets A and 3. [4] [Total 12]A modeller has developed a two-factor model to explain the returns obtained from security & It has the form: R, =2+1.3/, +0.8/2+ G However, he is concerned that the two indices I and 2 may be correlated and so decides to re-express the model in terms of orthogonal factors. He therefore regresses Index I on Index 2 and obtains the following equation for the line of best fit: / = 0.8+0.3/2 Use this information to re-express the two-factor model in terms of two orthogonal factors /, and /2-Show that the variance of portfolio returns can be written as; N + and use this expression to show that: the contribution of the specific risk on each security to the total risk of the portfolio becomes very small as the number of securities increases and the contribution of each security to the portfolio's total risk is only the systematic risk of that security, ie x. B, . as N -() A portfolio P consists of a assets, with a proportion x, invested in asset i. /=12.....# (so that >x, =1) Derive a formula for the portfolio beta, Sp . in terms of the individual bets for each asset. [2] (ibj The annual returns Rp on this portfolio can be assumed to conform to the single-index model of asset returns. Write down an equation defining this model and show that: van( RP) = = var( Ry ) + var(ep) where ap denotes the component of the portfolio return that is independent of movements in the market. [3] Explain why the specific risk var(8p) is sometimes referred to as the "diversifiable risk", giving an algebraic justification for your answer. (4] (iv) Discuss the following statement: "A portfolio with a beta of zero is equivalent to a risk-free asset." (2] [Total 11]

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts