Question: help please Use the following information for the next 2 questions: Given that: S = $15; X = $13. T = 73 days; Rf= 5%;

help please

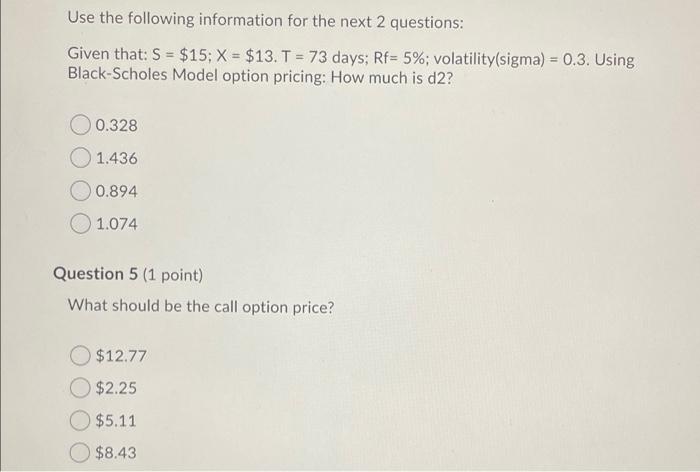

Use the following information for the next 2 questions: Given that: S = $15; X = $13. T = 73 days; Rf= 5%; volatility(sigma) = 0.3. Using Black-Scholes Model option pricing: How much is d2? 0.328 1.436 0.894 1.074 Question 5 (1 point) What should be the call option price? $12.77 $2.25 $5.11 $8.43

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock