Question: help with part 2 and 3 please Intro You manage a stock portfolio worth $49 million with a beta of 1.2. You want to hedge

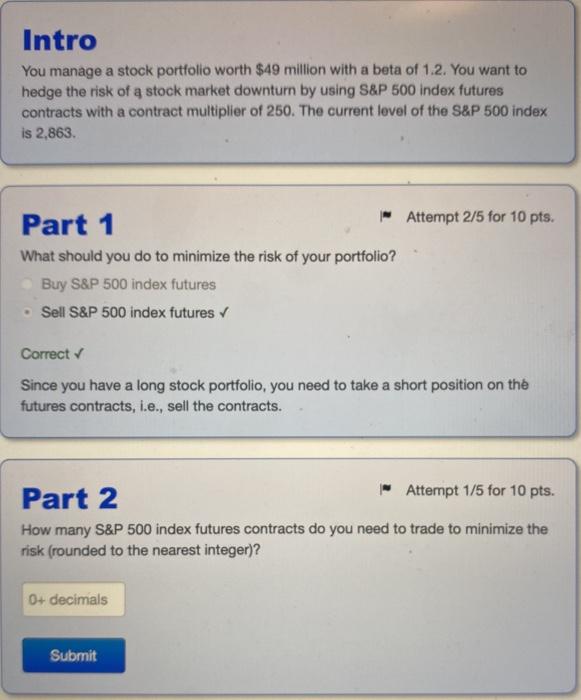

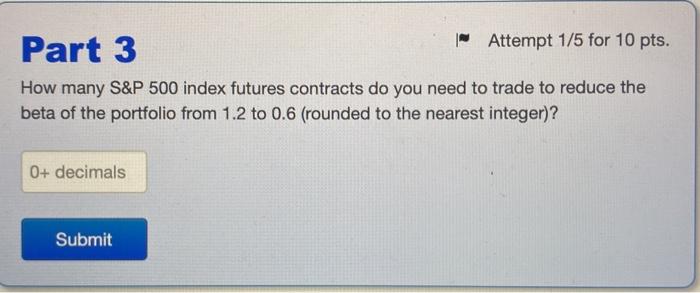

Intro You manage a stock portfolio worth $49 million with a beta of 1.2. You want to hedge the risk of a stock market downturn by using S&P 500 index futures contracts with a contract multiplier of 250. The current level of the S&P 500 index is 2,863 Part 1 - Attempt 2/5 for 10 pts. What should you do to minimize the risk of your portfolio? Buy S&P 500 index futures Sell S&P 500 index futures Correct Since you have a long stock portfolio, you need to take a short position on the futures contracts, i.e., sell the contracts. Part 2 - Attempt 1/5 for 10 pts. How many S&P 500 index futures contracts do you need to trade to minimize the risk (rounded to the nearest integer)? 0+ decimals Submit Part 3 - Attempt 1/5 for 10 pts. How many S&P 500 index futures contracts do you need to trade to reduce the beta of the portfolio from 1.2 to 0.6 (rounded to the nearest integer)? 0+ decimals Submit

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts