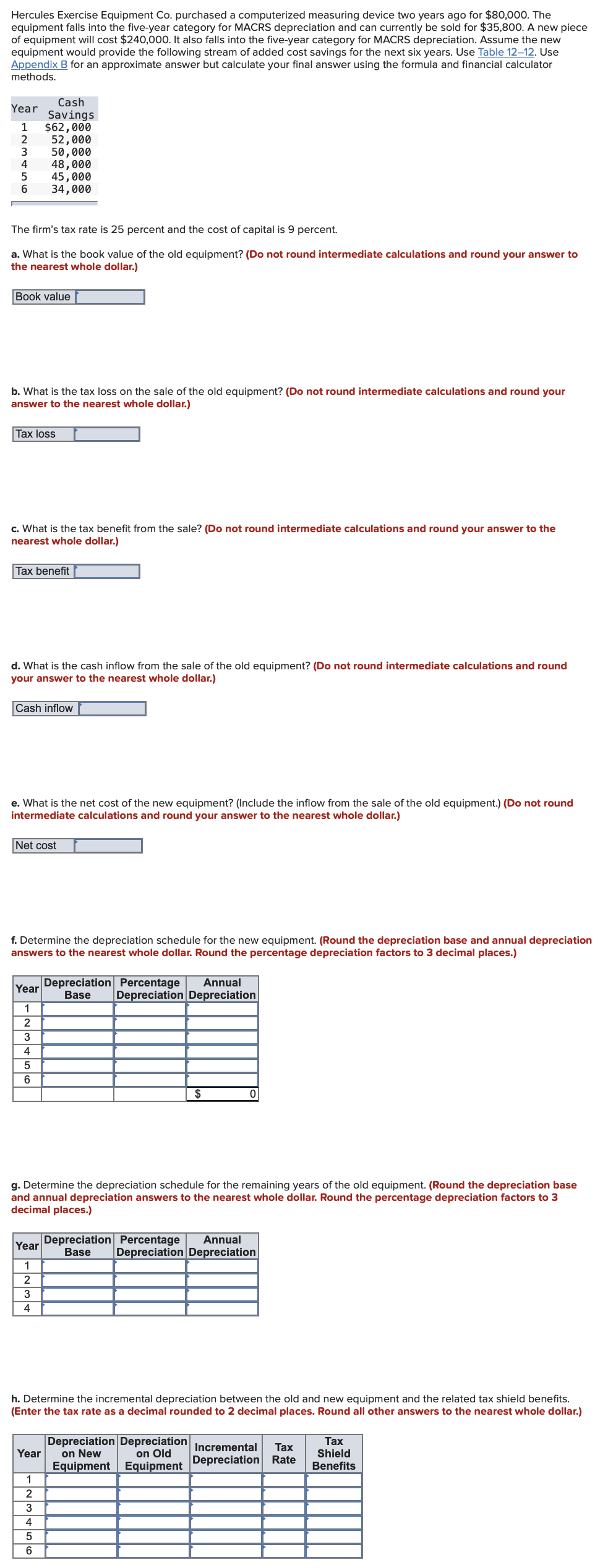

Question: Hercules Exercise Equipment Co. purchased a computerized measuring device two years ago for $80,000. The equipment falls into the five-year category for MACRS depreciation and

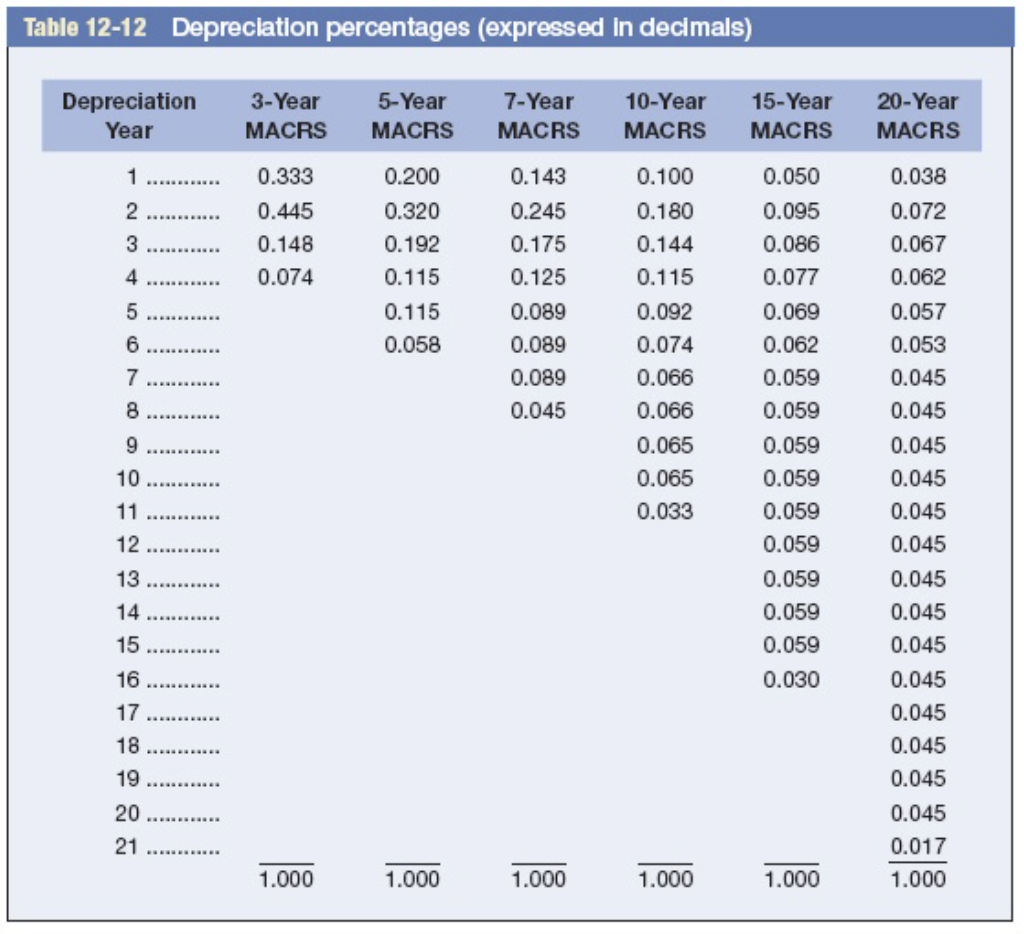

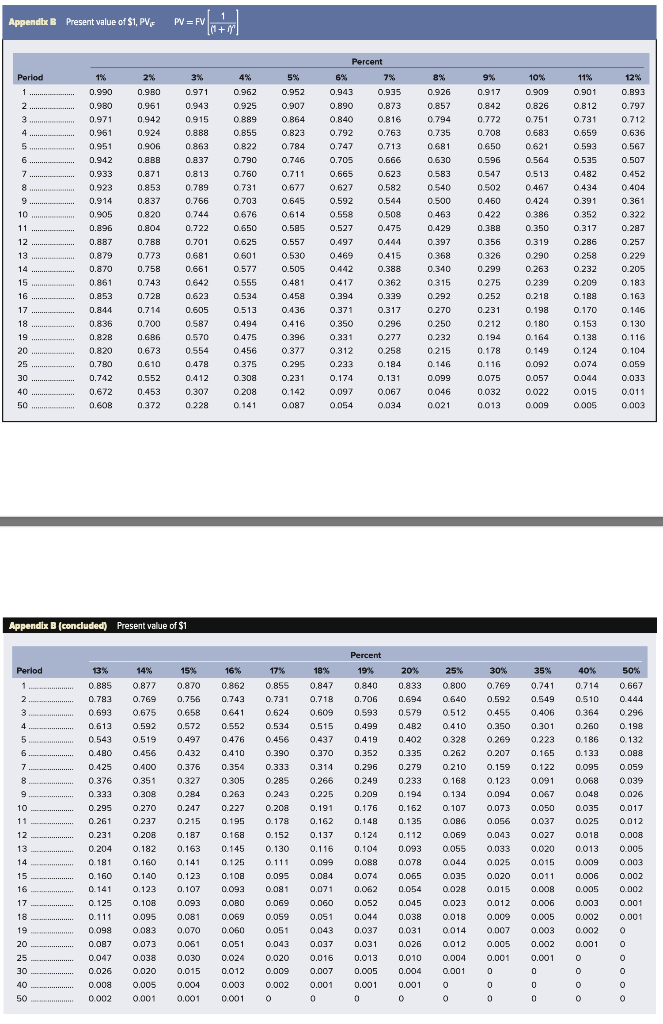

Hercules Exercise Equipment Co. purchased a computerized measuring device two years ago for $80,000. The equipment falls into the five-year category for MACRS depreciation and can currently be sold for $35,800. A new piece of equipment will cost $240,000. It also falls into the five-year category for MACRS depreciation. Assume the new equipment would provide the following stream of added cost savings for the next six years. Use Table 1212. Use Appendix B for an approximate answer but calculate your final answer using the formula and financial calculator methods. Cash Year Savings 1 $62,000 2 52,000 3 50,000 4 48,000 5 45,000 6 34,000 The firm's tax rate is 25 percent and the cost of capital is 9 percent. a. What is the book value of the old equipment? (Do not round intermediate calculations and round your answer to the nearest whole dollar.) Book value b. What is the tax loss on the sale of the old equipment? (Do not round intermediate calculations and round your answer to the nearest whole dollar.) Tax loss c. What is the tax benefit from the sale? (Do not round intermediate calculations and round your answer to the nearest whole dollar.) Tax benefit d. What is the cash inflow from the sale of the old equipment? (Do not round intermediate calculations and round your answer to the nearest whole dollar.) Cash inflow e. What is the net cost of the new equipment? (Include the inflow from the sale of the old equipment.) (Do not round intermediate calculations and round your answer to the nearest whole dollar.) Net cost f. Determine the depreciation schedule for the new equipment. (Round the depreciation base and annual depreciation answers to the nearest whole dollar. Round the percentage depreciation factors to 3 decimal places.) Annual Depreciation Percentage Year Base Depreciation Depreciation 1 2 3 4 5 6 $ g. Determine the depreciation schedule for the remaining years of the old equipment. (Round the depreciation base and annual depreciation answers to the nearest whole dollar. Round the percentage depreciation factors to 3 decimal places.) Annual Depreciation Percentage Year Base Depreciation Depreciation 1 | 2 3 4 h. Determine the incremental depreciation between the old and new equipment and the related tax shield benefits. (Enter the tax rate as a decimal rounded to 2 decimal places. Round all other answers to the nearest whole dollar.) Tax Year Depreciation Depreciation Incremental Depreciation Rate Equipment Equipment on New on Old Tax Shield Benefits 1 2 3 4 5 6 Table 12-12 Depreciation percentages (expressed in decimals) 3-Year 5-Year 7-Year 10-Year 20-Year Depreciation Year 15-Year MACRS MACRS MACRS MACRS MACRS MACRS 1 0.333 0.200 0.143 0.100 0.050 0.038 2 0.445 0.320 0.245 0.180 0.095 0.072 3 0.148 0.192 0.175 0.144 0.086 0.067 4 0.074 0.115 0.125 0.115 0.077 0.062 5 0.115 0.089 0.092 0.069 0.057 0.058 0.089 0.074 0.062 0.053 O CO 7 0.089 0.066 0.059 0.045 0.045 0.066 0.059 0.045 9 0.065 0.045 0.059 0.059 10 0.065 0.045 11 0.033 0.059 0.045 12 0.059 0.045 13 0.059 0.045 14 0.059 0.045 15 0.059 0.045 16 0.030 0.045 17 0.045 18 0.045 19 0.045 20 0.045 21 0.017 1.000 1.000 1.000 1.000 1.000 1.000 Appendbe B Present value of $1, PV PV = FV Percent Period 1% 2% 3% 4% 5% 7% 8% 9% 10% 11% 12% 1. 0.990 0.980 0.971 0.962 0.952 0.943 0.935 0.926 0.917 0.909 0.901 0.893 2 ......... 0.980 0.961 0.943 0.907 0.890 0.873 0.857 0.842 0.826 0.812 0.797 0.925 0.889 3 0.971 0.942 0.915 0.864 0.840 0.816 0.794 0.772 0.751 0.731 0.712 4 0.961 0.924 0.888 0.855 0.823 0.792 0.763 0.735 0.708 0.683 0.659 0.636 0567 5 0.951 0.906 0.863 0.822 0.784 0.747 0.713 0.681 0.650 0.621 0.593 6 0.942 0.8BB 0.837 0.790 0.746 0.705 0.666 0.630 0.596 0.564 0.535 0.507 7 0.933 0.871 0.813 0.760 0.711 0.665 0.623 0.583 0.547 0.513 0.482 0.452 0.404 8 0.923 0.853 0.789 0731 0.677 0.627 0.582 0.540 0.502 0.467 0.434 9 0.914 0.837 0.766 0.703 0.645 0.592 0.544 0.500 0.460 0.424 0.391 0.361 10 0.905 0.820 0.744 0.676 0.614 0.558 0.508 0.463 0.422 0.386 0.352 0.322 11 0.896 0.804 0.722 0.650 0.585 0.527 0.475 0.429 0.3BB 0.350 0.317 0.287 12 0.887 0.7BE 0.701 0.625 0.557 0.497 0.444 0.397 0.356 0.319 0.286 0.257 13 0.879 0.773 0.681 0.601 0.530 0.469 0.415 0.368 0.326 0290 0.258 0.229 14 0.870 0.758 0.661 0.577 0.505 0.442 0.388 0.340 0.299 0.263 0.232 0.205 15 ......... 0.861 0.743 0.642 0.555 0.481 0.417 0.362 0.315 0.275 0239 0.209 0.183 16 0.853 0.728 0.623 0.534 0.458 0.394 0.339 0.292 0.252 0.218 0.188 0.163 17 0.844 0.714 0.605 0.513 0.436 0.371 0.317 0.270 0.231 0.198 0.170 0.146 18 0.836 0.700 0.587 0.494 0.416 0.350 0.296 0.250 0.212 0.180 0.153 0.130 19 0.828 0.686 0.570 0.475 0.396 0.331 0.277 0.232 0.194 0.164 0.138 0.116 20 0.820 0.673 0.554 0.456 0.377 0.312 0.258 0.215 0.178 0.149 0.124 0.104 25 0.780 0.610 0.479 0.375 0.295 0.233 0.184 0.146 0.116 0.092 0.074 0.059 30 0.742 0.552 0.412 0.308 0.231 0.174 0.131 0.099 0.075 0.057 0.044 0.033 40 0.672 0.453 0.307 0.142 0.097 0.067 0.046 0.032 0.022 0.015 0.011 0.208 0.141 50 ... 0.608 0.372 0.228 0.087 0.054 0.034 0.021 0.013 0.009 0.005 0.003 Appendix B (concluded) Present value of $1 Percent Period 13% 14% 15% 16% 17% 18% 19% 20% % 25% 30% 35% 40% 50%. 1 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833 0.800 0.769 0.741 0.714 0.667 2. 0.783 0.769 0.756 0.743 0.731 0.718 0.706 0.694 0.640 0.592 0.549 0.510 0.444 3. 0.693 0.675 0.658 0.641 0624 0.609 0.593 0.579 0.512 0.455 0.406 0.364 0.296 4 ... 0.613 0.592 0.572 0.552 0.534 0.515 0.499 0.482 0.410 0.350 0.301 0.260 0.198 5 0.543 0.519 0.497 0.476 0.456 0.437 0.419 0.402 0.328 0.269 0.223 0.186 0.132 6 0.480 0.456 0.432 0.410 0.390 0.370 0.352 0.335 0.262 0.207 0.165 0.133 0.098 7 0.425 0.400 0.376 0.354 0.333 0.314 0.296 0.279 0.210 0.159 0.122 0.095 0.059 8 0.376 0.351 0.327 0.305 0.285 0.266 0.249 0.233 0.168 0.123 0.091 0.068 0.039 9. 0.333 0.308 0.284 0.263 0.243 0.225 0.209 0.194 0.134 0.094 0.067 0.048 0.026 10 0.295 0.270 0.247 0.227 0.208 0.191 0.176 0.162 0.107 0.073 0.050 0.035 0.017 11 0.261 0.237 0.215 0.195 0.178 0.162 0.148 0.135 0.086 0.056 0.037 0.025 0.012 12 0.231 0.208 0.187 0.168 0.152 0.137 0.124 0.112 0.069 0.043 0.027 0.018 0.008 13 0.204 0.182 0.163 0.145 0.116 0.104 0.093 0.055 0.033 0.020 0.013 0.005 0.130 0.111 14 0.181 0.160 0.141 0.125 0.099 0.088 0.078 0.044 0.025 0.015 0.009 0.003 15 0.160 0.140 0.123 0.108 0.095 0.084 0.074 0.065 0.035 0.020 0.011 0.006 0.002 16 0.141 0.123 0.107 0.093 0.081 0.071 0.062 0.054 0.028 0.015 0.008 0.005 0.002 17 0.125 0.108 0.09 0.OBO 0.069 0.060 0.052 0.045 0.023 0.012 0.006 0.003 0.001 18 0.111 0.095 0.081 0.069 0.059 0.051 0.044 0.038 0.018 0.009 0.005 0.002 0.001 19 0098 0.083 0.070 0.060 0.051 0,043 0.037 0.031 0.014 0.007 0.003 0.002 0 20 0.087 0.073 0.061 0.051 0.043 0.037 0.031 0.026 0.012 0.005 0.002 0.001 0 25 0.047 0.038 0.030 0.024 0.020 0.016 0.013 0.010 0.004 0.001 0.001 0 30 0.026 0.020 0.015 0.012 0.009 0.007 0.005 0.004 0.001 0 0 o 0 40 0.008 0.005 0.004 0.003 0.002 0.001 0.001 0.001 0 0 0 0 0 50 0002 0.001 0.001 0.001 0 0 0 0 0 0 0 0 0

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts