Question: here are the data in problem 1 Given the data in problem 1, what is the standard deviation of return from the point of view

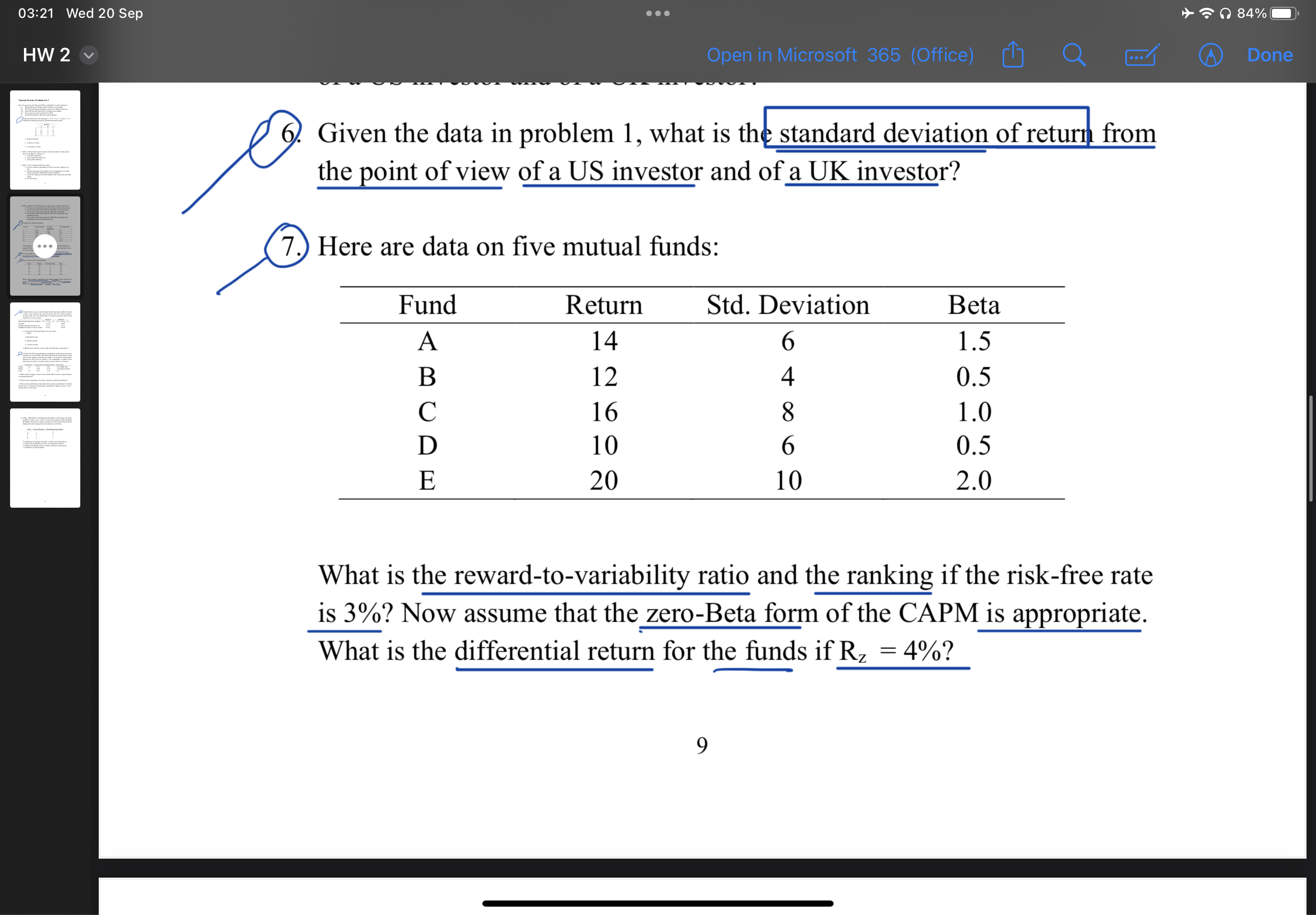

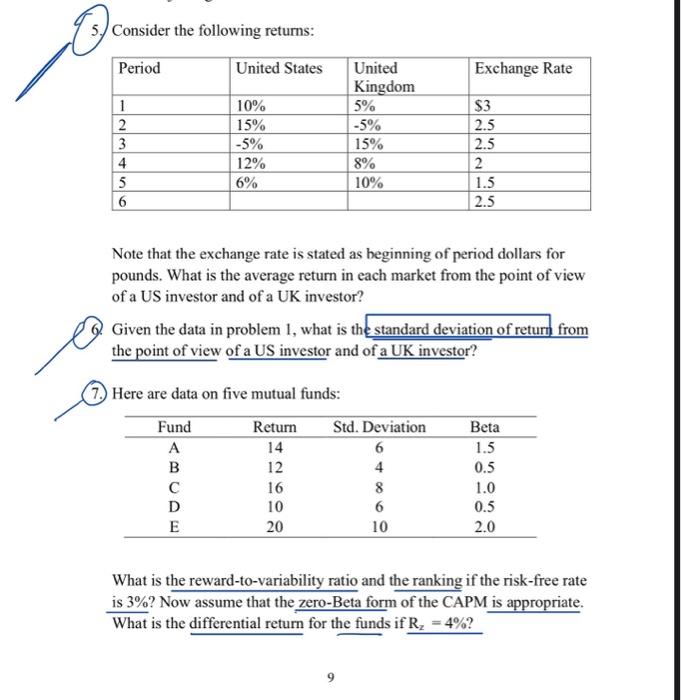

Given the data in problem 1, what is the standard deviation of return from the point of view of a US investor and of a UK investor? Here are data on five mutual funds: What is the reward-to-variability ratio and the ranking if the risk-free rate is 3% ? Now assume that the zero-Beta form of the CAPM is appropriate. What is the differential return for the funds if Rz=4% ? Consider the following returns: Note that the exchange rate is stated as beginning of period dollars for pounds. What is the average return in each market from the point of view of a US investor and of a UK investor? Given the data in problem 1, what is th from the point of view of a US investor and of a UK investor? Here are data on five mutual funds: What is the reward-to-variability ratio and the ranking if the risk-free rate is 3% ? Now assume that the zero-Beta form of the CAPM is appropriate. What is the differential return for the funds if Rz=4% ? Given the data in problem 1, what is the standard deviation of return from the point of view of a US investor and of a UK investor? Here are data on five mutual funds: What is the reward-to-variability ratio and the ranking if the risk-free rate is 3% ? Now assume that the zero-Beta form of the CAPM is appropriate. What is the differential return for the funds if Rz=4% ? Consider the following returns: Note that the exchange rate is stated as beginning of period dollars for pounds. What is the average return in each market from the point of view of a US investor and of a UK investor? Given the data in problem 1, what is th from the point of view of a US investor and of a UK investor? Here are data on five mutual funds: What is the reward-to-variability ratio and the ranking if the risk-free rate is 3% ? Now assume that the zero-Beta form of the CAPM is appropriate. What is the differential return for the funds if Rz=4%

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts