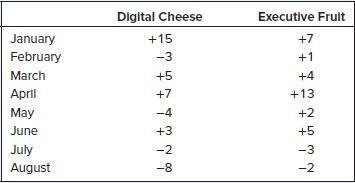

Question: Here are the returns on two stocks. a. Calculate the variance and standard deviation of each stock. Which stock is riskier if held on its

Here are the returns on two stocks.

a. Calculate the variance and standard deviation of each stock. Which stock is riskier if held on its own?

b. Now calculate the returns in each month of a portfolio that invests an equal amount each month in the two stocks.

c. Is the variance more or less than halfway between the variance of the two individual stocks?

Digital Cheese Executive Frult January +15 +7 February -3 +1 March +5 +4 April +7 +13 May -4 +2 June +3 +5 July -2 -3 August -8 -2

Step by Step Solution

3.52 Rating (169 Votes )

There are 3 Steps involved in it

Examiners utilize standard deviation as a boundary to quantify fluctuation conseque... View full answer

Get step-by-step solutions from verified subject matter experts