Question: Hi! Same problem, four parts. Required information Use the following information for Exercises 4-5 below. (Algo) [The following information applies to the questions displayed below]

![displayed below] Following are the issuances of stock transactions. 1. A corporation](https://dsd5zvtm8ll6.cloudfront.net/si.experts.images/questions/2024/09/66f7bb42e8f6a_36266f7bb42912a3.jpg)

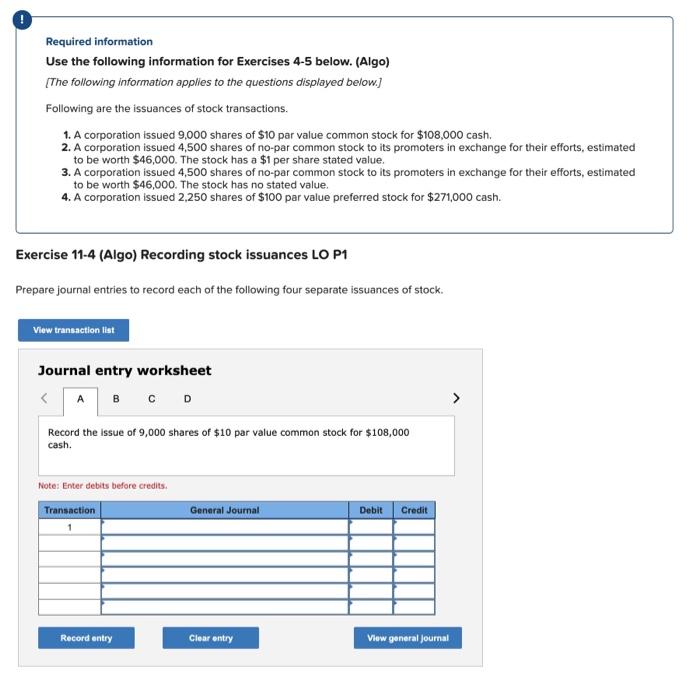

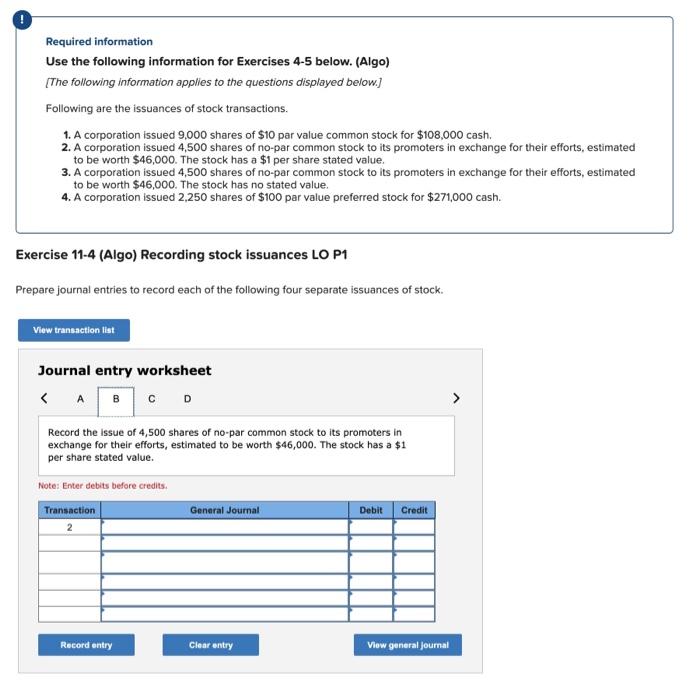

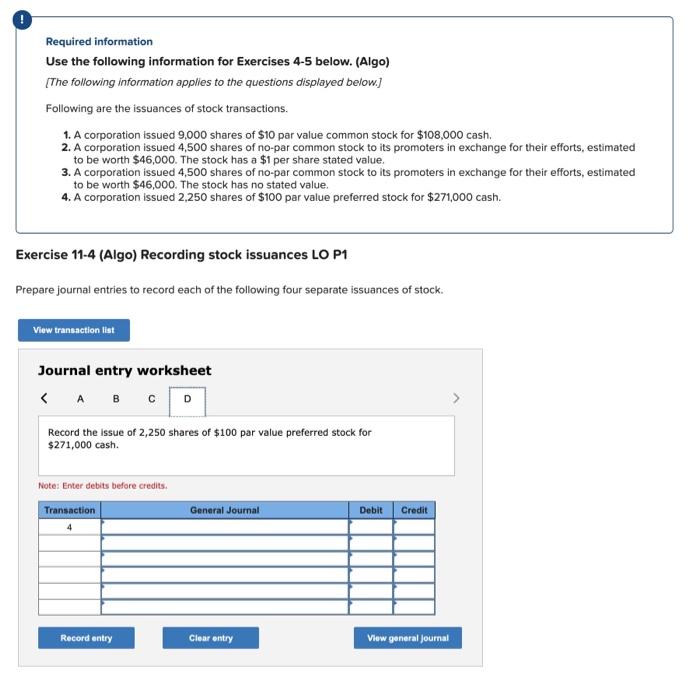

Required information Use the following information for Exercises 4-5 below. (Algo) [The following information applies to the questions displayed below] Following are the issuances of stock transactions. 1. A corporation issued 9,000 shares of $10 par value common stock for $108,000 cash. 2. A corporation issued 4,500 shares of no-par common stock to its promoters in exchange for their efforts, estimated to be worth $46,000. The stock has a $1 per share stated value. 3. A corporation issued 4,500 shares of no-par common stock to its promoters in exchange for their efforts, estimated to be worth $46,000. The stock has no stated value. 4. A corporation issued 2,250 shares of $100 par value preferred stock for $271,000 cash. Exercise 11-4 (Algo) Recording stock issuances LO P1 Prepare journal entries to record each of the following four separate issuances of stock. Journal entry worksheet Record the issue of 9,000 shares of $10 par value common stock for $108,000 cash. Note: Enter debits before credits. Required information Use the following information for Exercises 4-5 below. (Algo) [The following information applies to the questions displayed below] Following are the issuances of stock transactions. 1. A corporation issued 9,000 shares of $10 par value common stock for $108,000cash. 2. A corporation issued 4,500 shares of no-par common stock to its promoters in exchange for their efforts, estimated to be worth $46,000. The stock has a $1 per share stated value. 3. A corporation issued 4,500 shares of no-par common stock to its promoters in exchange for their efforts, estimated to be worth $46,000. The stock has no stated value. 4. A corporation issued 2,250 shares of $100 par value preferred stock for $271,000 cash. Exercise 11-4 (Algo) Recording stock issuances LO P1 Prepare journal entries to record each of the following four separate issuances of stock. Journal entry worksheet Record the issue of 4,500 shares of no-par common stock to its promoters in exchange for their efforts, estimated to be worth $46,000. The stock has a $1 per share stated value. Note: Enter debits before credits. Required information Use the following information for Exercises 4-5 below. (Algo) [The following information applies to the questions displayed below] Following are the issuances of stock transactions. 1. A corporation issued 9,000 shares of $10 par value common stock for $108,000cash. 2. A corporation issued 4,500 shares of no-par common stock to its promoters in exchange for their efforts, estimated to be worth $46,000. The stock has a $1 per share stated value. 3. A corporation issued 4,500 shares of no-par common stock to its promoters in exchange for their efforts, estimated to be worth $46,000. The stock has no stated value. 4. A corporation issued 2,250 shares of $100 par value preferred stock for $271,000 cash. Exercise 11-4 (Algo) Recording stock issuances LO P1 Prepare journal entries to record each of the following four separate issuances of stock. Journal entry worksheet Record the issue of 4,500 shares of no-par common stock to its promoters in exchange for their efforts, estimated to be worth $46,000. The stock has no stated value. Note: Enter debits before credits. Required information Use the following information for Exercises 4-5 below. (Algo) [The following information applies to the questions displayed below] Following are the issuances of stock transactions. 1. A corporation issued 9,000 shares of $10 par value common stock for $108,000cash. 2. A corporation issued 4,500 shares of no-par common stock to its promoters in exchange for their efforts, estimated to be worth $46,000. The stock has a $1 per share stated value. 3. A corporation issued 4,500 shares of no-par common stock to its promoters in exchange for their efforts, estimated to be worth $46,000. The stock has no stated value. 4. A corporation issued 2,250 shares of $100 par value preferred stock for $271,000 cash. Exercise 11-4 (Algo) Recording stock issuances LO P1 Prepare journal entries to record each of the following four separate issuances of stock. Journal entry worksheet Record the issue of 2,250 shares of $100 par value preferred stock for $271,000 cash. Note: Enter debits before credits

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts