Question: how do you get these numbers? show work! how did they get the numbers in the boxes specifically. Homework 3 A stock price is currently

how do you get these numbers? show work! how did they get the numbers in the boxes specifically.

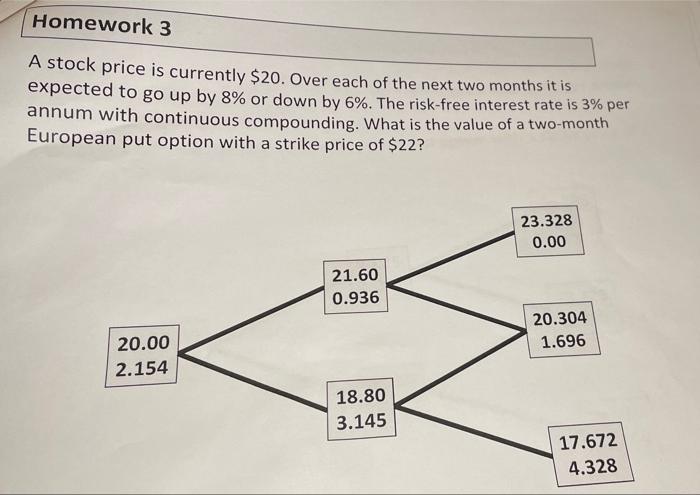

Homework 3 A stock price is currently $20. Over each of the next two months it is expected to go up by 8% or down by 6%. The risk-free interest rate is 3% per annum with continuous compounding. What is the value of a two-month European put option with a strike price of $22? a 23.328 0.00 21.60 0.936 20.304 1.696 20.00 2.154 18.80 3.145 17.672 4.328

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock