Question: How Does Overdraft Protection Work, and Why Is It Valuable? An overdraft occurs when an account holder attempts to withdraw funds or to make a

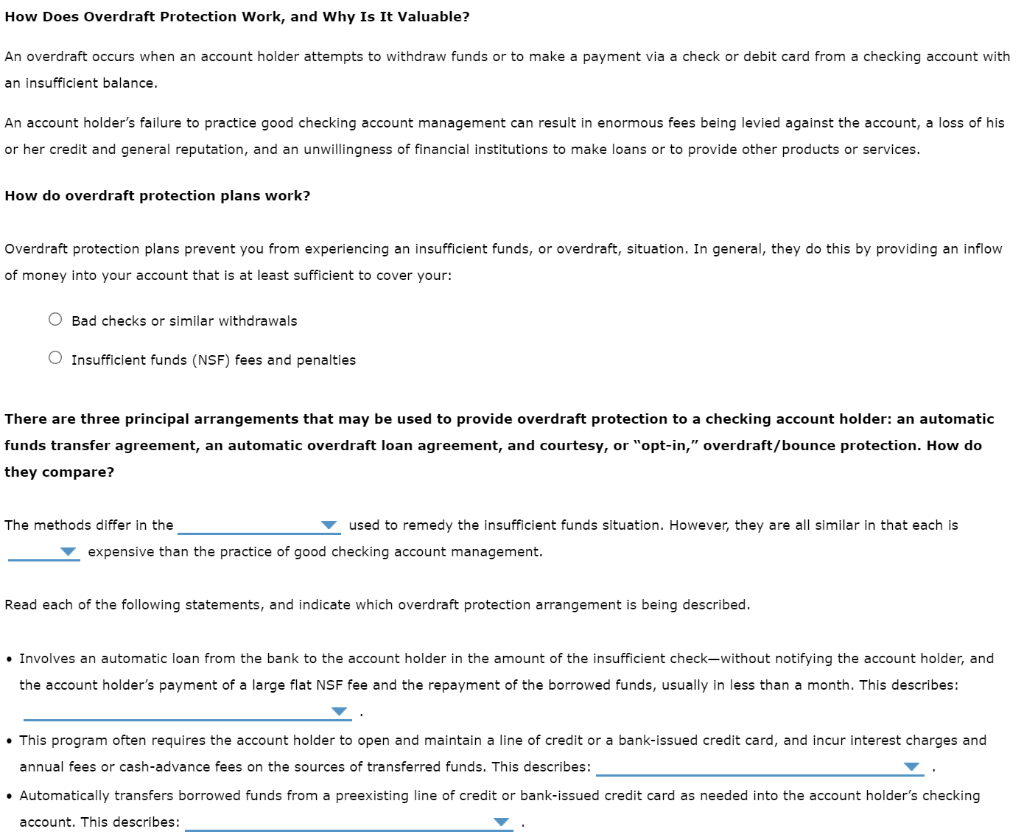

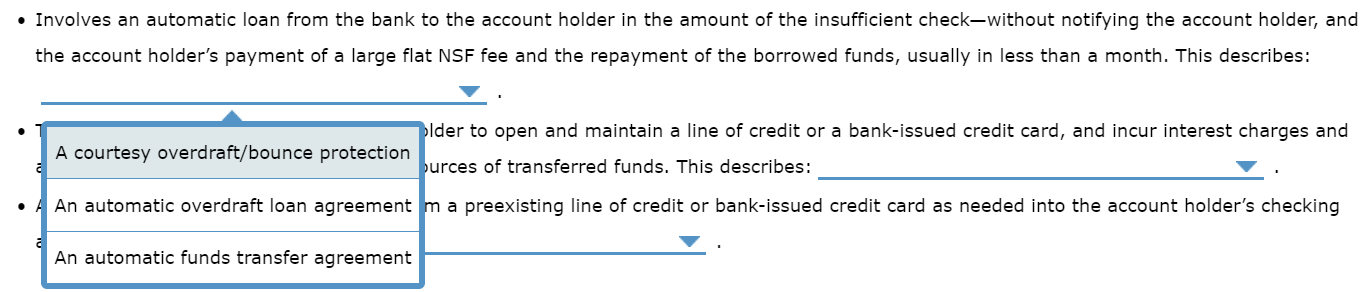

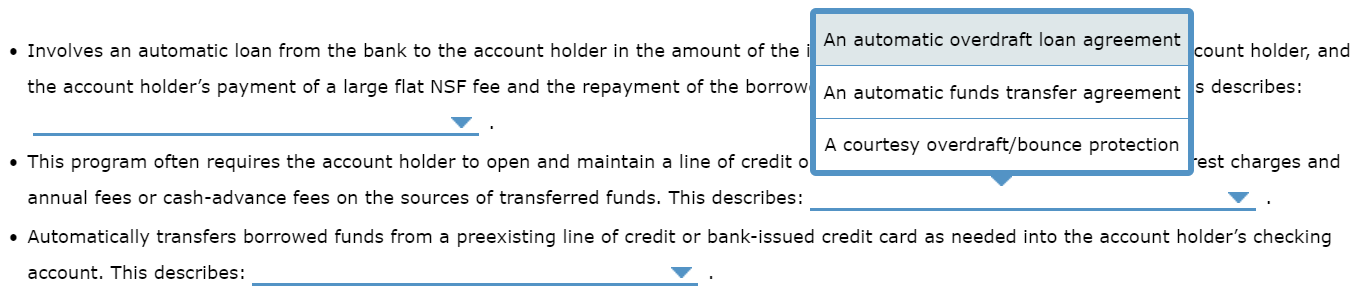

How Does Overdraft Protection Work, and Why Is It Valuable? An overdraft occurs when an account holder attempts to withdraw funds or to make a payment via a check or debit card from a checking account with an insufficient balance. An account holder's failure to practice good checking account management can result in enormous fees being levied against the account, a loss of his or her credit and general reputation, and an unwillingness of financial institutions to make loans or to provide other products or services. How do overdraft protection plans work? Overdraft protection plans prevent you from experiencing an insufficient funds, or overdraft, situation. In general, they do this by providing an inflow of money into your account that is at least sufficient to cover your: O Bad checks or similar withdrawals O Insufficient funds (NSF) fees and penalties There are three principal arrangements that may be used to provide overdraft protection to a checking account holder: an automatic funds transfer agreement, an automatic overdraft loan agreement, and courtesy, or "opt-in," overdraft/bounce protection. How do they compare? The methods differ in the used to remedy the insufficient funds situation. However, they are all similar in that each is expensive than the practice of good checking account management. Read each of the following statements, and indicate which overdraft protection arrangement is being described. Involves an automatic loan from the bank to the account holder in the amount of the insufficient check-without notifying the account holder, and the account holder's payment of a large flat NSF fee and the repayment of the borrowed funds, usually in less than a month. This describes: . This program often requires the account holder to open and maintain a line of credit or a bank-issued credit card, and incur interest charges and annual fees or cash-advance fees on the sources of transferred funds. This describes: Automatically transfers borrowed funds from a preexisting line of credit or bank-issued credit card as needed into the account holder's checking account. This describes: The methods differ in the used to remedy the insufficient funds situation. However, they are all similar in that each is expensive tha d checking account management. sources and costs Read each of the following uses and costs Jicate which overdraft protection arrangement is being described. The methods differ in the used to remedy the insufficient funds situation. However, they are all similar in that each is expensive than the practice of good checking account management. less th of the following statements, and indicate which overdraft protection arrangement is being described. more Tuvoives an automatic loan from the bank to the account holder in the amount of the insufficient check-without notifying the account holder, and Involves an automatic loan from the bank to the account holder in the amount of the insufficient check-without notifying the account holder, and the account holder's payment of a large flat NSF fee and the repayment of the borrowed funds, usually in less than a month. This describes: plder to open and maintain a line of credit or a bank-issued credit card, and incur interest charges and A courtesy overdraft/bounce protection burces of transferred funds. This describes: . An automatic overdraft loan agreement ma preexisting line of credit or bank-issued credit card as needed into the account holder's checking An automatic funds transfer agreement Involves an automatic loan from the bank to the account holder in the amount of the An automatic overdraft loan agreement count holder, and the account holder's payment of a large flat NSF fee and the repayment of the borrow An automatic funds transfer agreement s describes: A courtesy overdraft/bounce protection Jest charges and This program often requires the account holder to open and maintain a line of credito annual fees or cash-advance fees on the sources of transferred funds. This describes: Automatically transfers borrowed funds from a preexisting line of credit or bank-issued credit card as needed into the account holder's checking account. This describes: Involves an automatic loan from the bank to the account holder in the amount of the insufficient check-without notifying the account holder, and the account holder's pay ment of the borrowed funds, usually in less than a month. This describes: An automatic funds transfer agreement This program often requi An automatic overdraft loan agreement in a line of credit or a bank-issued credit card, and incur interest charges and annual fees or cash-adva ds. This describes: A courtesy overdraft/bounce protection Automatically transfers b redit or bank-issued credit card as needed into the account holder's checking account. This describes: How Does Overdraft Protection Work, and Why Is It Valuable? An overdraft occurs when an account holder attempts to withdraw funds or to make a payment via a check or debit card from a checking account with an insufficient balance. An account holder's failure to practice good checking account management can result in enormous fees being levied against the account, a loss of his or her credit and general reputation, and an unwillingness of financial institutions to make loans or to provide other products or services. How do overdraft protection plans work? Overdraft protection plans prevent you from experiencing an insufficient funds, or overdraft, situation. In general, they do this by providing an inflow of money into your account that is at least sufficient to cover your: O Bad checks or similar withdrawals O Insufficient funds (NSF) fees and penalties There are three principal arrangements that may be used to provide overdraft protection to a checking account holder: an automatic funds transfer agreement, an automatic overdraft loan agreement, and courtesy, or "opt-in," overdraft/bounce protection. How do they compare? The methods differ in the used to remedy the insufficient funds situation. However, they are all similar in that each is expensive than the practice of good checking account management. Read each of the following statements, and indicate which overdraft protection arrangement is being described. Involves an automatic loan from the bank to the account holder in the amount of the insufficient check-without notifying the account holder, and the account holder's payment of a large flat NSF fee and the repayment of the borrowed funds, usually in less than a month. This describes: . This program often requires the account holder to open and maintain a line of credit or a bank-issued credit card, and incur interest charges and annual fees or cash-advance fees on the sources of transferred funds. This describes: Automatically transfers borrowed funds from a preexisting line of credit or bank-issued credit card as needed into the account holder's checking account. This describes: The methods differ in the used to remedy the insufficient funds situation. However, they are all similar in that each is expensive tha d checking account management. sources and costs Read each of the following uses and costs Jicate which overdraft protection arrangement is being described. The methods differ in the used to remedy the insufficient funds situation. However, they are all similar in that each is expensive than the practice of good checking account management. less th of the following statements, and indicate which overdraft protection arrangement is being described. more Tuvoives an automatic loan from the bank to the account holder in the amount of the insufficient check-without notifying the account holder, and Involves an automatic loan from the bank to the account holder in the amount of the insufficient check-without notifying the account holder, and the account holder's payment of a large flat NSF fee and the repayment of the borrowed funds, usually in less than a month. This describes: plder to open and maintain a line of credit or a bank-issued credit card, and incur interest charges and A courtesy overdraft/bounce protection burces of transferred funds. This describes: . An automatic overdraft loan agreement ma preexisting line of credit or bank-issued credit card as needed into the account holder's checking An automatic funds transfer agreement Involves an automatic loan from the bank to the account holder in the amount of the An automatic overdraft loan agreement count holder, and the account holder's payment of a large flat NSF fee and the repayment of the borrow An automatic funds transfer agreement s describes: A courtesy overdraft/bounce protection Jest charges and This program often requires the account holder to open and maintain a line of credito annual fees or cash-advance fees on the sources of transferred funds. This describes: Automatically transfers borrowed funds from a preexisting line of credit or bank-issued credit card as needed into the account holder's checking account. This describes: Involves an automatic loan from the bank to the account holder in the amount of the insufficient check-without notifying the account holder, and the account holder's pay ment of the borrowed funds, usually in less than a month. This describes: An automatic funds transfer agreement This program often requi An automatic overdraft loan agreement in a line of credit or a bank-issued credit card, and incur interest charges and annual fees or cash-adva ds. This describes: A courtesy overdraft/bounce protection Automatically transfers b redit or bank-issued credit card as needed into the account holder's checking account. This describes

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts