Question: How to construct the unit factor portfolio for factor 1 with portfolio X, Y, and the risk-free asset: Well- diversified Portfolio Factor Sensitivity Factor Sensitivity

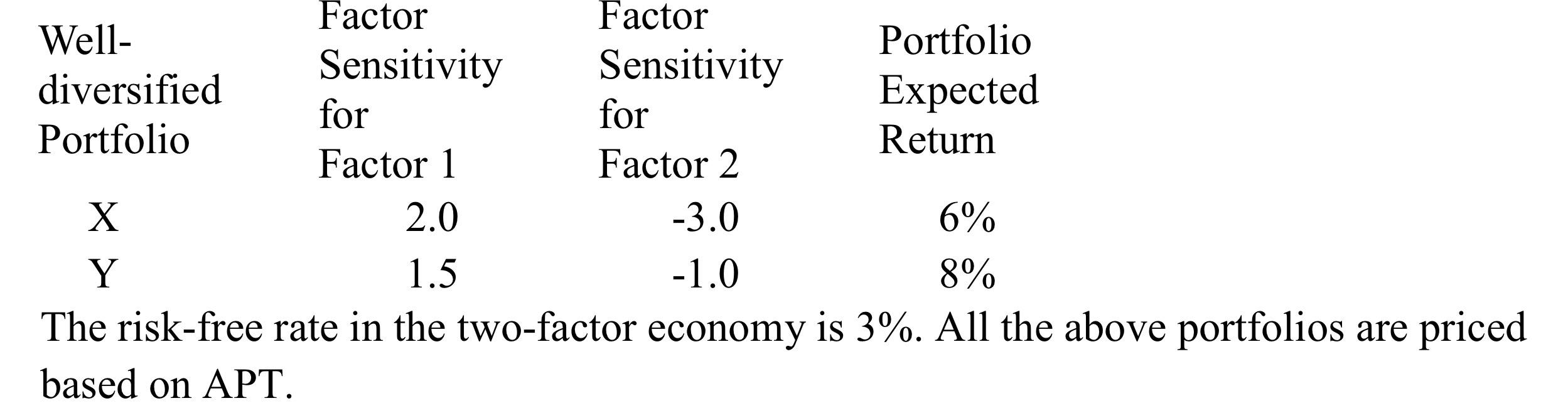

Well- diversified Portfolio Factor Sensitivity Factor Sensitivity Portfolio Expected Return for for Factor 1 Factor 2 X 2.0 -3.0 6% Y 1.5 -1.0 8% The risk-free rate in the two-factor economy is 3%. All the above portfolios are priced based on APT.

Step by Step Solution

★★★★★

3.50 Rating (170 Votes )

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

The expected return of portfolio factor 1 is 6 while its sensitivity to factor 1 is 15 This means th... View full answer

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock