Question: How would I go about solving this problem? It is very confusing and I am really struggling with Binomial Trees. Assume the stock price is

How would I go about solving this problem? It is very confusing and I am really struggling with Binomial Trees.

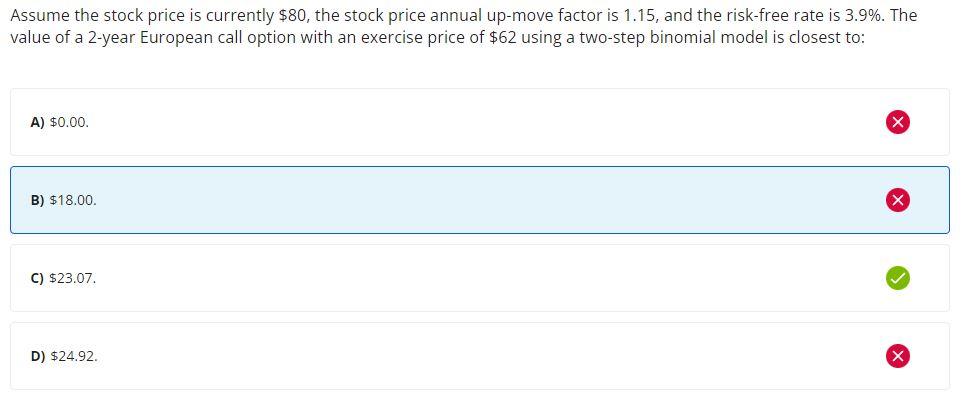

Assume the stock price is currently $80, the stock price annual up-move factor is 1.15, and the risk-free rate is 3.9%. The value of a 2-year European call option with an exercise price of $62 using a two-step binomial model is closest to: A) $0.00. B) $18.00. C) $23.07. D) $24.92

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock