Question: I do not know how to do qn 3 (e), could you show me the workings and formulas you used? I have attached the answers

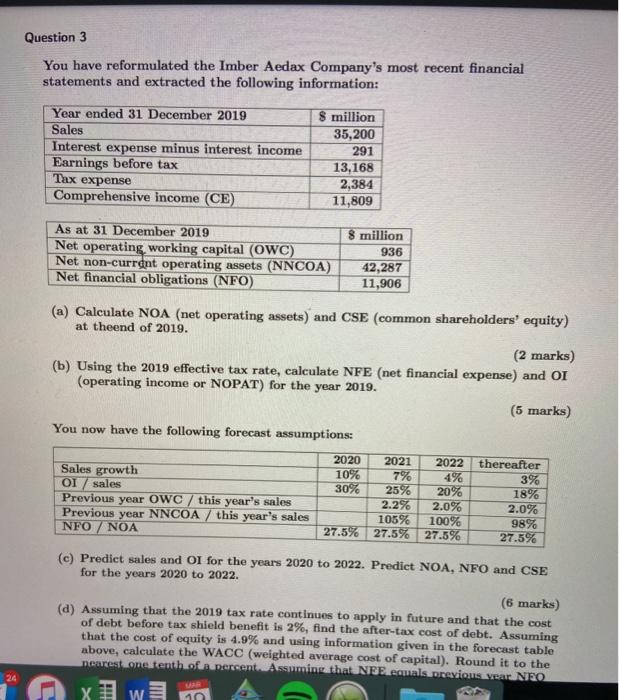

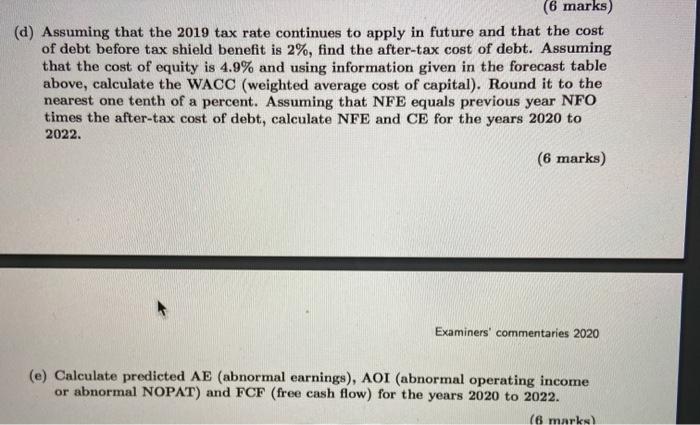

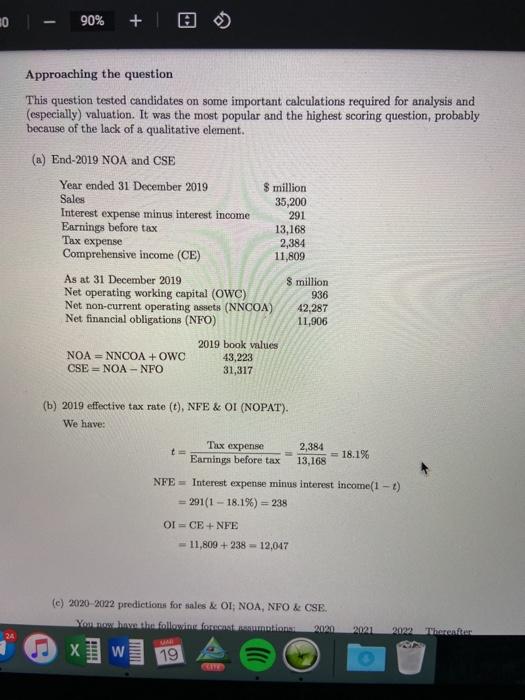

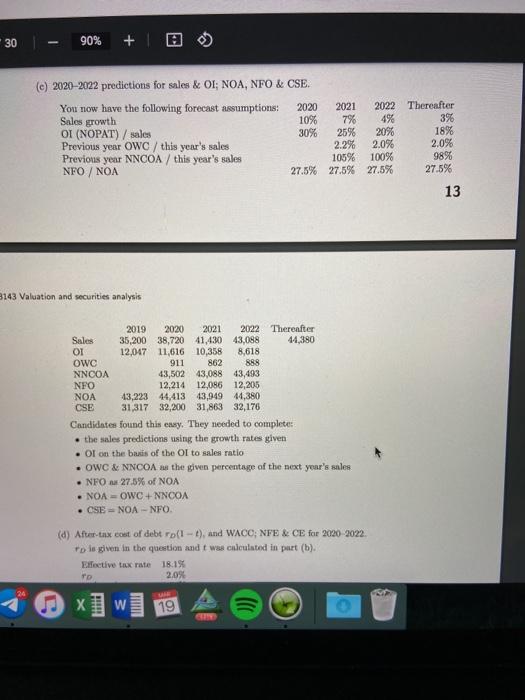

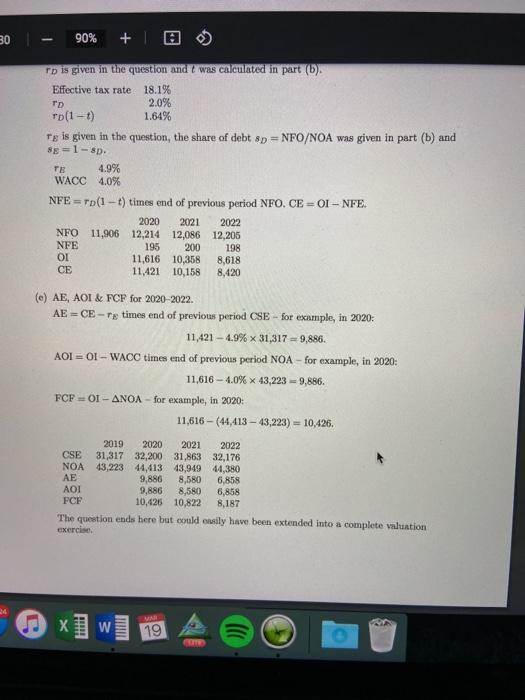

Question 3 You have reformulated the Imber Aedax Company's most recent financial statements and extracted the following information: Year ended 31 December 2019 Sales Interest expense minus interest income Earnings before tax Tax expense Comprehensive income (CE) 8 million 35,200 291 13,168 2,384 11,809 As at 31 Decemb 2019 Net operating working capital (OWC) Net non-current operating assets (NNCOA) Net financial obligations (NFO) 8 million 936 42,287 11,906 (a) Calculate NOA (net operating assets) and CSE (common shareholders' equity) at theend of 2019. (2 marks) (b) Using the 2019 effective tax rate, calculate NFE (net financial expense) and OI (operating income or NOPAT) for the year 2019. (5 marks) You now have the following forecast assumptions: 2022 Sales growth OI/ sales Previous year OWC / this year's sales Previous year NNCOA / this year's sales NFO/NOA 2020 2021 10% 7% 30% 25% 2.2% 105% 27.5% 27.5% 20% 2.0% 100% 27.5% thereafter 3% 18% 2.0% 98% 27.5% (c) Predict sales and Ol for the years 2020 to 2022. Predict NOA, NFO and CSE for the years 2020 to 2022. (6 marks) (a) Assuming that the 2019 tax rate continues to apply in future and that the cost of debt before tax shield benefit is 2%, find the after-tax cost of debt. Assuming that the cost of equity is 4.9% and using information given in the forecast table above, calculate the WACC (weighted average cost of capital). Round it to the nongest one tenth of a percent. Assuming that NEE. cemals previous year NEO 24 W 10 (6 marks) (d) Assuming that the 2019 tax rate continues to apply in future and that the cost of debt before tax shield benefit is 2%, find the after-tax cost of debt. Assuming that the cost of equity is 4.9% and using information given in the forecast table above, calculate the WACC (weighted average cost of capital). Round it to the nearest one tenth of a percent. Assuming that NFE equals previous year NFO times the after-tax cost of debt, calculate NFE and CE for the years 2020 to 2022. (6 marks) Examiners' commentaries 2020 (e) Calculate predicted AE (abnormal earnings), AOI (abnormal operating income or abnormal NOPAT) and FCF (free cash flow) for the years 2020 to 2022. (6 marks) 30 90% + Approaching the question This question tested candidates on some important calculations required for analysis and (especially) valuation. It was the most popular and the highest scoring question, probably because of the lack of a qualitative element. (a) End-2019 NOA and CSE Year ended 31 December 2019 S million Sales 35,200 Interest expense minus interest income 291 Earnings before tax 13,168 Tax expense 2,384 Comprehensive income (CE) 11,809 As at 31 December 2019 8 million Net operating working capital (OWC) 936 Net non-current operating assets (NNCOA) 42,287 Net financial obligations (NFO) 11,906 2019 book values NOA NNCOA + OWO 43,223 CSENOA - NFO 31,317 (b) 2019 effective tax rate (t), NFE & OI (NOPAT). We have: Tix expense 2,384 13,168 Earnings before tax 18.1% NFE Interest expense minus interest income(1-2) = 291(1 - 18.1%) = 238 OICE+NFE 11,809 +238 12,047 (c) 2020-2022 predictions for sales & OT: NOA, NFO & CSE. Sawah the followinformations 2020 20221 2022 Theronder x W 19 30 90% + (c) 2020-2022 predictions for sales & OL; NOA, NFO & CSE. You now have the following forecast assumptions: 2020 2021 2022 Thereafter Sales growth 10% 7% 4% 396 OI (NOPAT) / sales 30% 25% 20% 18% Previous year OWC / this year's sales 2.2% 2.0% 2.0% Previous year NNCOA / this year's sales 105% 100% 98% NFO / NOA 27.5% 27.5% 27.5% 27.5% 13 3143 Valuation and securities analysis 2019 2020 2021 2022 Thereafter Sales 35,200 38,72041,430 43,098 44,380 OI 12,047 11,616 10,358 8,618 OWC 911 862 888 NNCOA 43,502 43,088 43,493 NFO 12,214 12,086 12,205 NOA 13,223 44,413 43,949 44,380 CSE 31,317 32,200 31,863 32,176 Candidates found this easy. They needed to complete: the sales predictions using the growth rates given Ol on the basis of the Ol to sales ratio OWC & NNCOA as the given percentage of the next year's sales NFO - 27.5% of NOA NOA-OWC+NNCOA . CSE - NOA - NFO (d) After-tax cost of debt roll-t), and WACC; NFE & CE for 2020-2022 to is given in the question and was calculated in part (b). Effective tax rate 18.1% 2.0% TO W MI 19 30 90% + 0 rp is given in the question and I was calculated in part (6). Effective tax rate 18.1% TD 2.0% To(1-1) 1.64% Tg is given in the question, the share of debt 8D- =NFO/NOA was given in part (b) and SE=1-8p. TE 4.9% WACC 4.0% NFE = To(1 - 1) times end of previous period NFO. CEOI - NFE. 2020 2021 2022 NFO 11,906 12,214 12,086 12,205 NFE 195 200 198 OI 11,616 10,358 8,618 CE 11,421 10,158 8,420 (e) AE, AOI & FCF for 2020-2022. AE = CE - Te times end of previous period CSE - for example, in 2020: 11,421 - 4.9% x 31,3179,886. AOIOI - WACO times end of previous period NOA-for example, in 2020: 11,616 - 4.0% x 43,223 =9,886. FCFOI - ANOA-for example, in 2020: 11,616 - (44,413-43,223) = 10,426. 2019 2020 2021 2022 CSE 31,317 32,200 31,863 32,176 NOA 43,223 44,413 43,949 44,380 AE 9,886 8,580 6,858 9,886 8,580 FCF 10,426 10,822 8,187 The question ends here but could easily have been extended into a complete valuation exercise 6,858 xw 19 Question 3 You have reformulated the Imber Aedax Company's most recent financial statements and extracted the following information: Year ended 31 December 2019 Sales Interest expense minus interest income Earnings before tax Tax expense Comprehensive income (CE) 8 million 35,200 291 13,168 2,384 11,809 As at 31 Decemb 2019 Net operating working capital (OWC) Net non-current operating assets (NNCOA) Net financial obligations (NFO) 8 million 936 42,287 11,906 (a) Calculate NOA (net operating assets) and CSE (common shareholders' equity) at theend of 2019. (2 marks) (b) Using the 2019 effective tax rate, calculate NFE (net financial expense) and OI (operating income or NOPAT) for the year 2019. (5 marks) You now have the following forecast assumptions: 2022 Sales growth OI/ sales Previous year OWC / this year's sales Previous year NNCOA / this year's sales NFO/NOA 2020 2021 10% 7% 30% 25% 2.2% 105% 27.5% 27.5% 20% 2.0% 100% 27.5% thereafter 3% 18% 2.0% 98% 27.5% (c) Predict sales and Ol for the years 2020 to 2022. Predict NOA, NFO and CSE for the years 2020 to 2022. (6 marks) (a) Assuming that the 2019 tax rate continues to apply in future and that the cost of debt before tax shield benefit is 2%, find the after-tax cost of debt. Assuming that the cost of equity is 4.9% and using information given in the forecast table above, calculate the WACC (weighted average cost of capital). Round it to the nongest one tenth of a percent. Assuming that NEE. cemals previous year NEO 24 W 10 (6 marks) (d) Assuming that the 2019 tax rate continues to apply in future and that the cost of debt before tax shield benefit is 2%, find the after-tax cost of debt. Assuming that the cost of equity is 4.9% and using information given in the forecast table above, calculate the WACC (weighted average cost of capital). Round it to the nearest one tenth of a percent. Assuming that NFE equals previous year NFO times the after-tax cost of debt, calculate NFE and CE for the years 2020 to 2022. (6 marks) Examiners' commentaries 2020 (e) Calculate predicted AE (abnormal earnings), AOI (abnormal operating income or abnormal NOPAT) and FCF (free cash flow) for the years 2020 to 2022. (6 marks) 30 90% + Approaching the question This question tested candidates on some important calculations required for analysis and (especially) valuation. It was the most popular and the highest scoring question, probably because of the lack of a qualitative element. (a) End-2019 NOA and CSE Year ended 31 December 2019 S million Sales 35,200 Interest expense minus interest income 291 Earnings before tax 13,168 Tax expense 2,384 Comprehensive income (CE) 11,809 As at 31 December 2019 8 million Net operating working capital (OWC) 936 Net non-current operating assets (NNCOA) 42,287 Net financial obligations (NFO) 11,906 2019 book values NOA NNCOA + OWO 43,223 CSENOA - NFO 31,317 (b) 2019 effective tax rate (t), NFE & OI (NOPAT). We have: Tix expense 2,384 13,168 Earnings before tax 18.1% NFE Interest expense minus interest income(1-2) = 291(1 - 18.1%) = 238 OICE+NFE 11,809 +238 12,047 (c) 2020-2022 predictions for sales & OT: NOA, NFO & CSE. Sawah the followinformations 2020 20221 2022 Theronder x W 19 30 90% + (c) 2020-2022 predictions for sales & OL; NOA, NFO & CSE. You now have the following forecast assumptions: 2020 2021 2022 Thereafter Sales growth 10% 7% 4% 396 OI (NOPAT) / sales 30% 25% 20% 18% Previous year OWC / this year's sales 2.2% 2.0% 2.0% Previous year NNCOA / this year's sales 105% 100% 98% NFO / NOA 27.5% 27.5% 27.5% 27.5% 13 3143 Valuation and securities analysis 2019 2020 2021 2022 Thereafter Sales 35,200 38,72041,430 43,098 44,380 OI 12,047 11,616 10,358 8,618 OWC 911 862 888 NNCOA 43,502 43,088 43,493 NFO 12,214 12,086 12,205 NOA 13,223 44,413 43,949 44,380 CSE 31,317 32,200 31,863 32,176 Candidates found this easy. They needed to complete: the sales predictions using the growth rates given Ol on the basis of the Ol to sales ratio OWC & NNCOA as the given percentage of the next year's sales NFO - 27.5% of NOA NOA-OWC+NNCOA . CSE - NOA - NFO (d) After-tax cost of debt roll-t), and WACC; NFE & CE for 2020-2022 to is given in the question and was calculated in part (b). Effective tax rate 18.1% 2.0% TO W MI 19 30 90% + 0 rp is given in the question and I was calculated in part (6). Effective tax rate 18.1% TD 2.0% To(1-1) 1.64% Tg is given in the question, the share of debt 8D- =NFO/NOA was given in part (b) and SE=1-8p. TE 4.9% WACC 4.0% NFE = To(1 - 1) times end of previous period NFO. CEOI - NFE. 2020 2021 2022 NFO 11,906 12,214 12,086 12,205 NFE 195 200 198 OI 11,616 10,358 8,618 CE 11,421 10,158 8,420 (e) AE, AOI & FCF for 2020-2022. AE = CE - Te times end of previous period CSE - for example, in 2020: 11,421 - 4.9% x 31,3179,886. AOIOI - WACO times end of previous period NOA-for example, in 2020: 11,616 - 4.0% x 43,223 =9,886. FCFOI - ANOA-for example, in 2020: 11,616 - (44,413-43,223) = 10,426. 2019 2020 2021 2022 CSE 31,317 32,200 31,863 32,176 NOA 43,223 44,413 43,949 44,380 AE 9,886 8,580 6,858 9,886 8,580 FCF 10,426 10,822 8,187 The question ends here but could easily have been extended into a complete valuation exercise 6,858 xw 19

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts