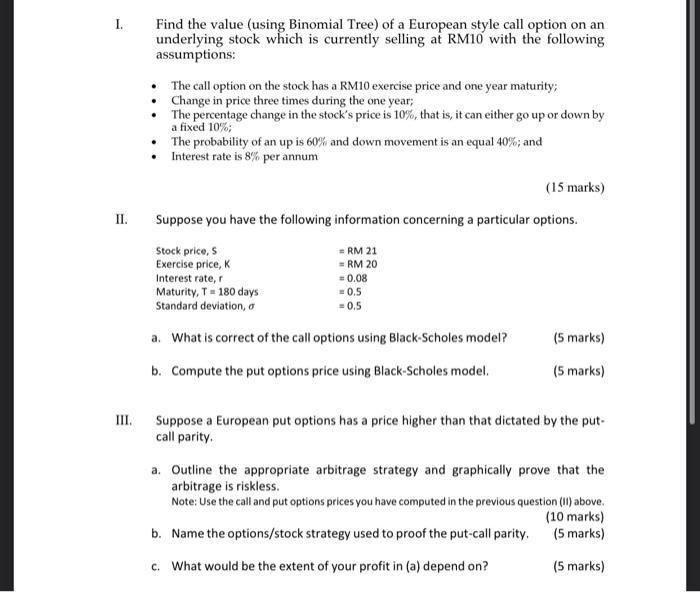

I. II. III. Find the value (using Binomial Tree) of a European style call option on...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Here are the answers to the questions I Find the value of a European call option using binomial tree method Stock price now RM10 Exercise price RM10 M... View the full answer

Related Book For

Intermediate Accounting principles and analysis

ISBN: 978-0471737933

2nd Edition

Authors: Terry d. Warfield, jerry j. weygandt, Donald e. kieso

Posted Date: