Question: I have to write R code for the following question and I don't know where to start. Any help/advice will be greatly appreciated. Question 1:

I have to write R code for the following question and I don't know where to start. Any help/advice will be greatly appreciated.

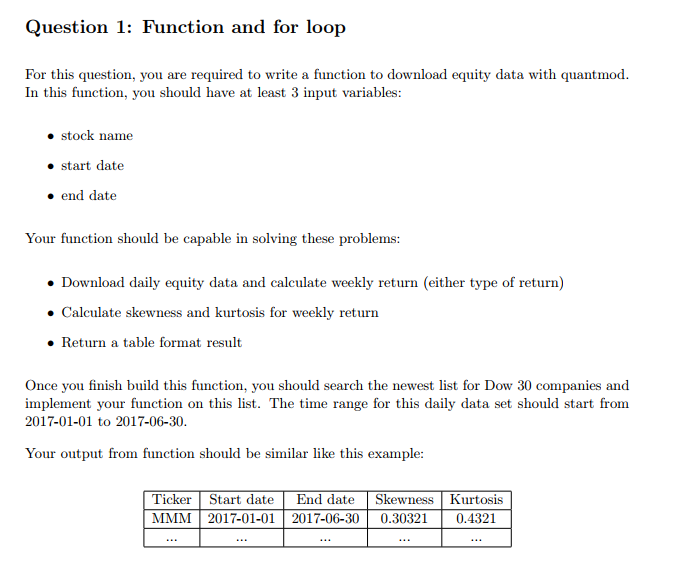

Question 1: Function and for loop For this question, you are required to write a function to download equity data with quantmod In this function, you should have at least 3 input variables: stock name . start date end date Your function should be capable in solving these problems: Download daily equity data and calculate weekly return (either type of return) . Calculate skewness and kurtosis for weekly return Return a table format result Once you finish build this function, you should search the newest list for Dow 30 companies and implement your function on this list. The time range for this daily data set should start from 2017-01-01 to 2017-06-30. Your output from function should be silar ike this example: Ticker Start date End date Skewness Kurtosis MMM 2017-01-01 2017-06-300.30321 0.4321

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts