Question: I just need help on part b. Let s and t be two nonnegative constants. Consider a stock whose present price is S(0) = 20

I just need help on part b.

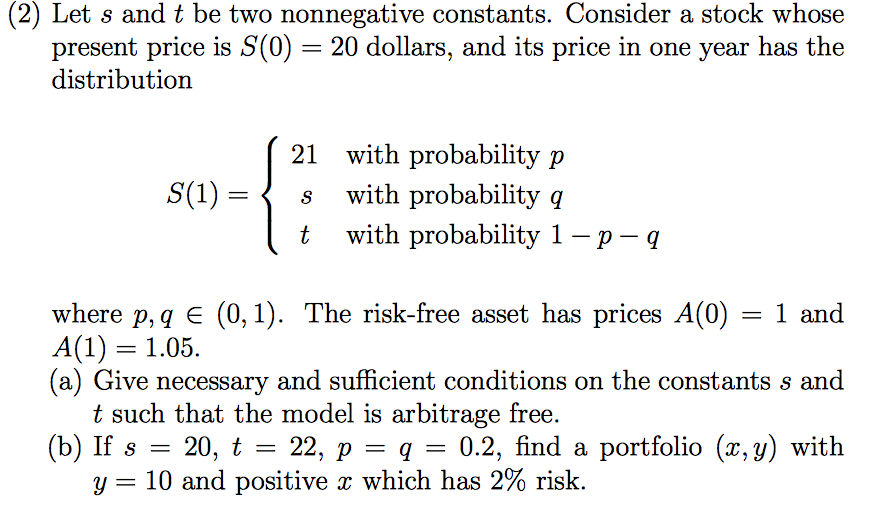

Let s and t be two nonnegative constants. Consider a stock whose present price is S(0) = 20 dollars, and its price in one year has the distribution S(1) = {21 with probability p s with probability q t with probability 1 - p - q where p, q (0, 1). The risk-free asset has prices A(0) = 1 and A(1) = 1.05. Give necessary and sufficient conditions on the constants s and t such that the model is arbitrage free If s = 20, t = 22, p = q = 0.2, find a portfolio (x, y) with y = 10 and positive x which has 2% risk

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock