Question: I know the question is a bit long. I will give you a really good rate!!! The market index model can be formulated as: R

I know the question is a bit long. I will give you a really good rate!!!

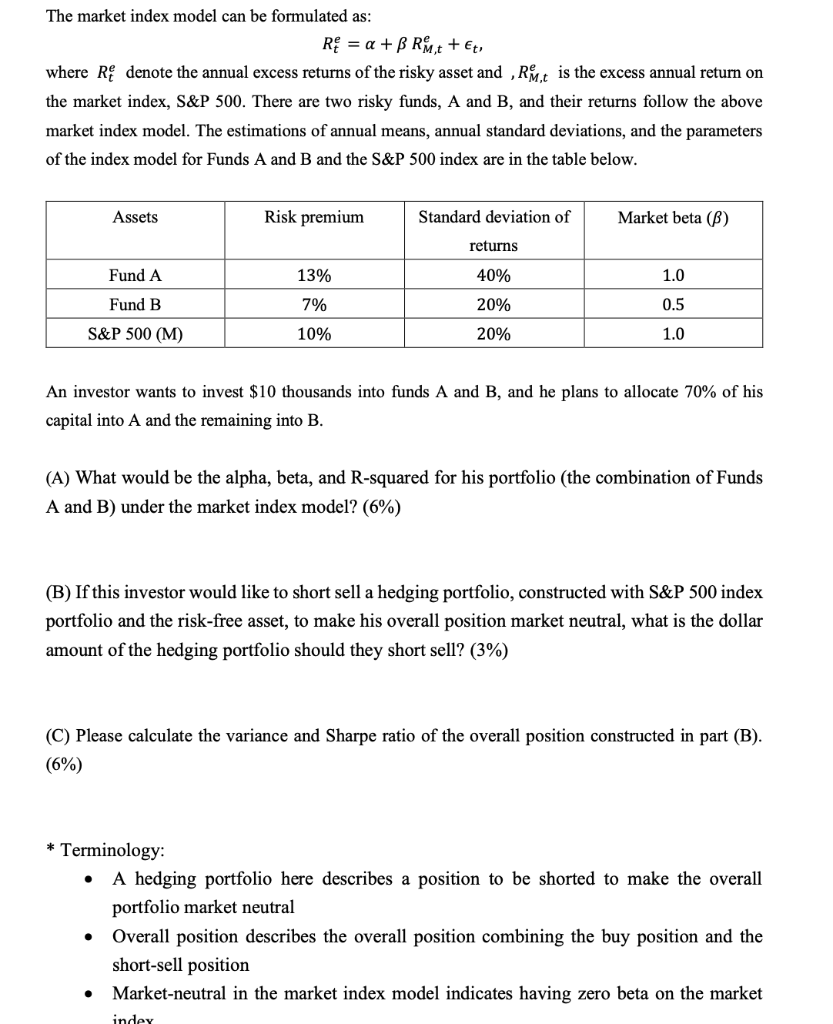

The market index model can be formulated as: R = a + B RM,+ + t, where R denote the annual excess returns of the risky asset and , RM,t is the excess annual return on the market index, S&P 500. There are two risky funds, A and B, and their returns follow the above market index model. The estimations of annual means, annual standard deviations, and the parameters of the index model for Funds A and B and the S&P 500 index are in the table below. Assets Risk premium Standard deviation of Market beta (B) returns Fund A 13% 40% 1.0 Fund B 20% 0.5 7% 10% S&P 500 (M) 20% 1.0 An investor wants to invest $10 thousands into funds A and B, and he plans to allocate 70% of his capital into A and the remaining into B. (A) What would be the alpha, beta, and R-squared for his portfolio (the combination of Funds A and B) under the market index model? (6%) (B) If this investor would like to short sell a hedging portfolio, constructed with S&P 500 index portfolio and the risk-free asset, to make his overall position market neutral, what is the dollar amount of the hedging portfolio should they short sell? (3%) (C) Please calculate the variance and Sharpe ratio of the overall position constructed in part (B). (6%) * Terminology: A hedging portfolio here describes a position to be shorted to make the overall portfolio market neutral Overall position describes the overall position combining the buy position and the short-sell position Market-neutral in the market index model indicates having zero beta on the market indey The market index model can be formulated as: R = a + B RM,+ + t, where R denote the annual excess returns of the risky asset and , RM,t is the excess annual return on the market index, S&P 500. There are two risky funds, A and B, and their returns follow the above market index model. The estimations of annual means, annual standard deviations, and the parameters of the index model for Funds A and B and the S&P 500 index are in the table below. Assets Risk premium Standard deviation of Market beta (B) returns Fund A 13% 40% 1.0 Fund B 20% 0.5 7% 10% S&P 500 (M) 20% 1.0 An investor wants to invest $10 thousands into funds A and B, and he plans to allocate 70% of his capital into A and the remaining into B. (A) What would be the alpha, beta, and R-squared for his portfolio (the combination of Funds A and B) under the market index model? (6%) (B) If this investor would like to short sell a hedging portfolio, constructed with S&P 500 index portfolio and the risk-free asset, to make his overall position market neutral, what is the dollar amount of the hedging portfolio should they short sell? (3%) (C) Please calculate the variance and Sharpe ratio of the overall position constructed in part (B). (6%) * Terminology: A hedging portfolio here describes a position to be shorted to make the overall portfolio market neutral Overall position describes the overall position combining the buy position and the short-sell position Market-neutral in the market index model indicates having zero beta on the market indey

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts