Question: i need answers for b and c 2. Data: Rz=14.5%;rf=2%; and z=4% a. Compute the expected rates of return and levels of risk for the

i need answers for b and c

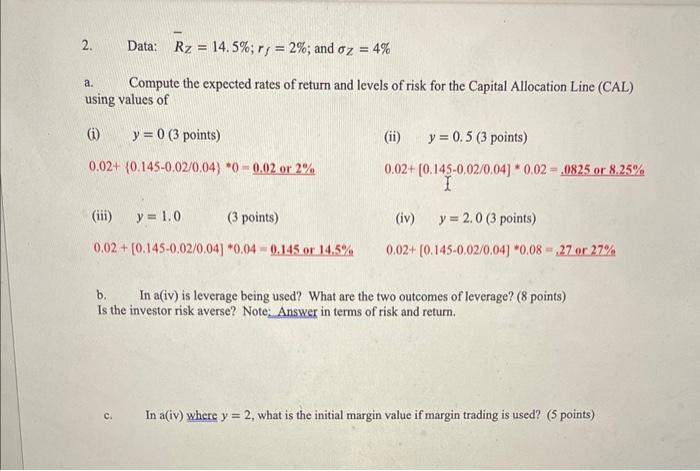

2. Data: Rz=14.5%;rf=2%; and z=4% a. Compute the expected rates of return and levels of risk for the Capital Allocation Line (CAL) using values of (i) y=0(3 points ) (ii) y=0.5(3 points ) 0.02+{0.1450.02/0.04}0=0.02or2%0.02+[0.1450.02/0.04]0.02=.,0825 or 8.25% (iii) y=1.0(3 points) (iv) y=2.0 (3 points) 0.02+[0.1450.02/0.04]0.04=0.145 or 14.5%0.02+[0.1450.02/0.04]0.08=.27 or 27% b. In a(iv) is leverage being used? What are the two outcomes of leverage? (8 points) Is the investor risk averse? Note; Answer in terms of risk and return. c. In a(iv) where y=2, what is the initial margin value if margin trading is used? ( 5 points)

Step by Step Solution

There are 3 Steps involved in it

1 Expert Approved Answer

Step: 1 Unlock

Question Has Been Solved by an Expert!

Get step-by-step solutions from verified subject matter experts

Step: 2 Unlock

Step: 3 Unlock