Question: I need help with D and E 3. In finance, we are often interested in how the return of one stock is related to some

I need help with D and E

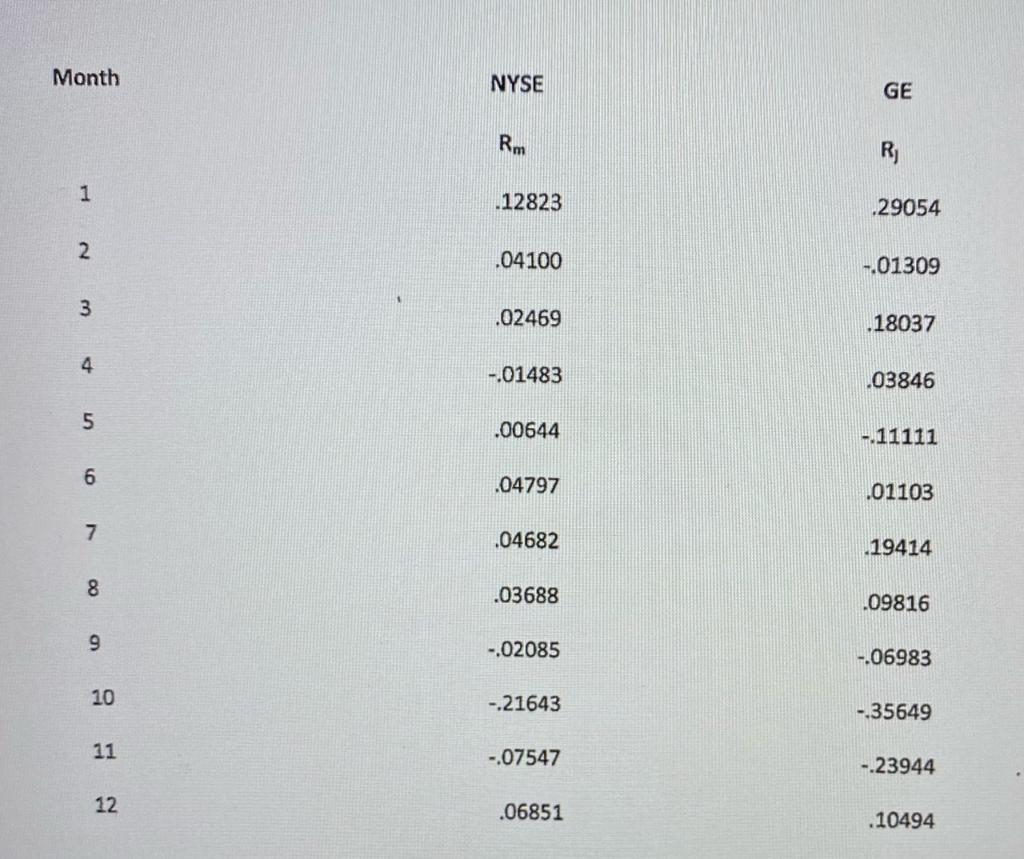

3. In finance, we are often interested in how the return of one stock is related to some market index such as NYSE. The model we usually estimate to understand this relationship is know as the market model and is given by the equation Rjx = a + bjRmt + ejt Where Rt = return on stock jin month t Rm,t = return on some market index in month t a = intercept of the regression b; slope of the regression elt = a random error term Use the data in the table in next page, answer the following questions. The table gives monthly rates of return for the value weighted New York Stock Exchange Index and GE stock. a. Estimate the regression coefficients and interpret them. b. Use a t-test to test the significance of the slope of the regression. C. Find the GE stock's beta coefficient. What type of information the stock's beta provide to investors? d. Find total risk, market risk, and diversifiable risk and interpret them. e. Forecast GE return, conditional on NYSE return of 0.05 and provide confidence interval for your forecast at 5 percent level. Month NYSE GE Rm 1 .12823 .29054 2 .04100 -.01309 3 .02469 .18037 4. -.01483 .03846 5 .00644 -.11111 6 .04797 .01103 7 .04682 19414 8 .03688 .09816 9 -.02085 -.06983 10 -.21643 -.35649 11 -.07547 -.23944 12 .06851 .10494 3. In finance, we are often interested in how the return of one stock is related to some market index such as NYSE. The model we usually estimate to understand this relationship is know as the market model and is given by the equation Rjx = a + bjRmt + ejt Where Rt = return on stock jin month t Rm,t = return on some market index in month t a = intercept of the regression b; slope of the regression elt = a random error term Use the data in the table in next page, answer the following questions. The table gives monthly rates of return for the value weighted New York Stock Exchange Index and GE stock. a. Estimate the regression coefficients and interpret them. b. Use a t-test to test the significance of the slope of the regression. C. Find the GE stock's beta coefficient. What type of information the stock's beta provide to investors? d. Find total risk, market risk, and diversifiable risk and interpret them. e. Forecast GE return, conditional on NYSE return of 0.05 and provide confidence interval for your forecast at 5 percent level. Month NYSE GE Rm 1 .12823 .29054 2 .04100 -.01309 3 .02469 .18037 4. -.01483 .03846 5 .00644 -.11111 6 .04797 .01103 7 .04682 19414 8 .03688 .09816 9 -.02085 -.06983 10 -.21643 -.35649 11 -.07547 -.23944 12 .06851 .10494

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts