Question: I need help with the following questions. Average Return Standard Deviation XOM= 0.808 5.910 DRIN 1.166 11.669 RF= 0.232 Correlation -0.210 The weight for XOM

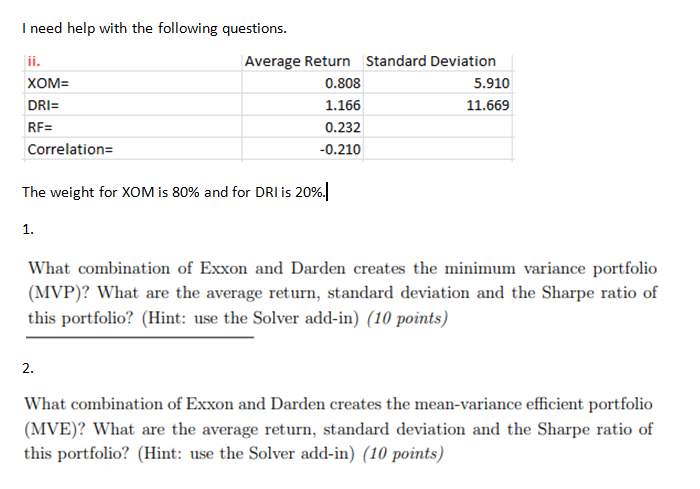

I need help with the following questions. Average Return Standard Deviation XOM= 0.808 5.910 DRIN 1.166 11.669 RF= 0.232 Correlation -0.210 The weight for XOM is 80% and for DRL is 20%.|| 1. What combination of Exxon and Darden creates the minimum variance portfolio (MVP)? What are the average return, standard deviation and the Sharpe ratio of this portfolio? (Hint: use the Solver add-in) (10 points) 2. What combination of Exxon and Darden creates the mean-variance efficient portfolio (MVE)? What are the average return, standard deviation and the Sharpe ratio of this portfolio? (Hint: use the Solver add-in) (10 points) I need help with the following questions. Average Return Standard Deviation XOM= 0.808 5.910 DRIN 1.166 11.669 RF= 0.232 Correlation -0.210 The weight for XOM is 80% and for DRL is 20%.|| 1. What combination of Exxon and Darden creates the minimum variance portfolio (MVP)? What are the average return, standard deviation and the Sharpe ratio of this portfolio? (Hint: use the Solver add-in) (10 points) 2. What combination of Exxon and Darden creates the mean-variance efficient portfolio (MVE)? What are the average return, standard deviation and the Sharpe ratio of this portfolio? (Hint: use the Solver add-in) (10 points)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts